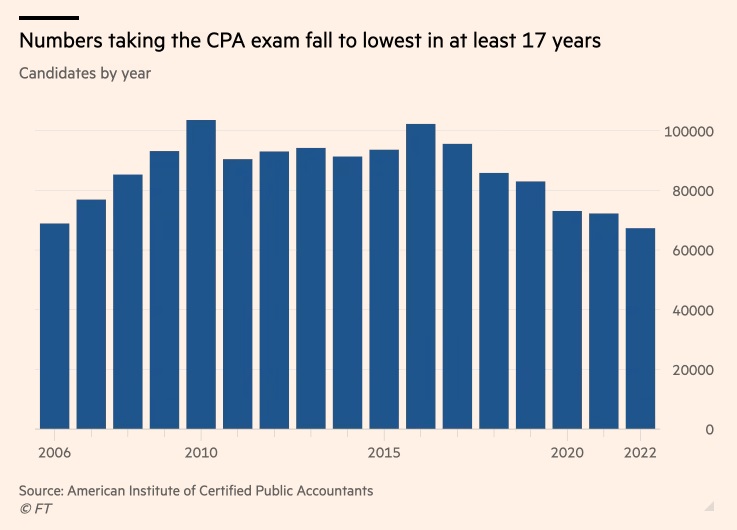

Good piece in the FT about the number of people taking the CPA exam in 2022 has dropped to its lowest level since the beginning of records for the modern exam in 2006.

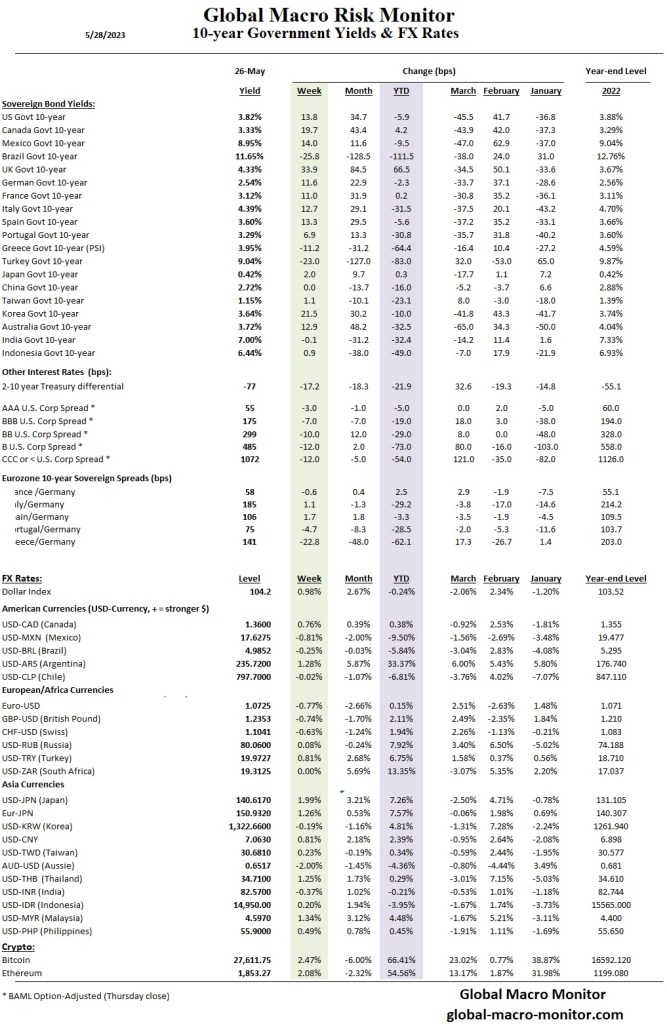

Money Points:

Nope!

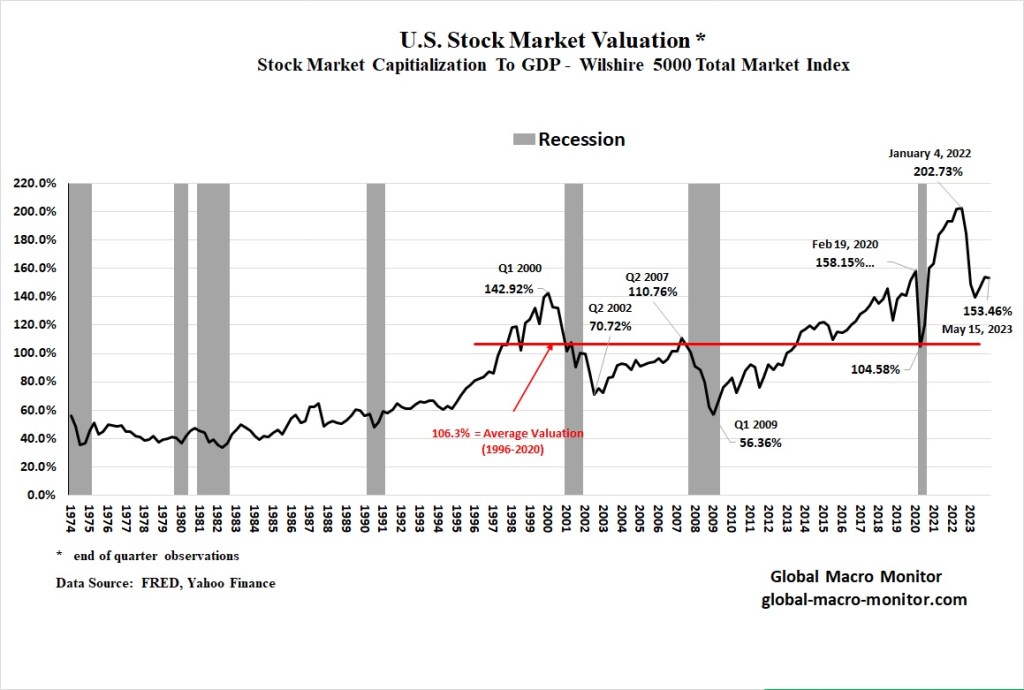

Based on Warren Buffet’s favorite stock market valuation metric, the market remains very expensive.

Note this is a mean-reverting chart — that is, the time series does not move from lower left to higher right as the total market capitalization as measured by the Wilshire 5000 is normalized by nominal GDP but will revert back to its mean valuation level.

Over the years, there have been various rationalizations as to why the market remained in the super-expensive zone for so long, such as globalization, low inflation, free money, China opening, offshoring, zero interest rates, and quantitative easing.

No mas, all gone. Now, the market must stand alone and grow earnings, and earnings grow with the economy.

Stay frosty, folks.

The summer trading doldrums have arrived, and our current market analysis indicates that long-term investors lack conviction. As a result, traders are pushing the S&P lower in the morning and covering into the close, stifling market volatility — albeit deceptively. However, there are underlying concerns that suggest we shouldn’t be complacent.

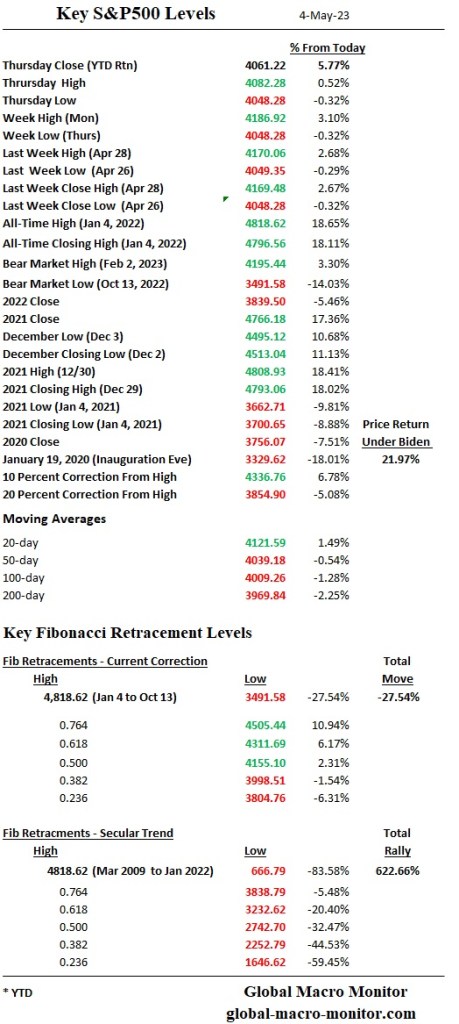

The market also appears to be trading as if the leveraged and fast money set is net short. The S&P closed the week right at its 20-day moving average and held the 4098ish level twice, while the rejection at the Wednesday high of 4154.28 occurred at the key .50 fibo for this bear market at 4155.10.

It’s a mug’s game trying to predict short-term market moves, but let us humor you going into the weekend. We suspect that next week, the recent market low at 4098.92 will break, and the S&P will test its 50-day moving average at 4057 soon, and very soon. If the 50-day moving average breaks, prepare for a summer vacation visiting the 200-day moving average at 3974.61.

On the upside, this week’s high and .50 fibo at 4155 is now the key resistance level to watch,

Firm convictions held loosely.

Stay frosty, folks.

The Monthly Treasury Statement has been released, and the data reveals a continued deterioration of the deficit, which is now at around 7.3 percent of GDP on a 12-month trailing basis. The Economist recently expressed concerns that the U.S. budget deficit could reach 7 percent by the end of the decade, and it appears we are already there.

We estimate that deficits could reach around 7% of GDP a year by the end of this decade—shortfalls America has not seen outside of wars and economic slumps. – Economist

We are alarmed by the rapid decline in budget receipts, which have fallen by 10 percent during the first seven months of the 2023 fiscal year compared to the previous year, with individual income taxes down by 18 percent. The April surplus was only 57 percent of last year’s surplus, which could be partly attributed to the slowing economy and, also, many of the wealthy California counties being given extra time to file their taxes due to the earlier floods. Maybe.

What’s even more concerning is the toxic cocktail of declining budget revenues and increasing interest payments on the national debt, which now exceed what the U.S. currently spends on its military programs.

Deficits don’t matter…until they do.

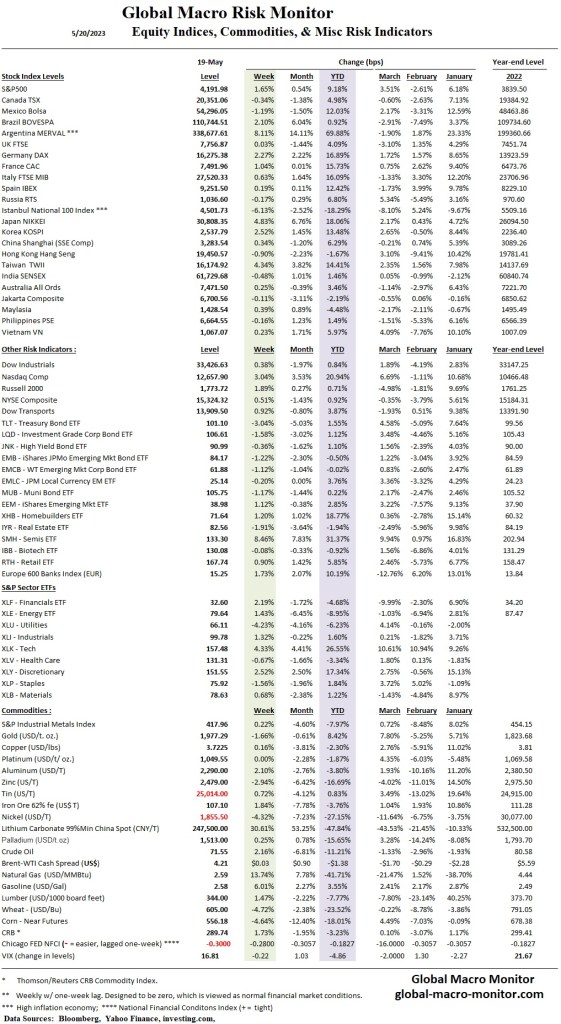

Note the S&P traded within 9 points from its February bear market high on Monday before falling 125 points into today’s close. The market is now in the hands of large depositors ($250k) in the regional banks. See no evil bank balance sheets are all the rage now, and who knows what evils lurk beneath those sheets. Therein lies the problem. Uncertainty.

The S&P index has held its 50-day moving average twice this week, including today. The KBW regional bank index is down over 30 percent since the beginning of March and put it in a nice dragonfly doji candle today, which may signal a short-term bottom, or it may not. Watch this space.

Aslan Capital is still on the move.