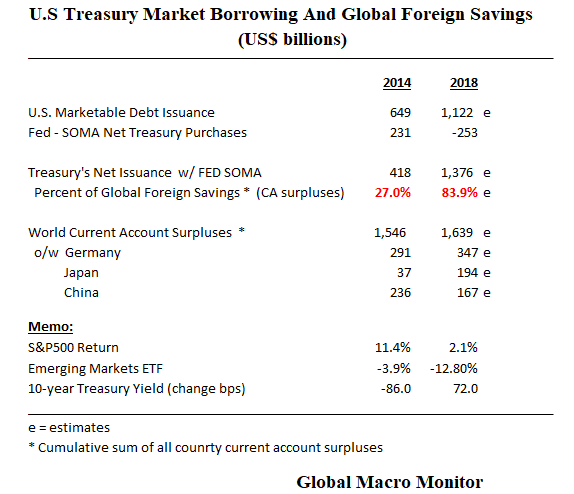

We were curious about how much U.S. Treasury market borrowings have increased relative to global foreign savings and whipped together the table below.

We define global foreign savings here as the cumulative current account surpluses of all the world’s surplus nations.

The sum of the world’s economies current account balance should equal to zero. That is not the case with the actual data, however, due to measurement errors. Some argue it is because the world runs a current account deficit with Mars. Wonder what kind of tariff will fix that?

Nevertheless, the data are quite shocking.

In 2014, for example, the U.S. Treasury issued $649 billion in marketable debt, of which the Fed, during QE3, bought more than 33 percent in the secondary market. The net issuance after QE totaled only 27 percent of the world’s foreign savings. Note this does not include domestic savings, which is the bulk of savings. Moreover, one should not conclude the Treasury absorbed all of the world’s foreign savings.

Our analysis should be used to benchmark Treasury market borrowings relative to savings and the potential stress it puts on the world’s capital flows and markets.

In 2018, based on the January through October realized data and our estimates for November and December, the Treasury will issue $1.12 trillion of marketable debt. The U.S. government will also repay over $250 billion to the Federal Reserve as they run off their SOMA portfolio. We estimate the net pressure on the capital markets will be $1.4 trillion, or 84 percent of global foreign savings, more than triple the 2014 level.

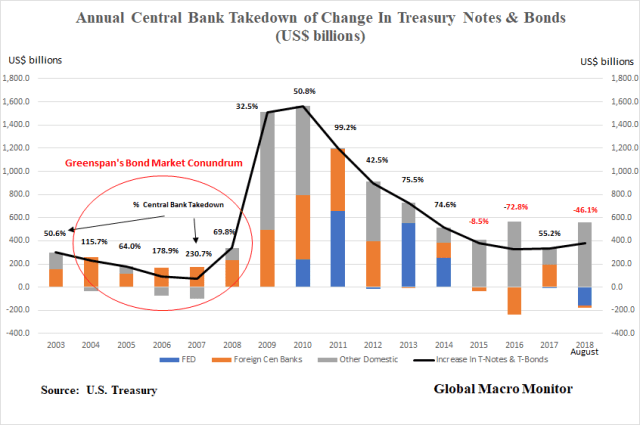

These data points are relevant given the U.S. government has been so dependent on foreign savings during the last 15 years to finance its budget deficits (see chart below). It also helps explain the pressure on emerging markets this year as the U.S. public sector borrowing requirement (PSBR) is crowding out capital flows to to the rest of the world and other markets.

Maybe this why markets are beginning to feel so tight even as global policy real interest rates remain at near or below zero.