Our beloved Carol K. starts a new risky treatment this week to try and conquer her serious illness. Everyone at GMM and all of our readers are with you, girlfriend!

Can’t wait to hear the Chairman justify zero rate policy and deficit monetization with inflation roaring at > 5 percent. It would be entertaining, if it weren’t so damaging.

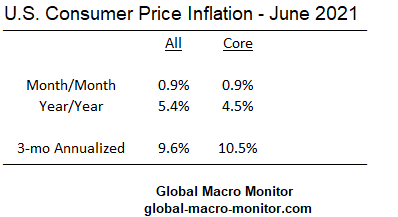

….CPI prints > 4 percent in May and you heard it here first. – GMM, April 29th

The past three months of core CPI inflation prints have been big, big, big — 0.9, 0.7, and 0.9 percent, respectively. There is zero “base effect” on these data, folks.

If annualized, as the GDP prints are, the economy hasn’t seen this type of three-month core inflation since 1981.

Sure, some have to do with the reopening, and some not.

Our priors are policymakers have distorted too many markets, over-stimulated the economy, and pumped too much high-powered money into the global economy. China rejoined the party last night.

My Lobster Roll Restaurant

We keep waiting for a new Lobster Roll (rare in Wine Country) restaurant to open up on my street, for example, and it’s taking forever. I spoke to the owner yesterday, who said he couldn’t find workers.

What the Fed believes is a demand problem to recover all the jobs lost to COVID is, in reality, a supply problem. Put the academic models down and go talk with the small businesses.

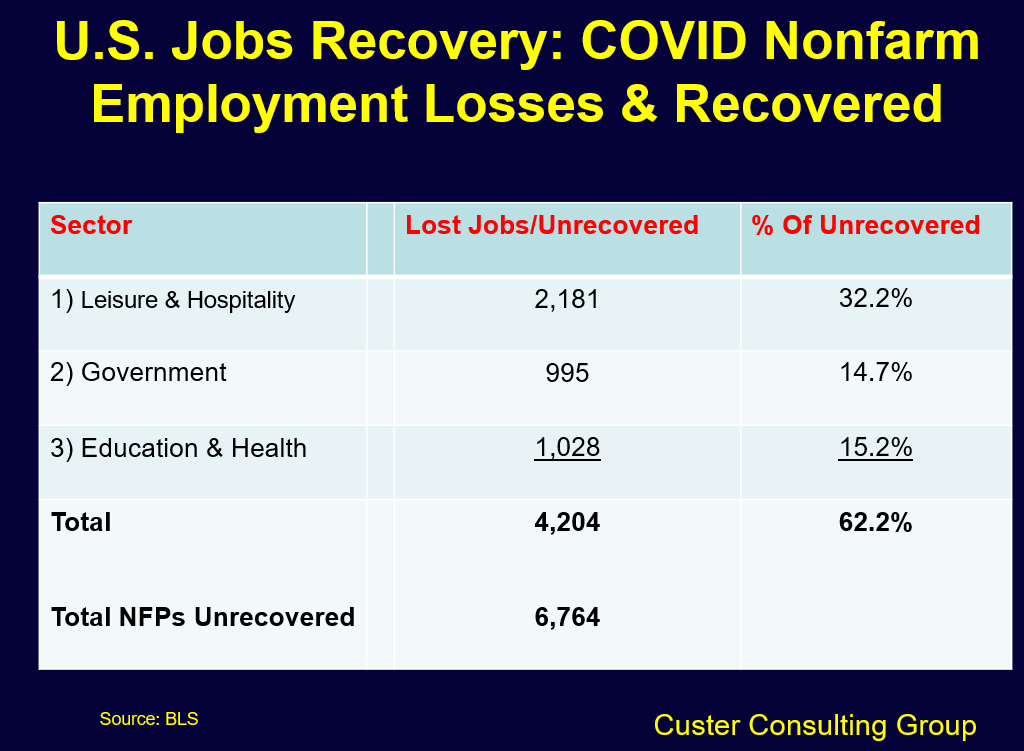

We maintain there is a shortage of labor at the given wage rates for much of the leisure and hospitality sector, which makes up about 12 percent of nonfarm payrolls yet 32 percent of unrecovered lost jobs lost to COVID. The jobs aren’t returning for lack of demand, mitigated by easy monetary policy. Still, most of the lost jobs are in three sectors, where we suspect will have to pay higher wages and benefits to attract workers.

We support higher wages if small businesses, which employ almost half the labor force, have the margins to pay and the ability to improve the productivity of their workers. Otherwise, they will pass the wage increases on with higher prices or shut the doors.

I believe we are witnessing that now.

Upshot

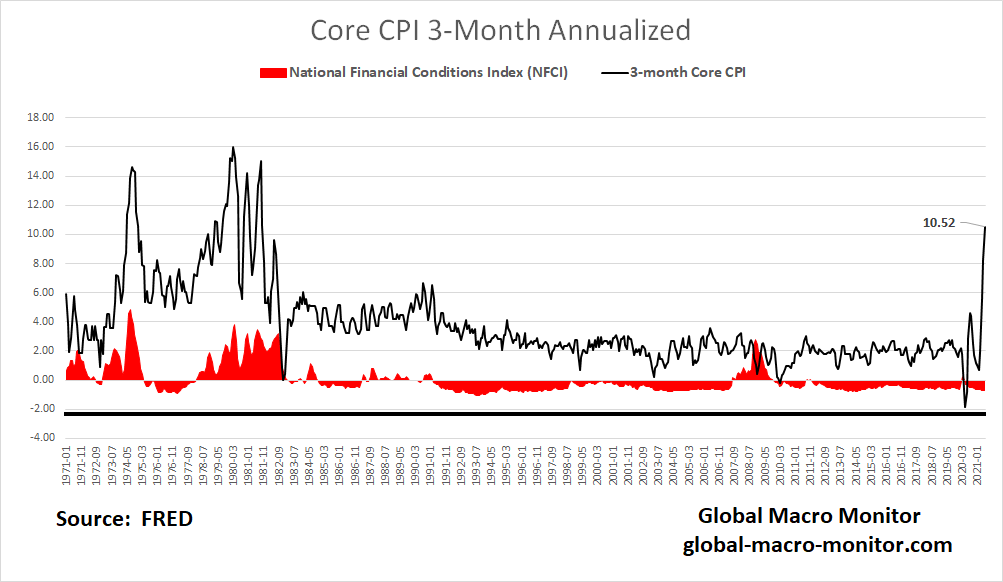

When today’s inflation print is put into the context of current financial conditions, as measured by the Chicago’s Fed Index, the U.S. economy has never seen this high short-term core inflation with such easy financial conditions, at least in the 50-year data set, we are looking at.

It won’t matter until it does, and then it will matter, and really matter.

Until then everyone’s making money, the Wall Street crowd tells us everything is awesome, and to party like its the 1920’s, maybe right off a fiscal cliff.

Wall Street and the government, who have a vested interested in low inflation prints, will promote the transitory narrative. Seniors and those on fixed-incomes will suffer until their Social Security cost of living increases (COLA) partially make them whole.

We also doubt seniors are buying used cars. Someone should go ask them if their monthly purchasing power is increasing or decreasing.

Markets

The markets?

They’ll get religion but the timing is tough.

When they do, however, and start selling assets, the “D” word, as in deflation will be back in the headlines because that is the kind of asset-dependent economy the U.S. has morphed into, folks.

The Inflation Dialectic

Recall our corner solution analysis on the inflation/deflation debate.

Marx (Karl, not Groucho) was wrong on many things but had a brilliant analysis of how society progresses through conflict, explained by the Hegelian dialectic. We apply it to monetary policy analysis

In the asset-dependent economy, where asset prices need to rise to stimulate demand as wages and income are insufficient to clear the goods market, valuations eventually overshoot, consumers begin to feel like millionaires, and start to spend that wealth.

Goods and service price pressures increase, monetary authorities react — not sure if they can now given valuation and debt levels — by pumping the breaks and asset markets flop. Wash, rinse, repeat.

We concede the wealth effect is much less prominent with the uber wealthy as they have much lower average and propensities to consume than the middle class but the asset markets have a much larger outsized effect than most economists tend to believe. This is being tested in real time with the COVID as real “helicopter money” is getting to the hands that need it and spend it. But inflation…

The thesis – inflation — sows the seeds for the anti-thesis forces – deflation – when monetary policy is perceived to be about to change. From that conflict arises the synthesis, a new and more convoluted monetary policy to prop up assets.

The dialectic is probably coming to an end, however, as inflation ticks up and the Fed is now perceived as the problem and not the cavalry.

Pray for transitory.

Stay tuned, folks.

Pingback: It Matters Now – Markets Get Religion | Global Macro Monitor