The world’s liberal geopolitical order led by the United States, which has driven the global economy for more than 70 years, is now under severe stress. Based on rules-based international cooperation, the post-war order ushered in decades of relative peace and prosperity. However, it is now morphing into a world of uncertainty, with the rise of economic nationalism reflected in the proliferation of country-specific and even supranational industrial policies.

More importantly, the competition between the world’s two dominant powers, the United States and China, is resetting cross-border trade and investment flow. Whatever future world economic order emerges, it will almost certainly result in a relatively lower trajectory of economic growth, higher inflation, and lower global prosperity in its steady-state equilibrium if one is ever to be obtained.

China’s PPP GDP Exceeds The U.S.

Figure 1 illustrates the rapid rise of the Chinese economy, which is now 23 percent larger than U.S. GDP on a purchasing power parity (PPP) basis. The PPP exchange rate attempts to level the purchasing power of both countries. Think of the PPP as the exchange rate that equates the price of a Big Mac in New York and Beijing in dollars, for example.

Many are now speaking of “Peak China” and believe its about to enter a long period of Japanification. Not so fast!

Undoubtedly, the country has some enormous structural problems, but its tech sector continues to rapidly advance as exhibited by Huawei’s recent release of the Mate 60 Pro, powered by SMIC’s 7nm advanced processor.

The release surprised many in the West, who underestimated China’s ability to make the more advanced chips. It was also a shock to many that China was able to circumvent U.S. efforts to block China’s access to the technology for advanced chip making.

Electronic Manufacturing Sector

The competition between the two superpowers is reshaping the global order, causing seismic shifts and significant dislocations in the electronics manufacturing industry. The superpower competition will be a major driver of the electronics manufacturing industry for many years to come.

The desire of both powers to gain a global technological advantage currently drives much of the competition, especially in the field of Artificial Intelligence.

Whoever becomes the leader in this sphere [A.I.] will become the ruler of the world – Vladimir Putin

That puts the electronics sector squarely in the middle of the conflict. The shifting tectonic plates of investment and trade flows, driven by a rethinking and de-risking of the global supply chain, will increase the uncertainty about how this plays out. It will also provide many new opportunities for companies that can remain flexible. We will have more to say on this in future newsletters.

But first, we need to put some historical context to the changing geopolitics and expand more on its existential threat.

The Thucydides’ Trap

The most critical issue concerning the emerging new international order is whether the confrontation between China and the United States can avoid the “Thucydides’s Trap.”

Named after the ancient Greek historian, the Thucydides’s Trap is a cautionary concept, highlighting the perils that arise when a rising ascendant power seeks to challenge an existing superpower. Notable historical instances of this dynamic include the age-old rivalry between Athens and Sparta in ancient Greece and the analogous comparison between Germany and Britain in the last century.

Drawing insights from historical narratives, a group affiliated with the Harvard Belfer Center for Science and International Affairs, under the leadership of Harvard history professor Graham Allison, calculated that most of the similar historic rivalries concluded unfavorably.

Their research showed that twelve of sixteen analogous scenarios spanning the past five centuries culminated in armed conflicts (see Figure 2). The four cases where a significant conflict was averted necessitated concessions by both the ascendant and established power, which required compromises and often painful adjustments in both actions and perceptions.

Complacency

Given the present trajectory, the likelihood of a future conflict between the United States and China is considerably higher than currently recognized or priced in the markets. Based on historical precedents, the empirical probability of conflict tilts more toward a major confrontation. As Allison points out, what many believe as “inconceivable” is not a fundamental statement about the possible state of future geopolitics but more about what our limited minds can conceive.

This past January, for example, the four-star Air Force general, Mike Minihan, sent a memo to his officers predicting the U.S. would be at war with China in two years. The general’s logic was based on his perception that the Taiwan and the U.S. presidential elections in 2024 will increase the risk that the U.S. is distracted and may be an opening for President Xi Jinping to move on Taiwan.

Moreover, the recent and relatively rapid deterioration of the Chinese economy may give the Chinese Communist Party (CCP) an excuse to lash out at the U.S. and blame the country’s economic woes on America’s imposition of trade and investment restrictions.

Not Likely

Call us optimists – we prefer realists – but a war between the two powers is certainly not inevitable, and we believe it to be unlikely. Due to both countries’ size and global economic integration, a Sino-U.S. hot war would be immensely costly for both nations and East Asia, as well as the rest of the world.

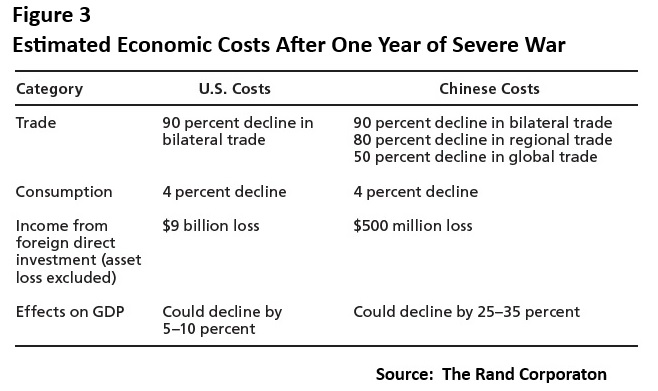

In their 2016 study (Figure 3), the Rand Corporation estimated the direct economic costs of a year-long conflict in both countries. We believe their estimates of a 5-10 percent decline in U.S. GDP and a 25-35 percent fall in China’s economy are much too conservative.

Given the integrated global supply chain, a hot war would push the world economy into a vicious feedback loop. The nonlinearity of such an event makes it impossible to estimate just how bad the carnage would be. And we are just talking economics here, folks.

Nevertheless, underestimating and misinterpreting the inherent risks in the U.S.-China relationship can ironically contribute to and increase the risk of conflict.

The relationship between the two major powers, including their bilateral relations with other nation-states, must be managed carefully and thought through with great diligence, combining a delicate balance of deterrence and diplomacy.

Careful Vigilance

Finally, one aspect related to Thucydides’s Trap is that it’s not just some big, extraordinary event that can instigate a significant conflict, such as an invasion or blockade of Taiwan. Even unremarkable occurrences can do so.

When a rising power poses a challenge to a reigning power, routine or minor crises that could typically be contained, such as the assassination of the archduke in 1914, can trigger a chain of events, causing unexpected and devastating outcomes that would take decades to recover from.

Time to stop sleepwalking.