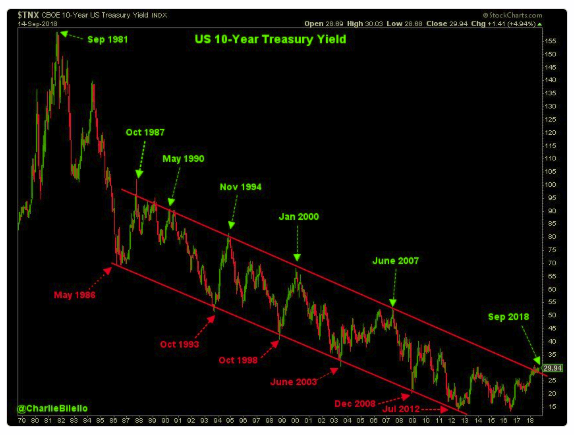

Great chart from Charlie B. He asked 3.5 or 2.5 percent?

We say beeline to 4 percent, when the rate breaks 3.13 percent, and quicker than the market believes.

It’s been 10 years since Lehman, nominal GDP is growing close to or over six percent (which, in normal times, the 10-year trades around nominal GDP growth), and inflation hovers at the 3 percent level, yet real long rates are zero to negative? Come on, man.

Central banks own the yield curve and could give a rat’s ass if they are making money. But that is starting to change.

Yes, record shorts in Treasury futures. But that has been the case for almost the entire last year. In early February, for example, the stock market experienced its biggest spike in volatility in history.

What did the 10-year rate do? It rose several basis points. That is important information, folks.

All bets off given a major financial or macro shock.

There are many structural forces working against keeping long-term rates low and the term premium suppressed. We will be out this week with our work. Promise.

Source: @charliebilello

Now I see it. Thanks. John