We are reposting a piece we wrote back in ancient days about how this housing bubble, or “everything bubble” would be different from the last (also see here). One major factor why the economy is holding up and not responding to the very aggressive interest hikes by the Fed is that the supply curve for many factors has shifted left.

Housing Supply Curve

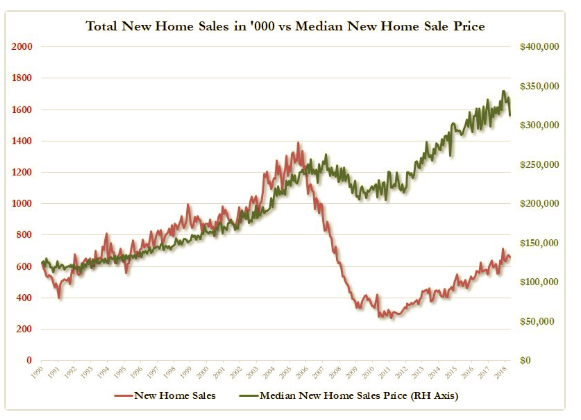

Theoretically, home prices should move inversely with mortgage rates but the lack of supply has ruptured that relationship during the current rodeo. This, in turn, affects consumption through the wealth effect as home prices remain intact. It’s amazing in our neck of the woods, a 1200 sq foot home or shack that sold for, say, $400k five years ago is now trading at close to $900k, if you can find one, that is. That’s an increase of more than 300 percent in the monthly mortgage payment. Simply stunning.

Note that 66 percent of Americans own their own homes. As always, we caution about getting lost in the averages. The home-ownership rate is vastly different among various age cohorts.

We have always maintained an increase in the relative price of housing — faster than wage increases, for example — is an intergenerational transfer of wealth from the young to the old. The following chart from the Census Bureau reinforces our point, kind of.

Doom Spending?

If homeowners still think they are millionaires, why not spend, spend, spend ’till daddy takes the T-Bird away? CNBC refers to it as “doom spending,”

Consumer spending has remained remarkably resilient in the face of some stiff economic headwinds.

Nearly all Americans, 96%, are concerned about the current state of the economy, according to a recent report by Intuit Credit Karma.

Still, more than a quarter are “doom spending,” or spending money despite economic and geopolitical concerns, the report found. – CNBC

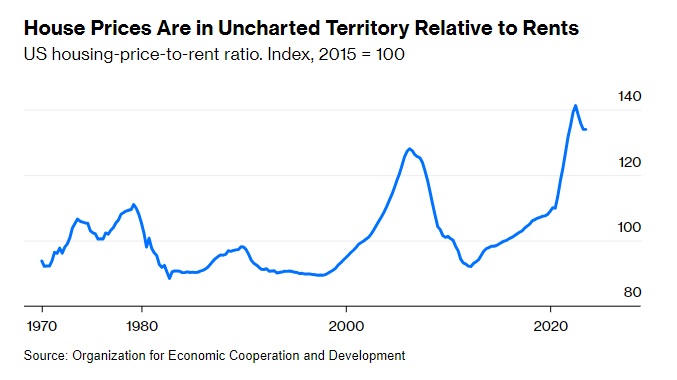

Overvalued As It Ever Has Been

The following chart from Bloomberg this morning illustrates how overvalued housing prices — even more so than the 2007 housing bubble. Eventually, rents will have to catch up, which means mo’ inflation or prices must come down to reality. The third way is that mortgage rates drop back to 3 percent, which would signal economic doom. You choose, folks.

Rents are to house prices what dividends or earnings are to stocks — the flow of income that justifies the value of the asset. When prices and rents get out of kilter, something presumably has to give eventually. As Federal Reserve Board economist Joshua Gallin put it at the June 2005 meeting of the interest-rate-setting Federal Open Market Committee, “rents provide a loose tether for house prices; prices deviate from their long-run relationship with rents for extended periods, but not indefinitely.” About a year and a half after that, US house prices began a five-year, 26% slide, going by the S&P CoreLogic Case-Shiller US National Home Price Index. – Bloomberg

The New Supply-Side Of Housing & Landlord Nation

David Stockman tweeted the following Zero Hedge chart this morning.

Clearly, a shift in the supply curve for new homes to the left.

OK – and some buying at irrational prices fueled by artificially low-interest rates and excess money. The irrational panic buying will take care of itself as interest rates rise and the Fed reduces its balance sheet making money tighter.

This is not the highly leveraged housing market of 2006-07, where even our range boy at the local golf club owned mortgaged three homes, quit his job, and bought an Escalade financed by a home equity loan (true story). This market is driven primarily by restricted supply and will be more difficult to pop. The price adjustment will also take place over a much longer period.

The New Supply-Side Economics Is Not Good

We have written how private equity has taken a yuuuge supply of existing homes off the market through their mega 2012-14 bankruptcy purchases, and now rent out the homes to the same people they foreclosed on. Existing housing is a perfect substitute for new homes.

Rising Costs

The rising costs of building, primarily labor shortages in the construction sector, and restrictive zoning laws are constraining building and the supply of new homes.

The lack of enough skilled workers and a narrow talent pipeline has added extra hurdles, time, and costs to many current projects, according to builders, hindering the current boom time in the industry.

“The number one issue is the cost and availability of labor,” says Randy Strauss, owner of Strauss Construction in Amherst, Ohio, roughly 40 miles east of Cleveland.

The issue is a nationwide one. Contractors in areas such as Houston, which were battered by Hurricane Harvey last year, have struggled to staff up, and the National Association of Home Builders recently found that 82 percent of its members believe the cost and availability of labor are their biggest issues. In 2011, only 13 percent named labor costs as their biggest worry. — Curbed

The immigration crackdown has played a significant role in the labor shortage in the construction sector.

One study from the National Bureau of Economic Research found that over 1.1 million undocumented immigrants, many of them skilled in essential trades such as framing, work in the construction industry. – CITYLAB

Lumber Prices

The parabolic rise in lumber prices isn’t helping either. Lumber prices are down over 12 percent from last week’s high, however, with several days of limit down in the futures markets. Look no further than the long-term lumber price chart to understand what tariffs do to prices and input costs, which ultimately hurt the majority.

Last April, the Trump administration placed a 20.83 percent tariff on Canadian lumber, to the benefit of politically valuable voters in Maine. Within the construction industry, these imports commonly turn into framing lumber, which is used to build single-family homes and small multifamily buildings.

– CITILAB

Bad timing by the administration unless you belong to the small minority of those who make their living in the framing lumber business.

Policy Relief Needed

Shortages are breaking out and are now ubiquitous throughout the economy.

The housing market is one of the hardest hit sectors. Shortages of new and existing homes; shortages of buildable land, shortages of skilled construction workers. Inflation is running rampant in the sector. Yet it hardly registers in the inflation indices because of the way the government measures housing costs.

The new supply-side of housing (shifting the curve left) is not working for most Americans. Taking existing homes off the market for rentals or the restriction of new supply through rising input costs, labor shortages, and zoning restrictions are severely reducing affordability and turning the country into a Landlord Nation.

Since most of the problems are policy-induced, they can be fixed by better and a more comprehensive housing policy. That is getting back to the old supply-side economics of the Reagan era where the supply curve shifts to the right, illustrated in the simple graph below. Lower prices with more supply of homes (P 2, Q 2).

Higher prices and lower supply may work for some, but it is certainly not good economics and only adds to an already toxic political environment.

It is time for disruption in housing.