Summary

- Turkey 10-year up almost 300 bps in August

- Brazil 10-year up 102 bps

- Italy 10-year up 52 bps

- U.S. & German 10-year 10 bps lower

- US credit spreads relatively stable in August

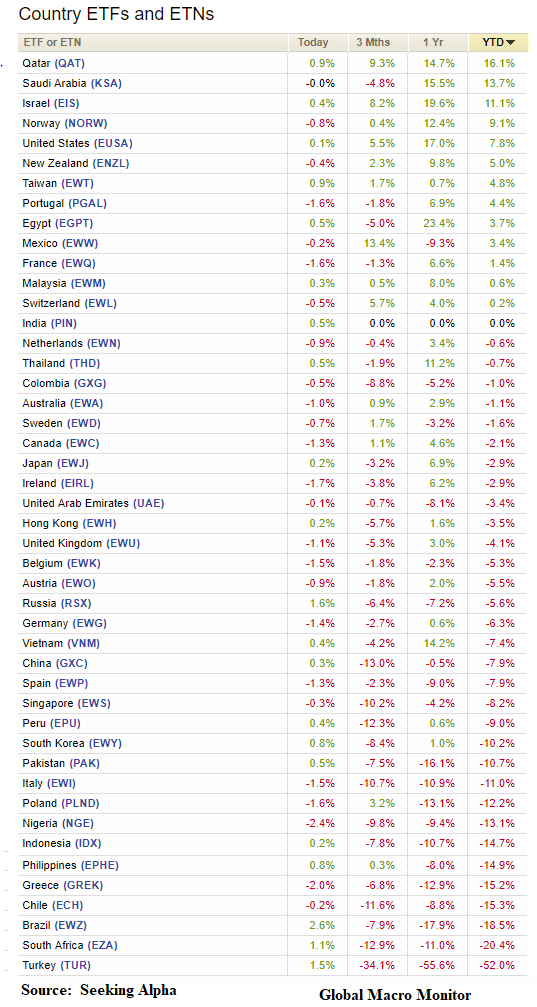

- Argentina peso crashes

- Turkish lira crashes

- South Africa significantly weaker

- Dollar index up about 1 percent in August

- Swissie stronger

- Aussie weaker versus the dollar

- S&P500 outperforming global markets, up 3 percent in August

- Italy stocks hammered 9 percent

- Euro bank index down over 7 percent on EM fears

- Corn and Copper continue to be weak

Summary: Tough month for the emerging markets. The capital flight from EM is coming back to the U.S., fueling the S&P500 and the haven flight to Treasuries. The Fed continues to tighten the vice on global liquidity, and there no let up in sight.

We are steering clear of EM. The probability of a major market disruption in emerging markets, ala 1995/1997/1998 is increasing.

The table below shows the sum of the monthly return on the S&P for July and August totaled 6.63 percent, putting 2018 in the 84th percentile of July/August returns since 1950. Impressive.

We were wrong in our bearishness in August for U.S. stocks, but NFW do we chase the market here. Of the years which have had similar July/August performances or better, the average September return is -0.1 percent; median return is -0.3 percent, and only 36.4 percent of the Septembers generated positive S&P returns. That is the conditional probabilities do not favor going long.

Interestingly, 45 percent of the 11 years where the July plus August S&P500 returns were higher than 2018 were during midterm election years. Statistically significant given that midterm elections only occur during 25 percent of total annual observations.

Given the current political climate, extremely low polling for the incumbent president, it does look like a 1994 rout is in store for the party in power. In 1994, the Democrats lost both the House and Senate as Newt’s “Contract with America” was ushered in with the Republicans capturing 54 congressional seats, eight Senate seats, and ten governorships.

The 1994 political rout took place in spite of a strengthening economy, which was beginning to accelerate — Q2 1994 GDP growth came in at 5.5 percent, with the three-quarter moving average GDP growth the highest in 10 years. The S&P500 was up around 2 percent going into September 1994.

The index was down close to 3 percent in September 1994, but the markets were pregnant with the dot.com bubble and on the eve of a historic run.

Don’t see the parallels today as the political shift will be far less market-friendly than the results of 1994 midterm and valuations are already at extremes.

The upshot? Don’t depend on the economy to save you during the midterms.