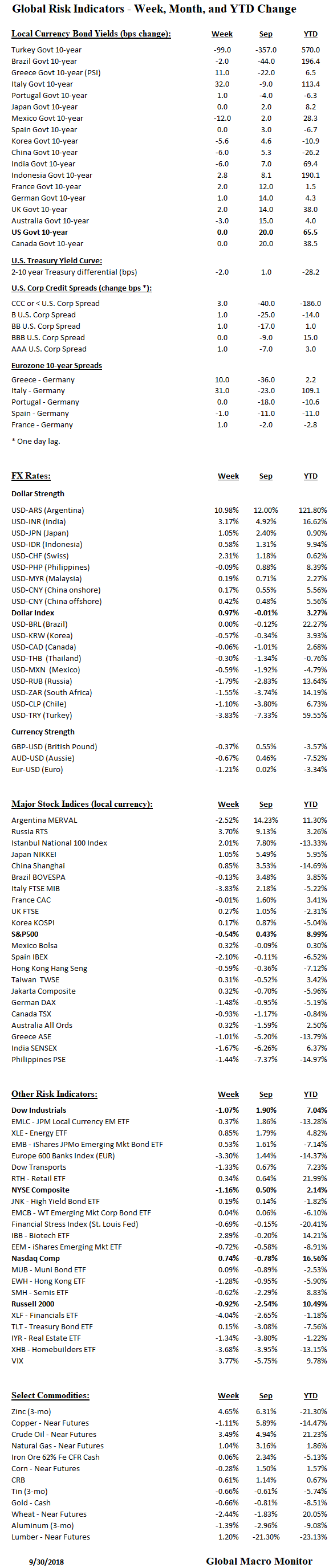

Summary

- Q3 saw major carnage in the emerging markets with Argentina, Turkey, and India’s currency taking major hits

- Big blowout in 10-year yields, though Turkish bonds rallied came in over 350 bps in September

- The S&P was flat up 0.50 percent in September and 7.20 percent in Q3

- U.S. credit remains strong

- Euro periphery bonds had a good month, however, a tough close on Friday on worries over the Italian budget

- The Nikkei up 5 ½ percent in September

- China stocks bounced back

- Indian and Philippine stocks down over 5 percent on the month

- Dow up 1.9 percent, Russell down 2.5 percent in September

- Crude oil futures up 5 percent on its march toward $80

Summary: U.S. stocks and credit remain well bid. U.S. equity market is bolstered by the New Supply-Side, that is restricted supply as corporations continue to buyback shares, and a lack of real sellers. Traders and ‘bots get short and are forced to cover as no real selling eventualizes.

Watch the lower-end of investment grade corporate credit as that is where the real supply is, and will probably come out first. We fully expect interest rates to continue their march higher. Emerging markets are tradeable on both sides, but expect pressure to continue as the Fed and Treasury continue to hoover up all the hot money in sight.

NAFTA deadline in a few hours. Looks like another Potemkin deal gets done, which should lather up the markets for a few days.

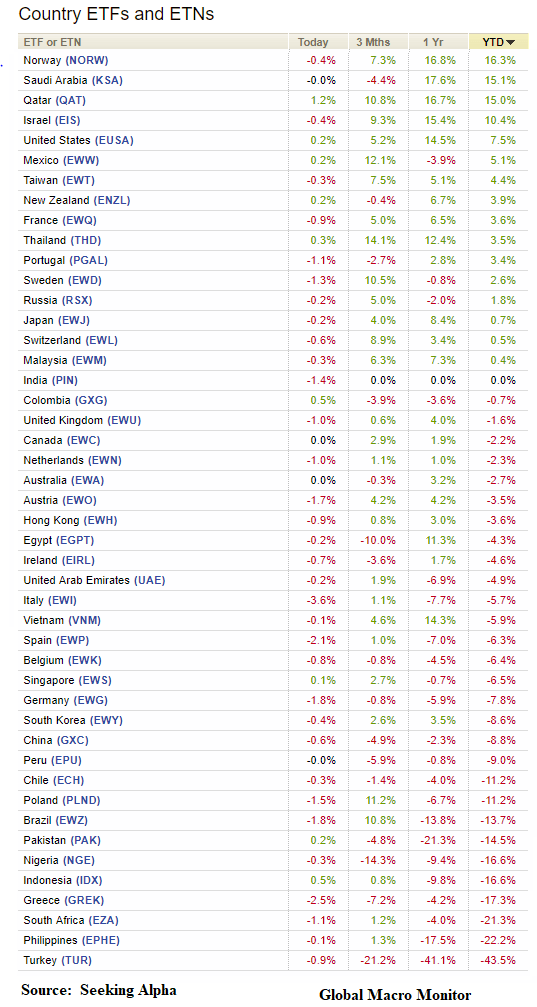

Ranked by YTD US$ return

Ranked by September US$ Return