NEW YORK (AP) — The head of the nation’s second-largest bank said consumers are spending “at a faster rate” than he’s ever seen but he remains concerned about how inflation and supply-chain issues will influence the economy going into the winter. – Brian Moynihan, CEO, Bank of America

The above statement by Brian Moynhan jibes with our view and posts over the course of 2021.

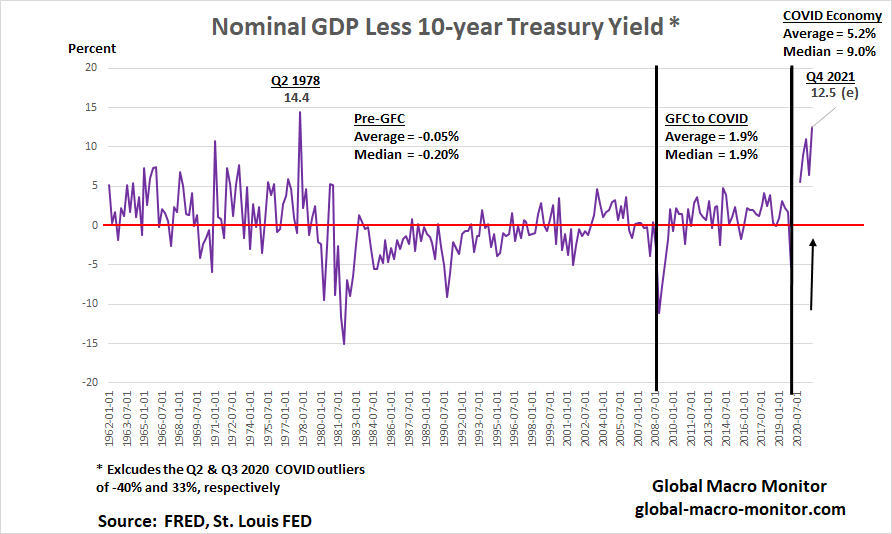

In our last post, a bit too wonky, we tried to convey how out of whack the bond market is with the economy. We have redone the chart to rid it of the COVID outliers and it more clearly illustrates the historic difference beween nomimal GDP growth, which should come in aournd 15 percent in Q4, and the 10-year note yield. The differential this quarter will come in only second to Q2 1978.

The data clearly illustrate the odd and unprecedented times in which we live. The stock market is going up, however, so “all is calm, all is bright.” Am I right?

Moreover, we have a sense the market is coming around to what we have been saying over the past few months: the economy is overheating and the Fed has some very heavy lifting to do.

We are reposting our chart on retail sales, which shows how far out of line current spending is with its pre-COVID trend.

We also maintain the primary factor causing inflation and the supply chain debacle is excess demand, the result of too much stimulus not just from the Fed but all the major central banks and governments.

The Fed may have to surprise on the hawkish side tomorrow but we’re doubtful as they don’t have the stomach for the pain it will cause in the stock market.

As Greenspan was in the 2004-07 tightening cycle, we suspect this Powell tightening will be way too slow and not bold enough.

Our bet is if the S&P craters, Powell will cave. Hence inflation will be a more permanent feature or the U.S. economy going forward.

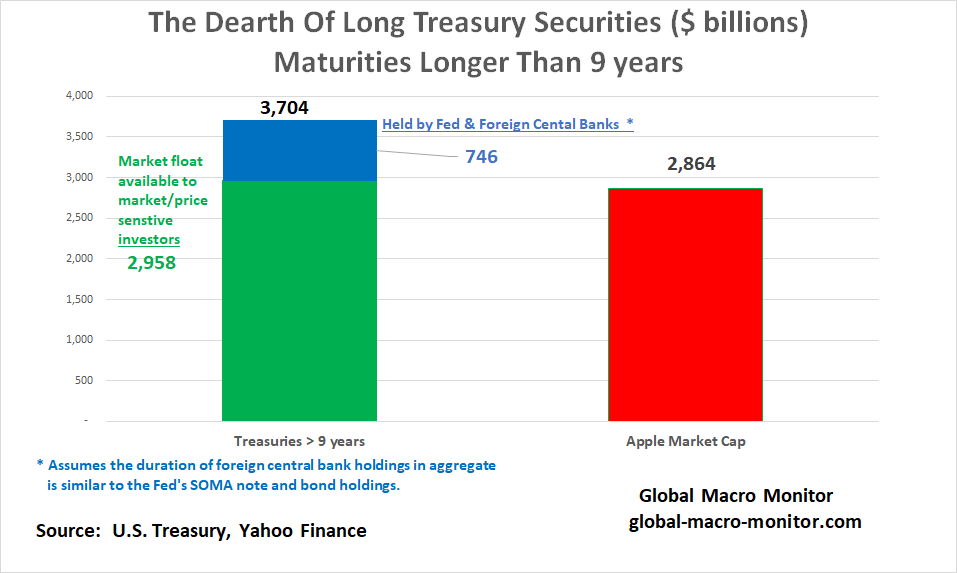

The dearth of longer maturity Treasury coupon securities has significantly distorted the yield curve.

Reverse Operation Twist

The Fed should also consider a reverse Operation Twist, where they sell or announce they are going to swap their long-term Treasury notes for shorter maturities. This would steepen the yield curve and slow down demand in the bublicious housing market and, more important stifle the market yapping that the world is coming to end because the yield curve is flattening or inverting.

Lack of price discovery in the bond market is going to become a very real problem for monetary policymakers throughout the world.

Go to 20 seconds in to hear Moynihan’s comment on the consumer.