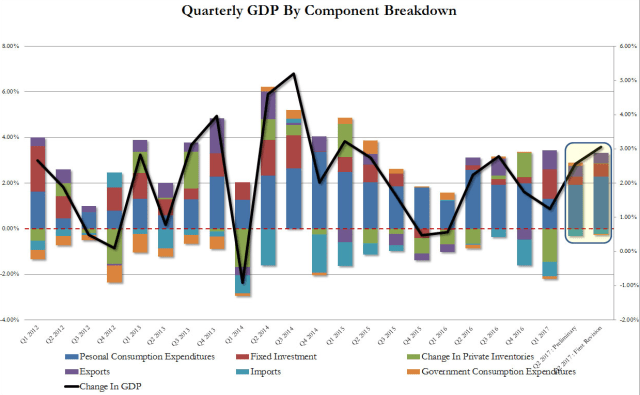

The BEA revised Q2 GDP up this morning,

Current-dollar GDP increased 4.0 percent, or $189.0 billion, in the second quarter to a level of $19,246.7 billion. In the first quarter, current-dollar GDP increased 3.3 percent, or $152.2 billion. – BEA

This makes us think the Fed is waaaay behind the curve. Markets are much too complacent about the potential for inflation to heat up and as we suspect, no, strongly suspect there may be some measurement problems with the data. Just as some suspect the same with the GDP data and now look to the labor market as a better gauge of economic activity.

Where is the labor going to come from to rebuild Houston, by the way?

The cheerleaders out en masse today with their Goldilocks scenario and talk.

Nonetheless, stock and risk positive in the short term.

A better way to gauge the tightness of monetary policy is to compare nominal interest rates with nominal GDP growth. An old rule of thumb is that, when interest rates are higher than the rate of growth in nominal GDP, monetary policy is restrictive; when interest rates are lower, policy is expansionary. A crude way to understand this is to see, say, America’s nominal GDP growth as, in effect, the average return from investing in America Inc. If the average return as measured by nominal GDP is higher than the cost of borrowing, investment will expand. – The Economist, October 4, 2001

Nominal interest rates and economic activity are probably more divorced from reality in the Euro zone, though the stronger euro acts as an effective tightening of policy. Draghi is going have to do a nice little dance to get through this one. Another, “whatever it takes” speech.

The FocusEconomics panel upgraded its outlook for the Eurozone again this month, after raising it in the two previous publications. GDP is seen growing a robust 2.0% this year, a notch above last month’s projection, thanks to a firmer labor market, vibrant investment and healthy external demand. Next year, growth is seen as slightly more modest at 1.8% as tailwinds wane.

– Focus Economics

Add the above concerns to our event risk checklist for a stinging, temporary market disruption, sometime around October. That is an unexpectedly sharp rise in market interest rates, probably beginning in Europe that spreads to the U.S..

Another positive return in September for stocks, sprinkled with some volatility, will also lead to even higher valuations and overbought conditions setting the stage for an October correction.

The move to passive investing with the market now on effective auto pilot, steered by trading ‘bots developed and raised in an age of BTFD quantitative easing, a decent sell off now requires a plethora of catalysts, which we do think are coming in October.

One contrarian caveat? Lots of fast money now bearish and hoarding cash.