Economies worldwide have thus far managed to steer clear of a recession, but the ongoing sustained decline in the global manufacturing sector paints a more complex picture. This phenomenon is succinctly explained by the above statement from Best Buy’s CEO.

[the] consumer electronics industry… remains challenged due to the pull-forward of demand in prior years and the various macroeconomic factors that we are all too familiar with…Our industry continues to experience lower consumer demand due to the pandemic pull-forward of tech purchases and the shift back into services spend outside the home like travel and entertainment… – Best Buy Earning Release & Conference Call, Aug 30th.

On a global scale, consumers are still transitioning from the significant surge in durable goods purchases during the COVID era to services. Furthermore, consumers face various macroeconomic challenges, including elevated inflation rates, mounting interest rates, a tightening monetary policy, and slowing economic growth.

Moreover, the growing weakness of the global consumer is another driving force behind the prolonged downturn in the consumer electronics industry. We anticipate that this sector will face challenges until mid-2024 when central banks begin to reverse their restrictive monetary policies and initiate interest rate cuts to stimulate demand.

It’s worth noting, however, that many non-cyclical sectors are thriving within the electronics industry thanks to ongoing secular growth trends. These include electric vehicles, healthcare technology, renewable energy infrastructure, and cloud computing. These sectors are faring considerably better in the current economic landscape

The Swiftie/Barbie Economy

In his Axios article titled “The Economy Runs on Girl Power,” Felix Salmon argues that Taylor

Swift’s “Eras” tour, along with the record-breaking box office sales of the “Barbie” movie, has significantly boosted spending on services and helped the U.S. economy steer clear of a recession.

Salmon also observes that “among the 69 markets monitored by Moody’s for hotel performance, those that featured a stop on the ‘Eras’ tour witnessed a notable upswing in revenue per available room compared to the same month in the previous year.”

He further posits the U.S. economy during the summer was driven by a novel equation:

Taylor Swift + Barbie = Goldilocks

The equation alludes to an economy characterized as “Goldilocks,” where conditions are neither excessively hot nor excessively cold, which fairly portrays the current economic climate in the United States.

Undoubtedly, the Swiftie/Barbie economy was reflected in the latest ISM services PMI, which unexpectedly jumped to 54.5 in August 2023, indicating the most robust growth in the services sector in six months. The price component came in quite hot, putting a dent in Goldilocks theme, however.

Manufacturing vs. Services

Manufacturing of durable goods typically dominates economic headlines, owing to its tangible nature and the availability of extensive historical data. For instance, the straightforward process of tallying durable goods production on an assembly line starkly contrasts the intricate challenge of quantifying services. While dentists can quantify filled teeth, measuring the output of customer service reps or auto mechanics performing a range of tasks is far from straightforward. Services like housekeeping, investment advice, teaching, and writing present complexities in output measurement.

Nonetheless, it’s essential to recognize that services constitute the lion’s share of economic activity, contributing over 70 percent of GDP in OECD nations. As we are currently observing, services play a pivotal role in driving economic growth and often serve as a vital counterbalance to a weakened manufacturing sector.

The service sector in the United States continues to display relative robustness. Conversely, the Eurozone recently experienced its first contraction in the services Purchasing Managers Index (PMI) since the preceding December. This contraction rate is the swiftest since February 2021, with all four major Eurozone economies reporting declines.

Recognizing that factories are driven primarily by actual unit sales, not the nominal dollar spending figures is crucial.

The Ratio of Consumption of Durables to Services chart further underscores this trend, revealing that in July, .26 units of durables were consumed for every unit of services, a decline from the peak of .30 but still an increase from the pre-COVID level of .20. When considering nominal consumption of durables, which accounts for prices, it currently stands at $.18 for every $1.00 spent on services. This marks a decrease from the peak of $.22 for every dollar of services consumed but is an improvement from the pre-pandemic figure of $.15.

The chart also highlights that the consumer preference mix between durables and services, as depicted by the ratio, requires further adjustment to return to its long-term trendline.

Price Trends

Both charts above implicitly depict the shifting dynamics in relative prices between durables and services, a trend further illustrated in our chart, Implicit Price Deflator Index: Durables vs. Services.

Notably, the price of services exhibits a persistent upward trajectory, while the extended downward trend in durable prices saw a reversal during the pandemic and continues to seek their equilibrium levels

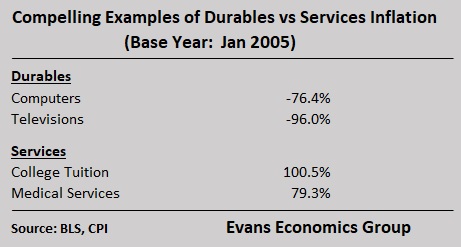

To underscore the contrasting trajectory of durable and service prices, we’ve assembled a table comparing the inflation rates of computers and televisions with those of medical services and college tuition. The findings are remarkable: there has been an almost 90 percent price reduction for durables and a corresponding 100 percent increase for services since 2005.

Upshot

Our analysis concludes that the ongoing shift in consumer preferences toward favoring services over durables has yet to run its course fully.

More importantly, a critical factor in revitalizing the manufacturing sector is reversing the macroeconomic headwinds confronting global consumers, a topic we delve into further in our country-specific outlooks below.

Make sure you set aside 10 minutes to watch this excellent interview with Walter Isaacson on his new book, Elon Musk.

We are conflicted about Elon: a terrific entrepreneur that the country surely needs more of, but we don’t fancy the frat boy antics and he did ruin Twitter! Ughh!

Click here for the interview.

US-China tensions are rewiring global trade, as the US seeks to reduce supply-chain reliance on geopolitical rivals and also source imports from closer to home. Mexico appeals on both counts—which is one reason it’s just overtaken China as the biggest supplier of goods to the giant customer next door.

On top of resurgent exports, Mexico boasts the world’s strongest currency this year and one of the best-performing stock markets. Foreign direct investment is already up more than 40% in 2023, even before Tesla Inc. starts building a proposed $5 billion factory. Not since the signing of the North American Free Trade Agreement in the 1990s has the country held the kind of allure for investors that it has right now. – Bloomberg

It was early August 2001 when I asked my wife if we should fly into Washington, D.C. a few days early before my best friend’s wedding. He was planning to marry his sweetheart on September 16, 2001, at St. John’s Episcopal Church. My 6 and 3-year-old daughters and I were in the wedding party.

I wanted some extra time for the girls to see the great sites of the Capitol City, where I had attended graduate school and began my career several years earlier.

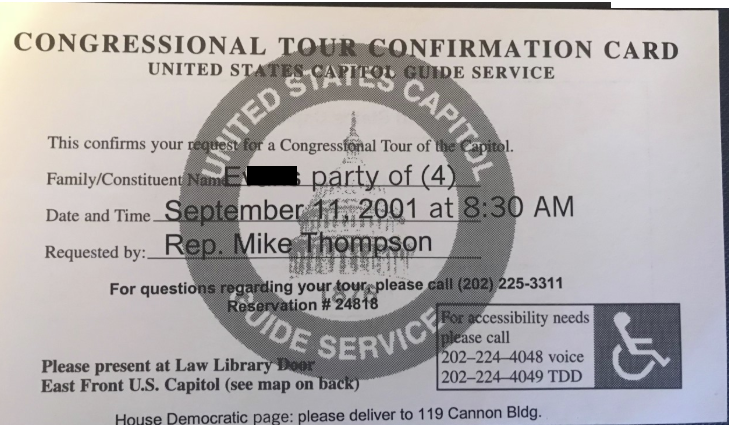

I secured some VIP passes from our congressman for tours of the White House and the U.S. Capitol. The passes came in the mail around mid-August with the date for the Capitol tour scheduled at 8:30 am, September 11, 2001.

Just another day. It was before history changed.

We also planned a trip to New York after the wedding as my girls wanted to visit their birthplace. The oldest specifically requested a trip to the top of the World Trade Center’s (WTC) Windows on the World.

Their last night in New York before moving to California was spent at the Marriott World Trade Center, South Tower.

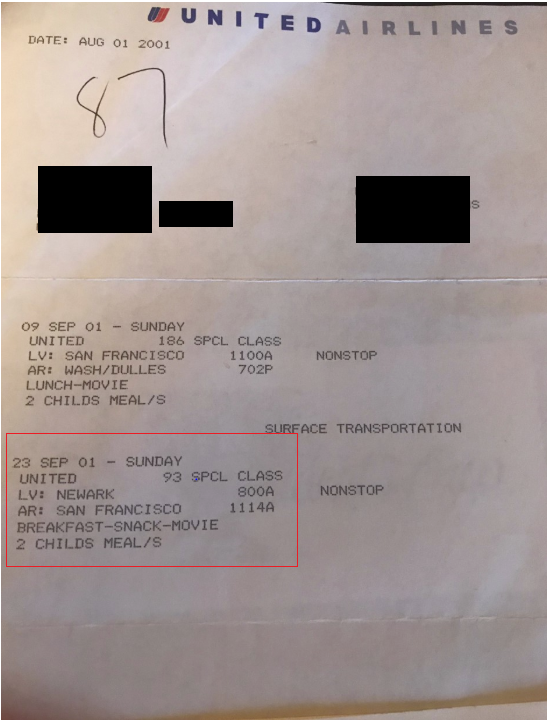

We booked our flights.

The return flight from New York was familiar. I had flown it at least a hundred times — United Flight #93, Newark to San Francisco.

Just another routine United flight. It was before history changed.

Washington, D.C.

We arrived at Dulles airport on Sunday night, September 9th, and it felt good to be back in Washington.

As we were disembarking, my 3-year-old noticed the overhead air blowers were still on and blowing hard. She shouted at me, “dad, they are wasting energy.”

The plane burst out in laughter. California was in the middle of an energy crisis and experiencing brownouts on a daily basis throughout that summer.

September 10, 2001

The following morning we had some downtime, and because the White House was only a few blocks from our Georgetown hotel, I took the girls down to see the president’s house. We arrived at the front gate, and I noticed the secret service on top of the White House with high-powered binoculars looking into the sky.

I hadn’t seen this since the day after the U.S. bombed Libya in 1986 in retaliation for Gaddafi’s bombing of a Berlin disco, which killed some American soldiers. I had an interview the next day at the Council of Economic Advisers (CEA) in the Old Executive Office Building. I recalled how tight security was, specifically, the sharpshooters on top of the White House.

Just for context, I hadn’t been in Washington in five years before our September 11, 2001 visit, and, no doubt, security had ramped up considerably. Put away those conspiracy theories.

Video Tape

I began filming the White House on the day before history changed, specifically the secret service with their high-powered eyes trained on the sky above the White House.

I mentioned to my family there must be “some sort of terrorist alert.” My bright, analytical 3-year-old immediately chimed in, “dad, they are trying to hurt the president.”

After thinking another minute, she asked, “dad, do they [the secret service] know we are good guys?” It was somewhat hilarious, at least, at the time. We have it all on tape.

Lafayette Park

It was hot and humid in Washington on September 10, 2011, the day before history changed. I took the family across the street, sat them on a bench in Lafayette Park, and went to fetch them some water from a street vendor.

Before leaving on the water run, I noticed a middle eastern looking man sitting on the bench next to my daughters. He was fiddling with his cell phone and rapidly thumbing through a stack of ATM receipts. I recall some were from Bank of America.

What struck me most was his fidgety and nervous demeanor.

He was casually dressed in nice khaki slacks, an olive-green button-down shirt, and sandal-like full-toed shoes. He smelled of cheap European cologne. I will never forget his face.

During my search for water, for some reason, I had a bad feeling. I began to think the man on the bench fit the profile of a terrorist. I seriously thought about walking back across Pennsylvania Avenue to report the suspicious character to the uniform secret service officers at the White House north gate. I am sure they would have laughed and dismissed me as some kook.

When I got back to the park, the man was gone. I asked my wife, “what happened to the guy sitting on the bench? He reminded me of a terrorist.” True story.

Racial profiling? Do you really think I gave a shit?

I had a strong feeling based on his actions and my experience being so close to the first 1993 bombing of the World Trade Center when I worked on Wall Street.

September 11, 2001

At about 8:00 am, my wife woke us in a panic. We had overslept and needed to hurry to get to the Capitol building.

I knew we wouldn’t make it on time and, reluctantly, put the kibosh on our trip up to the Hill. She and the oldest went down to the lobby to grab some breakfast. My youngest, still suffering from jet lag, was sound asleep.

I was reading the Washington Post when they returned to the room in horror and said to turn on the television as a plane had crashed into the World Trade Center.

For the next few hours, I watched in shock and was on the phone constantly to my friend, the bridegroom, who had a view of the WTC from his Greenwich Village apartment.

When American #77 went into the Pentagon about an hour later, it was only a few minutes before the F-14s buzzed over our Georgetown hotel.

I went outside, saw people hustling up the sidewalk, and noticed the military had come out on the street. A military Humvee stationed at every corner in Georgetown. This doesn’t happen in America.

Get Out Of Washington

I began to fear for the safety of my family and decided it was time to get out of Washington. I told my wife, “if these people have chemical or nuclear weapons, we are smack in the middle of their target.”

As I was going out the door to rent a car, my oldest shouted, “dad, get a purple car.” Yeah, right, I thought.

I arrived at Hertz in Georgetown, and the clerk said I was lucky as there was one car left. They pulled the car up to the office. A purple Volvo!

Charlottesville

On our way to Charlottesville, I was overcome with the incredible grief that all of America was suffering, especially thinking about my friends in the WTC. I felt sick.

It was the end of American exceptionalism. These things just don’t happen in America.

Seeing the American flags draped over the freeway overpasses on our drive to southern Virginia, I thought, as many others did on that day that changed history, this is my generation’s Pearl Harbor.

September 12

The next day at Jefferson’s Monticello, a busload of senior Japanese tourists pulled up to our third president’s home. They were soon smitten with my 3-year-old. She was one helluva of a cute baby with a unique and very friendly persona.

The Japanese tourists asked to take pictures with her. I warmly agreed and thought how surreal, the day after our own Pearl Harbor. Surely some of these people were alive, and on the other side, on December 7, 1941.

It was the first few days of the grave new crisis, and the nation was grieving and in complete shock, just as the Pearl Harbor generation was on that dark December day, which changed history 60 years earlier. And there was my child chumming it up, the pearl in the eyes of these beautiful Japanese seniors, who were once considered the enemy of the “greatest generation” just a little over a half-century prior.

It gave me a glimmer of hope that the country would make it through the dark days.

The Japanese are now one of our closest allies, which could never have happened without forgiveness. No peace without justice, no justice without forgiveness.

Whenever I have a chance and feel it’s safe or not inappropriate, I ask my Japanese friends if they forgive the U.S. for bombing Hiroshima and Nagasaki. I have never received an unequivocal answer. Not once.

It seems the official position is to sweep it under the rug,

In 2007, during Shinzo Abe’s first term as prime minister, Defense Minister Fumio Kyuma referred to the bombing of Hiroshima and Nagasaki as “something that couldn’t be helped.” – LA Times, April 2016

The FBI

Nevertheless, the day after the September 11th attacks, I began to think about that man I encountered in Lafayette Park the day before.

I contacted the FBI to report the incident.

At first, they seemed to mock me. Asking how he was dressed, probably thinking I would reply, “in Arab garb,” such as thobe and a ghutra and egal.

I spoke with the FBI several times after that. They always remained aloof and never provided information.

Enter Bob Woodward

I then contacted the Washington Post’s Bob Woodward, who put me in touch with his research assistant. We had about an ½ hour conversation in which he told me that Al-Qaeda liked to scout their targets just before hitting them.

Was the White House a target?

Several reports specifically identified Capitol Hill and the White House as targets on Sept. 11. One said a bin Laden associate — erroneously — “gave thanks for the explosion in the Congress building.”

A key figure in the bin Laden financing organization called Wafa initially claimed “the White House has been destroyed,” before having to correct himself. – Washington Post, January 28, 2002

I can’t remember if the FBI or Woodward’s guy confirmed that the 9/11 terrorists were emptying their bank accounts just before the attack and transferring the cash back to the UAE.

From September 5 through September 10, 2001, the hijackers consolidated their unused funds and sent them to Hawsawi in the UAE – National Commission on Terrorist Attacks

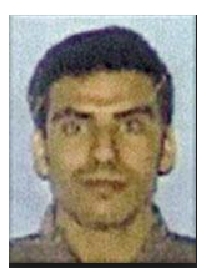

The ATM receipts were convincing enough, but my suspicions about the man in the park were confirmed when the FBI released the photos of the 9/11 hijackers,

I will never forget that face.

I had sat my daughters down on a park bench across the street from the White House on the day before September 11, 2001, with one of the hijackers. Khalid Al Mihdhar was a senior Al-Qaeda operative who crashed American Airlines Flight #77 into the Pentagon.

How twisted was it that on September 10, 2001, secret service agents were on top of the White House combing the sky for potential terrorists, and one of the Al-Qaeda hijackers was sitting just under their nose, less than 1,000 feet away?

The Wedding

My friends bravely decided not to cancel their wedding the following Sunday, and we participated and shared with them their joy under highly stressful conditions.

The church was located just across the street from Lafayette Park, a stone’s throw from the White House, where presidents-elect traditionally attend their pre-inaugural church service.

During the middle of the wedding, with the country and all of us still nervous and on pins and needles, an army of sirens began to blare. It seemed like it lasted for an hour. Almost certainly, everyone in the church thought another attack might be underway.

I thought the presbyter was going to stop the wedding. We got through it.

Back Home

When the government lifted the ban on air travel, we caught one of the first flights out of Dulles back to the west coast. That was one nervous flight.

One of our flight attendants freaked out when a passenger refused to sit down. I have no doubt our plane was crawling with air marshals.

We Made It

We did get through it. The nation got through it.

The world is much different now.

September 11th was way too close to my family, and we were fortunate to escape the ultimate tragedy.

Not so for many of our friends, fellow Americans, and good citizens from other countries who lost their lives on that day that changed history.

I miss my friends who lost their lives that day.

Please, God, bless their families and all those who lost loved ones, the brave Americans who have made the ultimate sacrifice protecting us, and the many who still work to keep us safe.

Everyone Has A Story

Every person remembers precisely where they were, and what they were doing on the day that changed history.

I have wanted to write this story down for 17 years but just couldn’t do it. Now my children will have it to pass on to their children.

Everyone has a 9/11 story. Write it down. It’s cathartic.

The world’s liberal geopolitical order led by the United States, which has driven the global economy for more than 70 years, is now under severe stress. Based on rules-based international cooperation, the post-war order ushered in decades of relative peace and prosperity. However, it is now morphing into a world of uncertainty, with the rise of economic nationalism reflected in the proliferation of country-specific and even supranational industrial policies.

More importantly, the competition between the world’s two dominant powers, the United States and China, is resetting cross-border trade and investment flow. Whatever future world economic order emerges, it will almost certainly result in a relatively lower trajectory of economic growth, higher inflation, and lower global prosperity in its steady-state equilibrium if one is ever to be obtained.

China’s PPP GDP Exceeds The U.S.

Figure 1 illustrates the rapid rise of the Chinese economy, which is now 23 percent larger than U.S. GDP on a purchasing power parity (PPP) basis. The PPP exchange rate attempts to level the purchasing power of both countries. Think of the PPP as the exchange rate that equates the price of a Big Mac in New York and Beijing in dollars, for example.

Many are now speaking of “Peak China” and believe its about to enter a long period of Japanification. Not so fast!

Undoubtedly, the country has some enormous structural problems, but its tech sector continues to rapidly advance as exhibited by Huawei’s recent release of the Mate 60 Pro, powered by SMIC’s 7nm advanced processor.

The release surprised many in the West, who underestimated China’s ability to make the more advanced chips. It was also a shock to many that China was able to circumvent U.S. efforts to block China’s access to the technology for advanced chip making.

Electronic Manufacturing Sector

The competition between the two superpowers is reshaping the global order, causing seismic shifts and significant dislocations in the electronics manufacturing industry. The superpower competition will be a major driver of the electronics manufacturing industry for many years to come.

The desire of both powers to gain a global technological advantage currently drives much of the competition, especially in the field of Artificial Intelligence.

Whoever becomes the leader in this sphere [A.I.] will become the ruler of the world – Vladimir Putin

That puts the electronics sector squarely in the middle of the conflict. The shifting tectonic plates of investment and trade flows, driven by a rethinking and de-risking of the global supply chain, will increase the uncertainty about how this plays out. It will also provide many new opportunities for companies that can remain flexible. We will have more to say on this in future newsletters.

But first, we need to put some historical context to the changing geopolitics and expand more on its existential threat.

The Thucydides’ Trap

The most critical issue concerning the emerging new international order is whether the confrontation between China and the United States can avoid the “Thucydides’s Trap.”

Named after the ancient Greek historian, the Thucydides’s Trap is a cautionary concept, highlighting the perils that arise when a rising ascendant power seeks to challenge an existing superpower. Notable historical instances of this dynamic include the age-old rivalry between Athens and Sparta in ancient Greece and the analogous comparison between Germany and Britain in the last century.

Drawing insights from historical narratives, a group affiliated with the Harvard Belfer Center for Science and International Affairs, under the leadership of Harvard history professor Graham Allison, calculated that most of the similar historic rivalries concluded unfavorably.

Their research showed that twelve of sixteen analogous scenarios spanning the past five centuries culminated in armed conflicts (see Figure 2). The four cases where a significant conflict was averted necessitated concessions by both the ascendant and established power, which required compromises and often painful adjustments in both actions and perceptions.

Complacency

Given the present trajectory, the likelihood of a future conflict between the United States and China is considerably higher than currently recognized or priced in the markets. Based on historical precedents, the empirical probability of conflict tilts more toward a major confrontation. As Allison points out, what many believe as “inconceivable” is not a fundamental statement about the possible state of future geopolitics but more about what our limited minds can conceive.

This past January, for example, the four-star Air Force general, Mike Minihan, sent a memo to his officers predicting the U.S. would be at war with China in two years. The general’s logic was based on his perception that the Taiwan and the U.S. presidential elections in 2024 will increase the risk that the U.S. is distracted and may be an opening for President Xi Jinping to move on Taiwan.

Moreover, the recent and relatively rapid deterioration of the Chinese economy may give the Chinese Communist Party (CCP) an excuse to lash out at the U.S. and blame the country’s economic woes on America’s imposition of trade and investment restrictions.

Not Likely

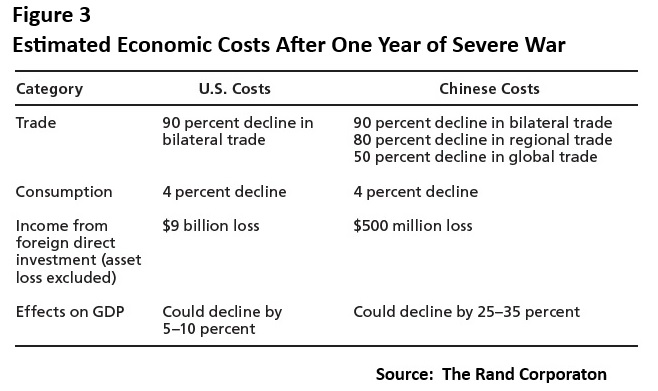

Call us optimists – we prefer realists – but a war between the two powers is certainly not inevitable, and we believe it to be unlikely. Due to both countries’ size and global economic integration, a Sino-U.S. hot war would be immensely costly for both nations and East Asia, as well as the rest of the world.

In their 2016 study (Figure 3), the Rand Corporation estimated the direct economic costs of a year-long conflict in both countries. We believe their estimates of a 5-10 percent decline in U.S. GDP and a 25-35 percent fall in China’s economy are much too conservative.

Given the integrated global supply chain, a hot war would push the world economy into a vicious feedback loop. The nonlinearity of such an event makes it impossible to estimate just how bad the carnage would be. And we are just talking economics here, folks.

Nevertheless, underestimating and misinterpreting the inherent risks in the U.S.-China relationship can ironically contribute to and increase the risk of conflict.

The relationship between the two major powers, including their bilateral relations with other nation-states, must be managed carefully and thought through with great diligence, combining a delicate balance of deterrence and diplomacy.

Careful Vigilance

Finally, one aspect related to Thucydides’s Trap is that it’s not just some big, extraordinary event that can instigate a significant conflict, such as an invasion or blockade of Taiwan. Even unremarkable occurrences can do so.

When a rising power poses a challenge to a reigning power, routine or minor crises that could typically be contained, such as the assassination of the archduke in 1914, can trigger a chain of events, causing unexpected and devastating outcomes that would take decades to recover from.

Time to stop sleepwalking.