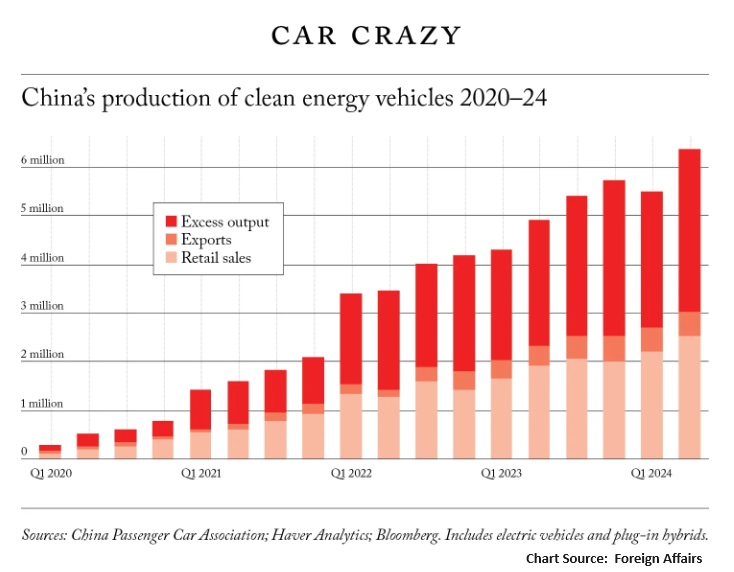

With electric vehicles, for instance, carmakers in Europe are already facing stiff competition from cheap Chinese imports. Factories in this and other emerging technology sectors in the West may close or, worse, never get built. – Foreign Affairs

China’s economic strategy of relying on global markets to absorb its excess production has led to significant overcapacity across multiple sectors, including steel, aluminum, electric vehicle batteries, and solar panels. This overinvestment has saturated domestic markets and strained international relations as foreign governments become wary of China unloading its surplus production, not to mention the country’s supply chain dominance. The consequences are concerning. Globally, Western manufacturing faces heightened competition, risking closures and stifling innovation. Domestically, overproduction has triggered price wars, depressed profits, and led to near-zero inflation, heightening the risk of China entering a deflationary spiral.

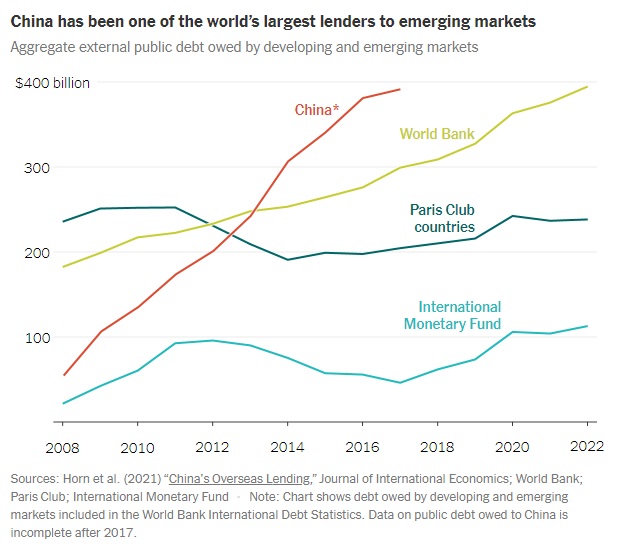

China’s collapse in foreign lending has contributed to a world of hurt and burdensome debt.

China also lent more than $1 trillion abroad, largely for infrastructure projects to be built by Chinese companies under its Belt and Road Initiative. Over the past two decades, one in three infrastructure projects in Africa was built by Chinese entities. The long-term debt risks for fragile developing economies were often ignored.

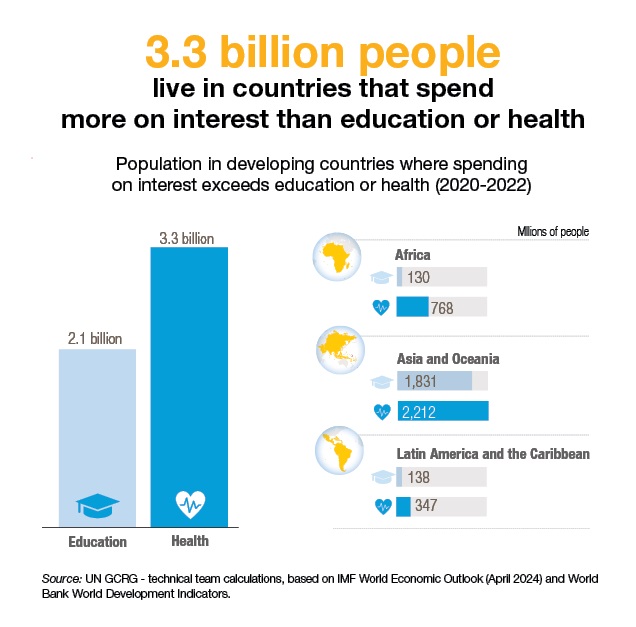

…China, now by far the world’s largest sovereign lender, has played a leading role in saddling many countries with levels of debt, often through nontransparent arrangements, that are comparable with those seen in the 1980s. The situation is becoming perilous. Over the past decade, during which China doled out more lending than the Paris Club — a grouping of 22 of the world’s largest creditor nations — the total value of interest payments of the 75 poorest countries in the world have quadrupled and will outstrip their total annual spending on health, education and infrastructure combined, according to the World Bank. An estimated 3.3 billion people live in countries where interest payments exceed investments in either education or health, the United Nations said. – NY Times

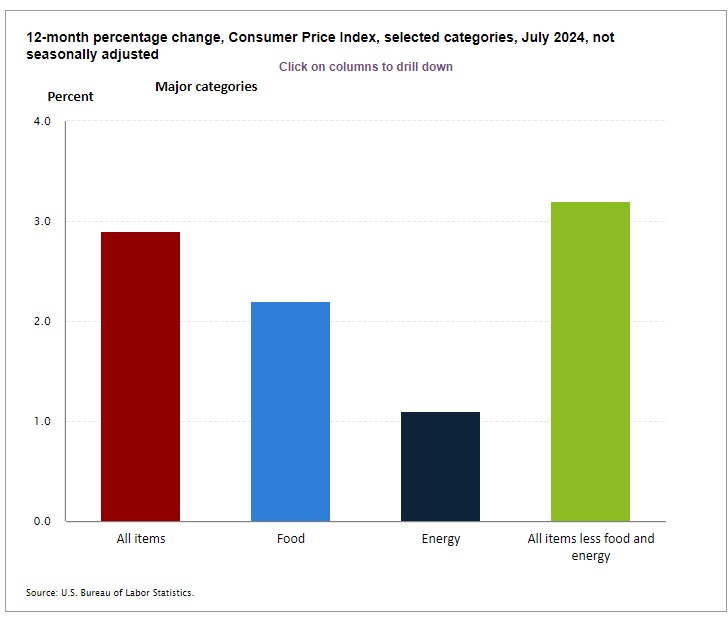

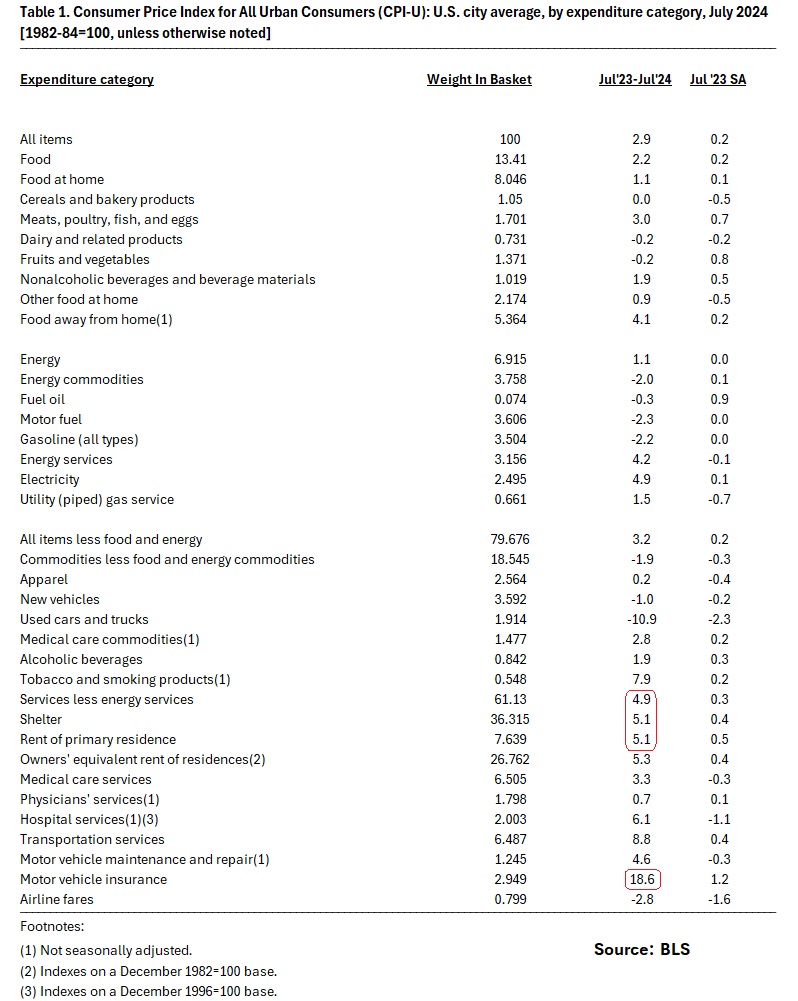

The Consumer Price Index for All Urban Consumers (CPI-U) rose by 0.2% in July on a seasonally adjusted basis, reversing the 0.1% decline in June. The annual increase was 2.9%, the smallest since March 2021. The shelter index was the main driver, contributing nearly 90% of the monthly rise, with a 0.4% increase. Energy prices remained flat after two months of decline, and food prices also saw a modest increase of 0.2%.

Core inflation, excluding food and energy, rose by 0.2% and 3.2% year-on-year, driven by gains in shelter, motor vehicle insurance, and household furnishings. Despite these increases, some areas like used cars, medical care, and airline fares saw price declines.

Cue the Fed.

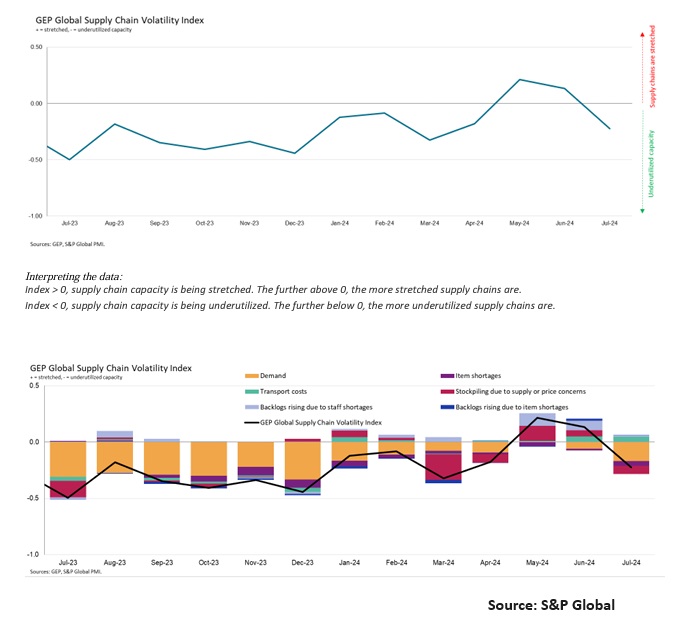

The latest release from S&P Global regarding the GEP Global Supply Chain Volatility Index for July underscores a marked decrease in supplier capacity utilization, falling to a four-month low not observed since April. This downturn indicates an alleviation of strains across international supply chains concurrently with a general softening in demand across multiple regions.

Europe stands out with pronounced underutilization, driven predominantly by a manufacturing sector grappling with recessionary forces. Germany, in particular, has seen a significant contraction in factory purchasing activity, exemplifying the region’s economic challenges.

Similarly, growth in Asia has slowed, with factory demand plummeting to the lowest levels since December 2023. Chinese manufacturing sectors have notably reduced purchasing activity for the first time in nine months, marking significant economic softening. Japan’s manufacturing malaise has further exacerbated the region’s declining performance.

Conversely, North America’s supply chain utilization has seen only marginal changes from June. Nevertheless, the region is not without difficulties, evidenced by a slowdown in purchasing across the United States, Mexico, and Canada. Canada, in particular, has experienced the most severe contraction within the region, whereas earlier growth observed in Mexican factories has abated somewhat, marking the first downturn in demand since October 2023.

Despite these challenges, global supply chains have maintained a degree of operational efficiency, with negligible disturbances in stock levels, shortages, or undue price fluctuations. However, global transportation costs have escalated to a 21-month peak, largely propelled by increased expenses in Asia.

The diminished purchasing activities reflect broader economic slowdowns, prompting intensified discussions about the necessity for the Federal Reserve to reduce interest rates to bolster demand and mitigate further economic deceleration in the latter half of the year.

Overall, the July 2024 S&P Global report signals growing concerns over deteriorating economic conditions globally, with particular emphasis on critical areas such as Europe and Asia and the subsequent impact on the efficiency of international supply chains.