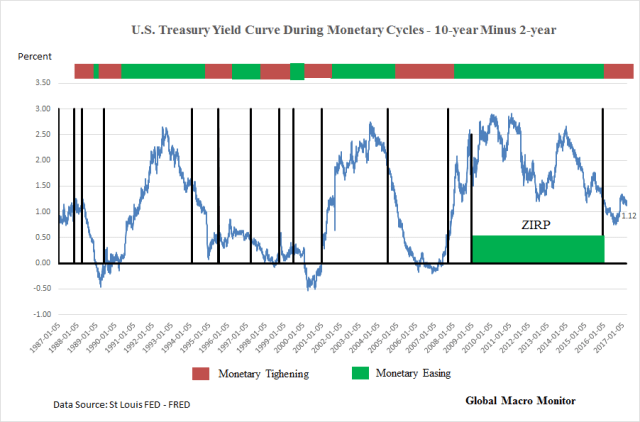

The 10-year minus 2-year yield spread closed today at 1.12 basis points, back to the election day low. All the steepening of the yield curve since the election day, widening out to 1.34 in December, has vanished.

We don’t think this reflects anything to do with a slowing global economy but is more a reflection of a broken bond market. Too many shorts and a structural shortage of risk-free bonds engineered by quantitative easing.

The following is a long-term chart and thus hard to recognize the short-term flattening.