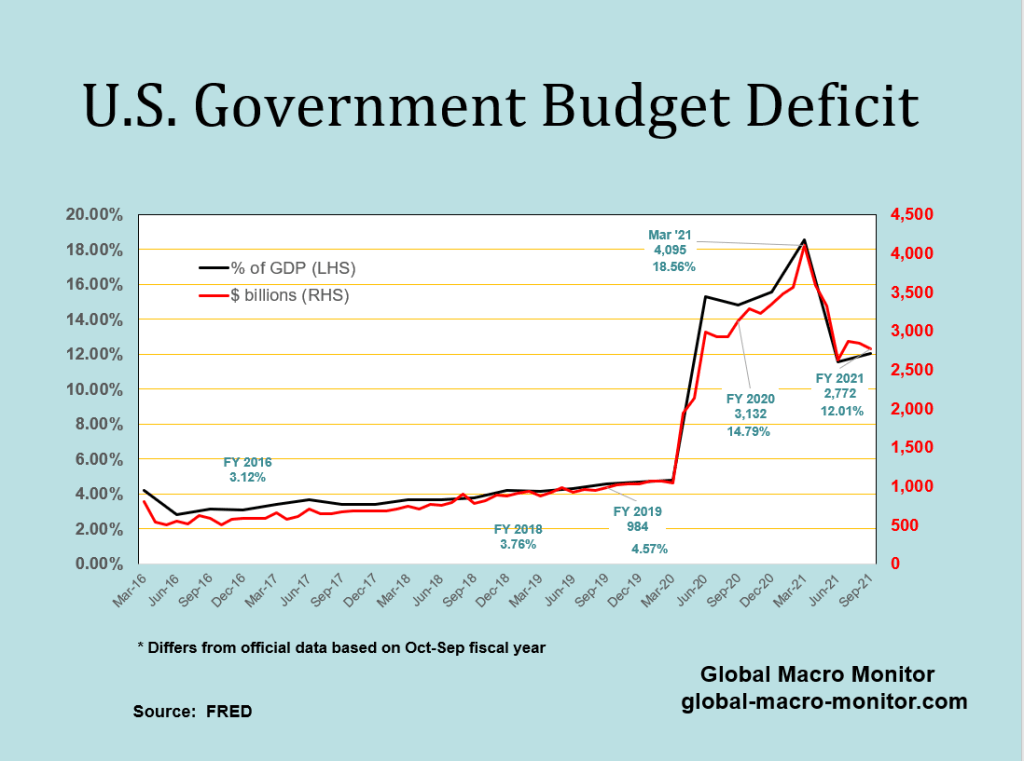

The U.S. Treasury findly released their monthly statement on Friday, which closed the books on the government’s 2021 fiscal year (October to September). The deficit came in at $2.8 trillion (12.0 percent of GDP, based on our Q3 GDP estimate) , a bit lower than FY 2020’s $3.1 trillion (14.8 percent of GDP). Those are some massive deficits, folks.

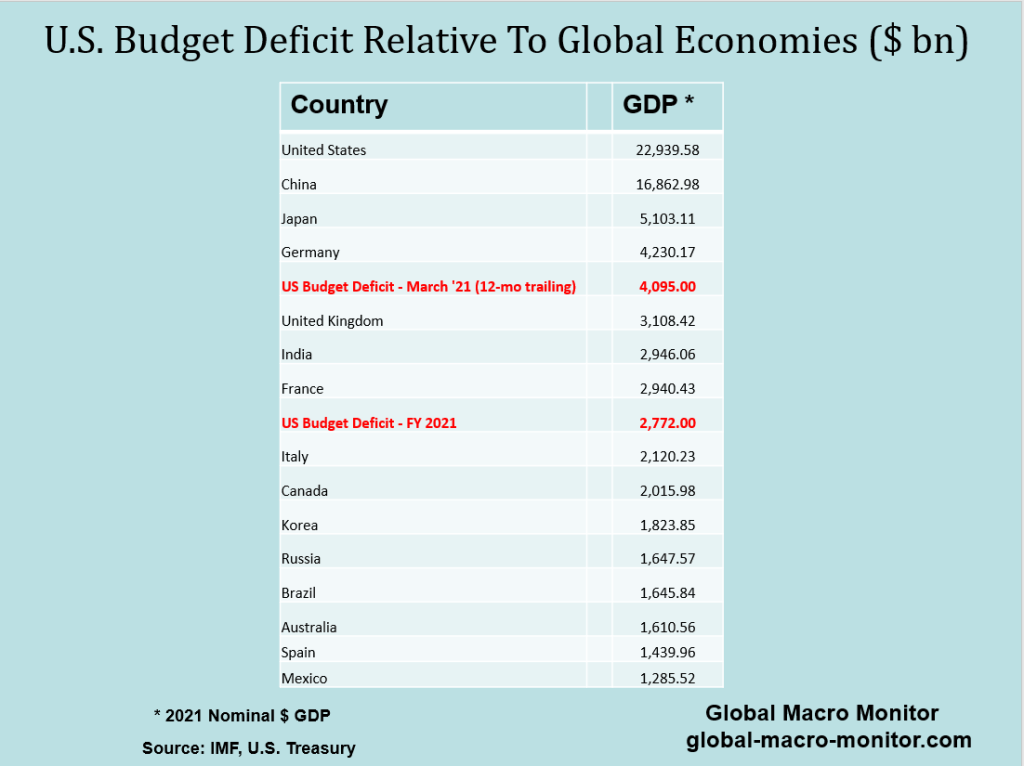

U.S. Deficit Larger Than 95 Percent Of Global Economies

In fact, the FY 2021 deficit was larger than Italy and Canada’s economy, bigger than 185 of the 192 country economies in the IMF’ World Economic Outlook (WEO) database. Take a look at the peak 12-month deficit of $4.1 trillion in March. The March deficit would have made the G5.

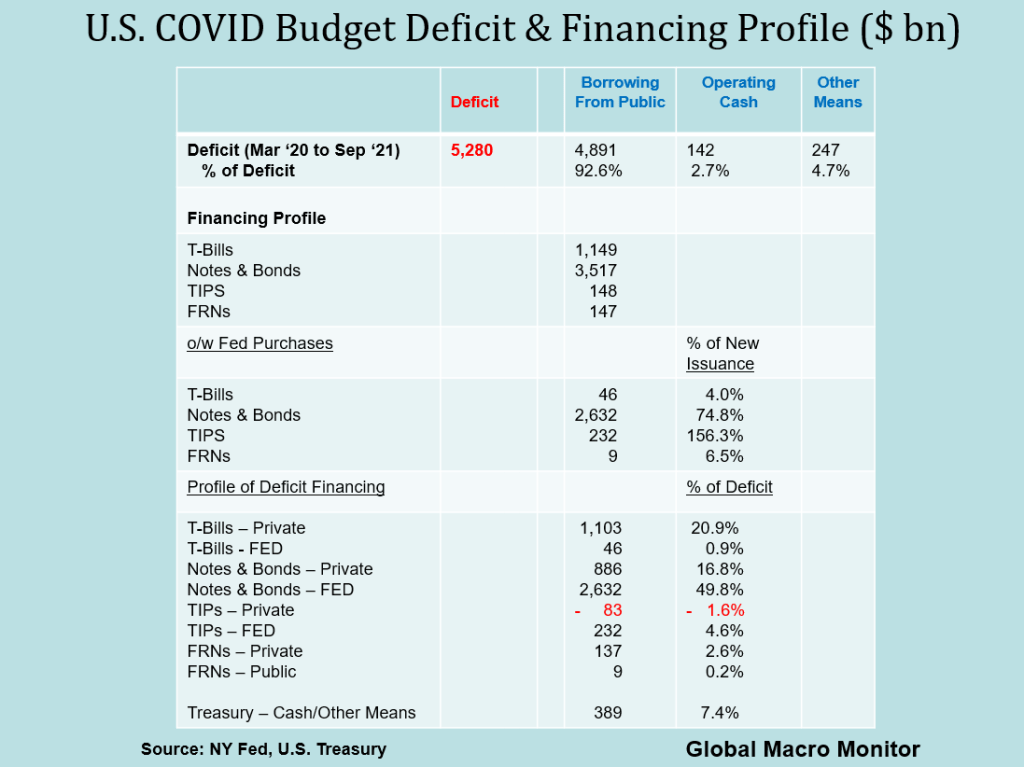

Financing The COVID Deficit

How can the U.S. Treasury finance $5 trillion in borrowing over the past 18-months without spiking global interest rates, crowding out investment and other asset markets, and tanking asset prices? They can’t.

The table below breaks down the financing by several different measures. Check it out.

The bottom line is that 23 percent of the COVID deficit borrowing has been financed by an increase in Treasury bill issuance, easy given the mass excess liquidty on the short-end where the Fed is soaking up over a trillion with overnight reverse repos in order to keep short-term rates positive. Most of that liquidity, by the way, was created from QE, which, by extension, was, in effect, the Fed financing Bill purchases.

Of the remaining $4.1 trillion of non T-Bill debt issuance, 75 percent was taken down by the Fed, albeit indirectly.

No Judgement

There you have have it, folks, T-Bills and the Fed have financed the bulk of the COVID deficit and debt buildup. No judgment, but policymakers are now going to have engineer a soft landing in the economy and asset markets as we approach a fiscal cliff to normalize the budget deficit and tighten up monetary policy.

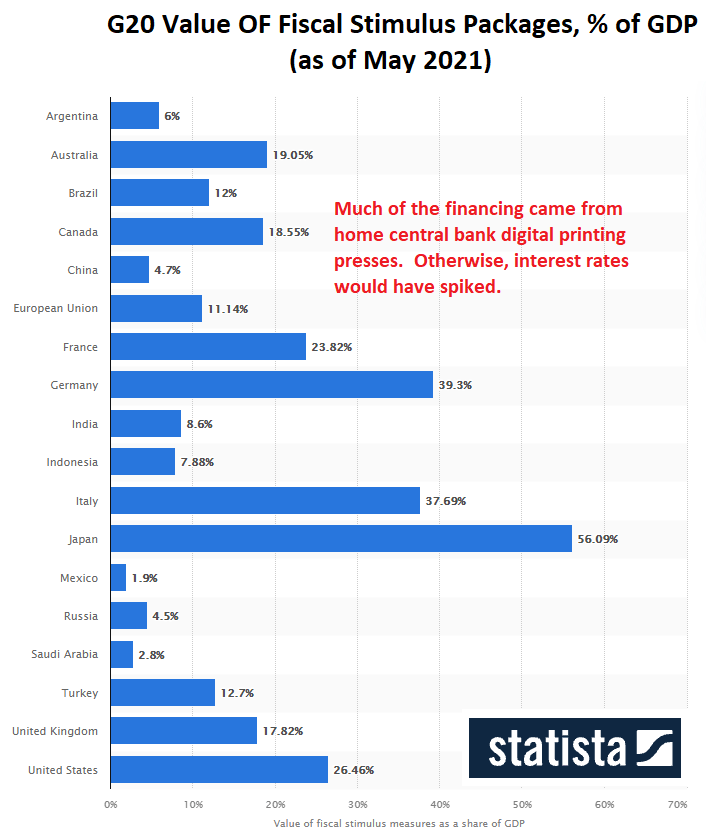

We are not throwing stones as the policymakers saved the world from a global economic castasophe.

We do criticize their continued irresponsible policies as inflation rages and stagflation sets in. It’s not wise, in our experience, to try and monetize supply shocks. We learned that hard and painful lesson by doing so with the OPEC oil shocks of the 1970s.

Deficits and monetization don’t matter? Go ask the purchasing managers up and down the global supply chain, who have been swamped by too much demand, spiking input costs, and parabolic commodity prices.

Narrow window for a soft landing. Stay tuned.

Email us or comment if you have questions.

Appendix

Pingback: The Great Reset: The Bond Yield-Dollar Feedback Loop | Global Macro Monitor

Pingback: The Great Reset: The Bond Yield-Dollar Feedback Loop – Mist Vista