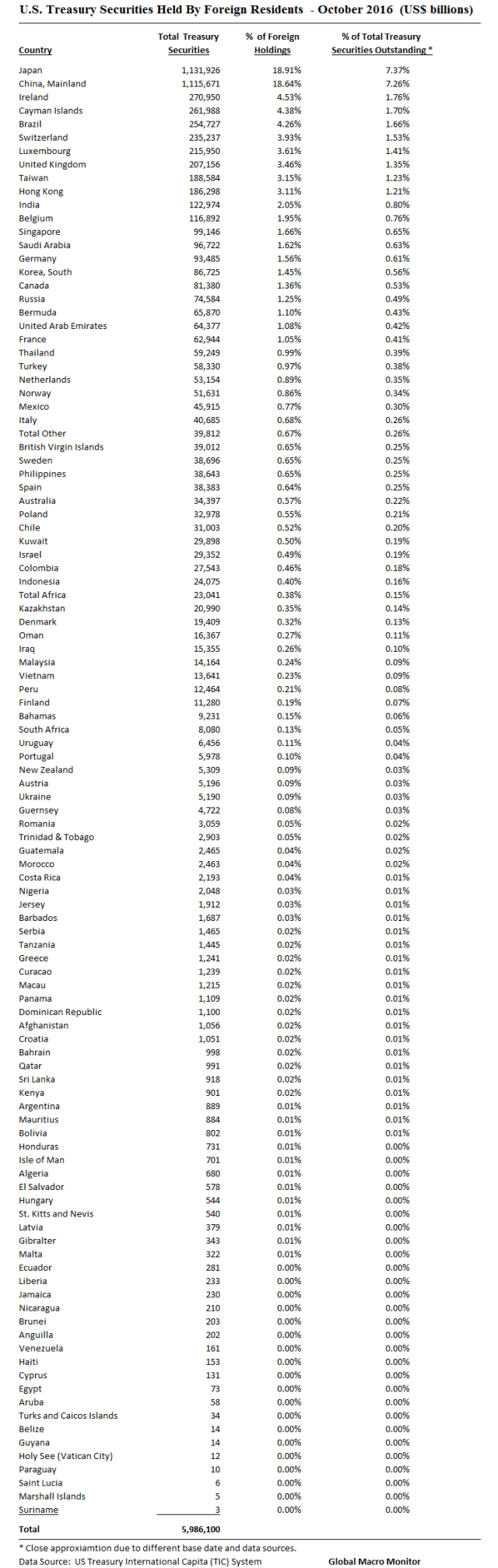

The ginormous table below of foreign holdings of U.S. Treasury securities compliments Friday’s post, TOTD: Who Owns The Treasury Market?

First some background, a few caveats about the data, some thoughts on how the U.S. became so dependent on foreign financing and what we think the future holds under a Trump Administration. Feel free to ignore the wonkish stuff below and go straight to the Table.

Ireland and the Cayman

First, the total of foreign-held Treasury securities slightly differs from our earlier post probably due to differing reporting dates and reporting systems. Close enough for government work in our book, however.

Second, note that Ireland and the Cayman Islands are the third and fourth largest foreign holders of Treasuries. Does this make sense given the size of their economies? The data put Ireland’s holdings of U.S. Treasuries at almost 100 percent of their GDP. WTF?

It is because both are offshore tax havens. We suspect much of Apple’s cash hoard is held in Treasury securities domiciled in Ireland and counted in the data, for example. The Cayman, with an economy of only around $2.5 billion, is a haven for many of the world’s hedge funds.

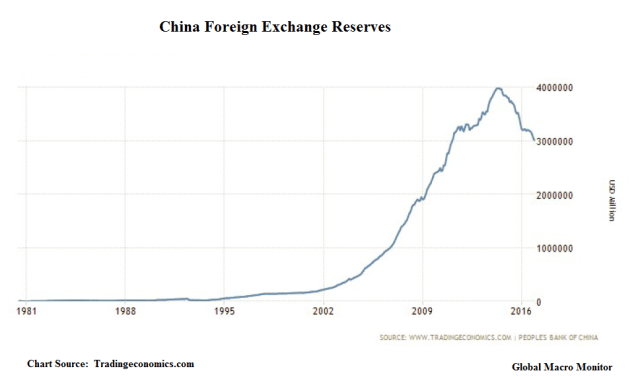

China

China has recently slipped from the top foreign holder of Treasury securities to second place. This could be from the country’s desire to diversify or due to forced selling as the result of the capital flight currently taking place in the country and the loss of almost $1 trillion in FX reserves over the past few years as authorities intervene in the FX market to stabilize the Yuan. We, along with most, believe it is mainly due to the latter.

Trump Fiscal Policy and the Current Account Deficit

If President Trump succeeds in implementing his proposed tax cuts and $1 trillion infrastructure spending plans, the U.S. current account deficit, by definition, will, once again, balloon as net public savings will decline and, we believe, will be complemented by a decline in net private savings as business investment and private consumption increases. This is the simple national income identity,

(S-I) + (T-G) = (X-M)

(S-I) is the ‘private savings balance’ or the difference between private sector savings (S) and investment (I); (T-G) is the ‘government balance’ or the difference between tax receipts (T) and all government expenditure (G); (X-M) is the difference between exports (X) and imports (M) and is usually called the simple ‘current account balance’. –

President-elect Trump doesn’t like trade deficits and we suspect he will be perplexed by the continued deterioration of the current account deficit caused by his macro policies. This risks that his administration may implement even greater international trade distortions to try and reduce the trade deficit.

Recycling of the Current Deficit And Greenspan’s Bond Market Conundrum

The large deterioration of the U.S. current account deficit, starting in the early 1990’s (note also the deterioration in the Reagan years) coupled with yield-seeking capital sent a boatload of dollars into the global financial markets.

During most of the decade, the emerging countries were recipients of much of the dollar flows and most allowed their currencies to appreciate as the dollars flowed in as it helped repress domestic inflation.

Emerging Crises of the 1990’s

After the Mexican, Asian and Russian financial crises of the 1990’s, all rooted (not so much Russia) in external account imbalances, the emerging markets took to heart the harsh lesson of rapidly appreciating currencies. They moved to intervene in their foreign exchange markets to deter currency appreciation, buying the excess dollars being pumped into the global economy as the U.S. current account deficit and international capital flows continued to accelerate after the turn of millennium

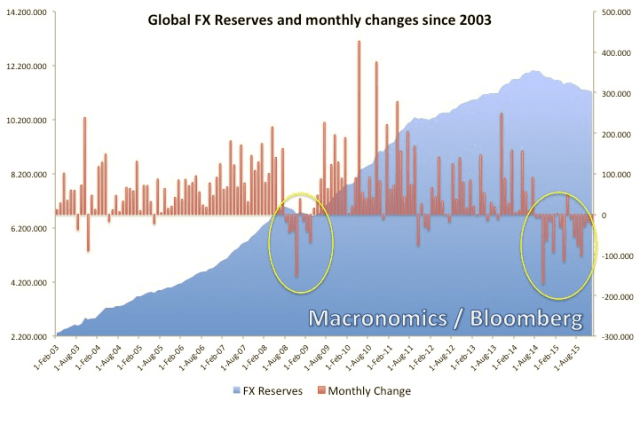

Massive Build Up in Global FX Reserves

The result was a massive buildup in international foreign exchange reserves and the recycling of those reserves back into the U.S. financial markets, particular, official holdings of U.S. Treasury securities. This led to Alan Greenspan’s “bond market conundrum“, i.e., the Fed’s inability to affect long-term interest rates.

The former Fed chairman blames this, and not excessively loose monetary policy, as the root cause of the low-interest rates that drove the credit and housing bubble and subsequent 2007-08 financial crisis.

A Repeat of the 2000’s?

So, is what’s past prologue? Is the same scenario of the 2000’s about to repeat itself? It may rhyme, but we don’t think so.

If President Trump gets his way and his stated policies are passed and implemented, the national income identity — (S-I) + (T-G) = (X-M) — shows the U.S. current account deficit will deteriorate unless private savings increases, which we do not expect. In fact, the Trump plan is betting on business investment picking up.

The global economy will, once again, be flooded with dollars, which will likely be recycled back into the U.S. financial markets.

We think this recycling of capital flows will be even greater than in the 2000’s as it will include some of the $10 trillion-plus stock of the past build up in foreign exchange reserves as capital flight in many emerging markets will flee to the U.S. as real rates rise, relative tax rates change, and global trade barriers increase.

That is, similar to what we see in China, capital flight forces authorities to intervene in their foreign exchange markets to smooth out currency fluctuations, forcing them to sell off official reserve assets, such as Treasury securities. The private sector uses these proceeds either to increases consumption or invests the proceeds in foreign assets, such as real estate and the equity and bond markets. The transfer of official reserve assets to the private sector, on the margin, should result in higher inflation.

Fed Panic

The result will be a highly or overly liquefied U.S. financial system that will initially bolster asset prices, the dollar, economic growth and inflation.

The overheating of the U.S. economy will eventually cause panic in the Fed as the FOMC realize they are way behind the curve, policy rates are much too low, and monetary policy much more complicated due to international capital flows, the size of the Fed’s balance sheet, and the massive stock of excess reserves in the banking system. Just as monetary policy was compromised and complicated under Greenspan’s “bond market conundrum.”

Interest rates are currently much too low if the Trump fiscal policies have any reasonable probability of being implemented. We don’t see many analysts addressing or speaking to these second and third order effects of Trump’s fiscal policy as we are here.

And one reason why we expect such a scenario is because nobody is expecting it!

The End Game

But, here’s the rub. Will a Republican Congress allow a Republican President to run massive budget deficits? Our scenario is highly dependent on an emphatic yes. If not, we will have to reaccess.

Our scenario will take some time to unfold as policies are debated and will certainly not be implemented on Inauguration Day and the impact on the economy will have lags. As the U.S. economy moves into greater internal and external imbalance over the next few years, however, new bubbles and financial distortions will be created. Enjoy the ride.

How it all ends is anybody’s guess.

Our instincts? In tears.

Could be wrong. Wouldn’t day trade it.

Stay tuned.

“We think this recycling of capital flows will be even greater than in the 2000’s as it will include some of the $10 trillion-plus stock of the past build up in foreign exchange reserves as capital flight in many emerging markets will flee to the U.S. as real rates rise, relative tax rates change, and global trade barriers increase.”

I would argue that this stock that has built up has already “fled” to the US via central banking intervention in fx markets and US treasury purchases.

That is an excellent point. I guess reserves will decline and find there way to other assets rather than treasuries.

Such as Chinese capital flight finding its way into real estate. We should see a turbo charged dollar.

I made an update based on your comments, Gianpaolo. Thank you very much.