If the stock market is defined as the S&P500, the answer is: “On average, no.”

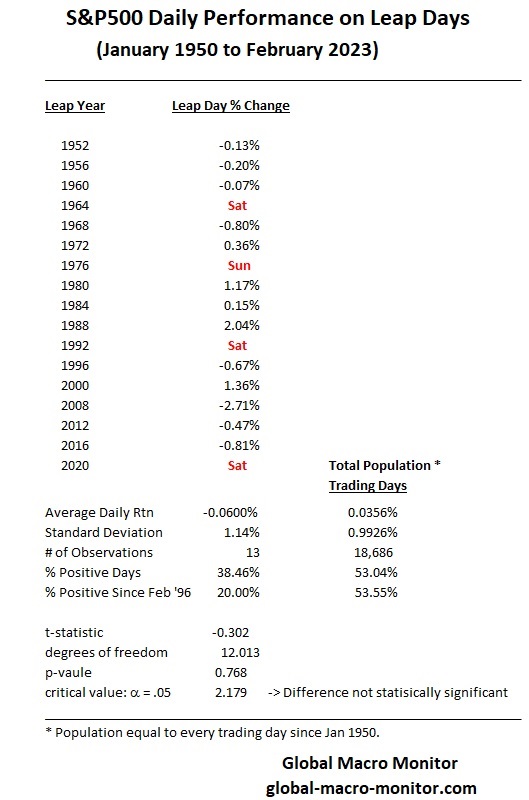

The following table illustrates that of the 13 leap trading days (February 29) since 1950, when the markets were open, the average leap day return is -0.06 percent versus 0.0356 percent for the total population of 18,686 trading days.

Only 5 of the 13 leap days (38 percent) have generated positive returns versus 53 percent for all trading days since 1950. Four of the past five leap days (2020 fell on a Saturday) have seen negative returns, with the last three consecutive leap days in the red.

Statistically Meaningful?

Is the return differential meaningful? Statisticians would say no.

Based on the results of our two-tailed t-test, there is insufficient evidence to conclude that a significant difference exists in the mean value between leap year returns.

The t-statistic of -0.302 indicates the direction and magnitude of the difference between the average returns, relative to the variation observed within the groups. However, the p-value of 0.768 falls short of the critical value at the 0.05 alpha level (95% confidence level) of 2.179, suggesting the hypothesis that the two means are not statistically different cannot be rejected. This implies that the observed difference in means between leap returns and all trading day returns is not statistically significant.

The significant disparity in sample sizes statistically swamps any of the signals one might gain from the differences in the data.

Traders Are Not Academics

Nevertheless, traders and algorithms are not academic statisticians. They look for patterns and run with them. In fact, it’s about time we get used to the fact that the new AI models, especially the LLMs, derive their logic from empirical observations, i.e., more data and patterns in the data, and less on traditional logic.

Place your leap day bets.