Summary

- Another fugly week for stocks. It’s really shaping up to be a Trapper John year — full of bull and bear traps making it difficult for traders to make money. The ‘bots have won, folks

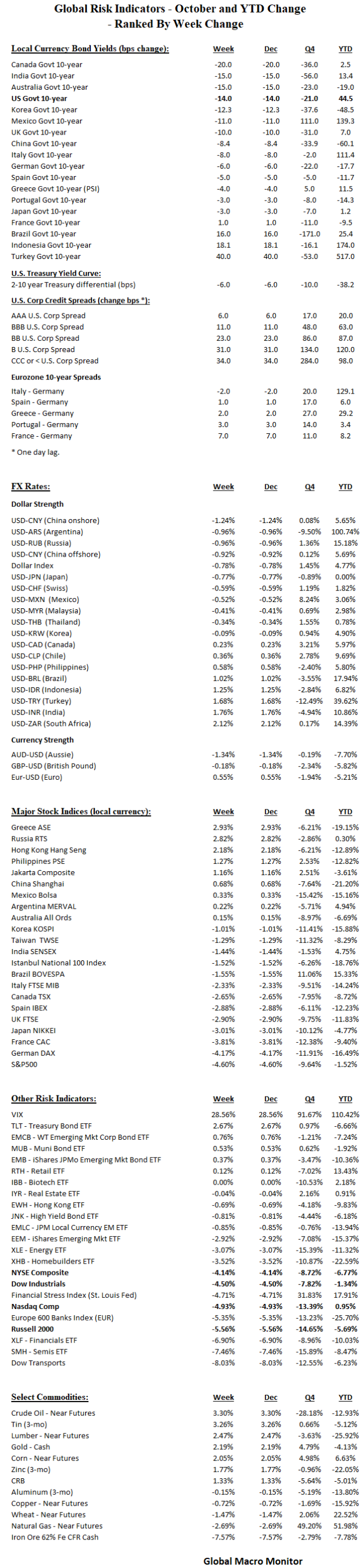

- Transports down over 8 percent for the week, which has only happened 21 weeks in the past 70 years, of which 12 have occurred in the new century. The last time was during the European Debt Crisis in 2011

- Yields are starting to come in over worries about the economy. We think the Fed’s cave to the president’s pounding was a mistake, sent a bad message and confused the markets. The funds rate is still negative in real terms. Let’s see how inflation comes in this week

- The flattening yield curve, which is highly distorted by past monetary action and the Treasury front loading new issuance, may cause a self-fulfilling prophecy as so many in the market still, mistakenly, in our opinion, use it as a signal as the economic health of the nation. Viable economies usually don’t “fall out of the sky,” which begs the question, “is the U.S. economy viable” or excessively dependent on asset markets?

- U.S credit continues to have a horrendous Q4

- The Dollar index a tad weaker. EM currencies still adjusting to their wild “summer of l

ovevolatility” - G5 stock markets led the equities lower last week

- Crude stabilizing. Iron Ore was pounded last week

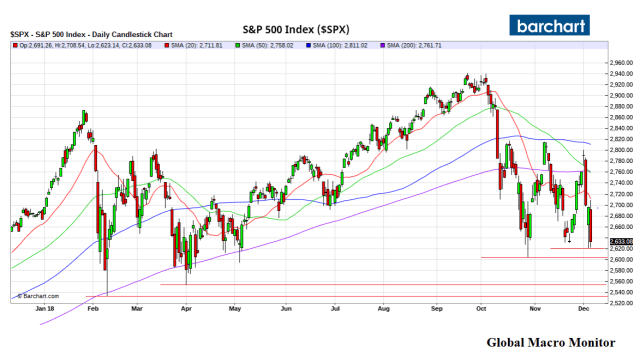

Commentary: Feels like the S&P has traveled a million miles 1.61 million kilometers this year. Two 10 percent corrections this year and don’t yet count out another. The S&P sits at a critical level after testing the 2621-23 on Thursday and Friday. If that level doesn’t hold, and we don’t expect it to, the Q4 correction low at 2603 is a 90 percent probability, which, if that breaks, brings the 2018 low at 2532, about 4 percent lower, in play.

You knew this type of price action in 2018 was coming.

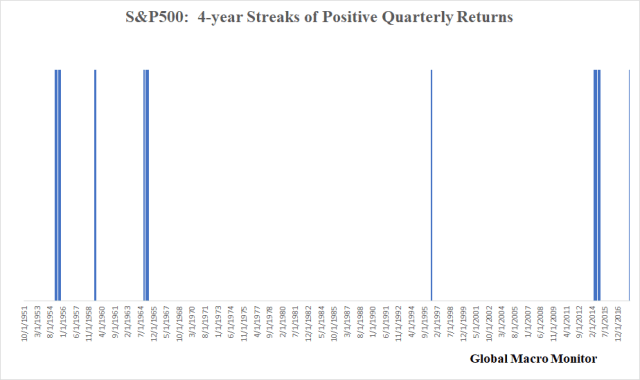

Going into Q1, the S&P500 had delivered positive returns for 16 consecutive quarters or four straight years. The chart illustrates how rare the streak has been over the past half-century.

Our Global Risk Monitor illustrates that 2 of the 4 quarters (2nd and 4th) in 2018 will deliver negative returns.

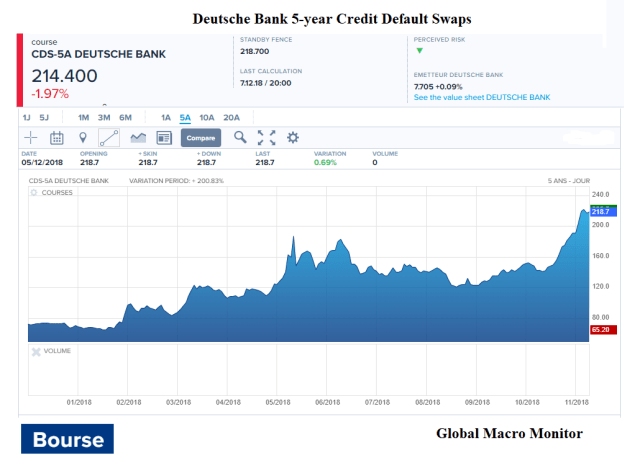

What to watch: Aside from the key S&P levels, the BREXIT vote on Tuesday, U.S. inflation mid-week, Super Mario and the ECB on Thursday, which is big as QE is set to end in Europe, and Deutsche Bank stock making new lows. We expect the term “Counter-Party Risk” to become all the rage of the market experts into year-end as Deutsche’s stock circles the drain.

Sounds like the German government is preparing for a bailout of DB. Merging two weak banks will require a significant injection of capital. Who will, if any, be bailed in?

Upshot: Don’t like it here. Think we are in a bear market. Bears markets do bounce hard, however, as we have seen time and time again this year.

Capital preservation folks. Scalpers and traders can have this market.

DB Stock Making New Lows and CDS Blowing out – Counter-Party Risk

Scary. Note: one million miles equals 1,603,400 kilometers.

>

Thanks for that, Larry. Transposed the denominator.