Inflation peaking? Doubt it.

The price of shelter, which is about one-third of the CPI basket, is screaming higher.

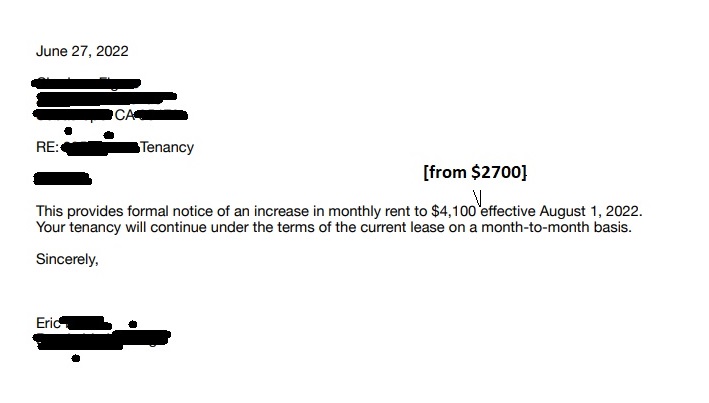

Last month, we wrote about our old baseball buddy, who was slammed with a rent increase.

We caught this article this morning,

Click here for article

Then a friend sent this over earlier today.

She has been levied a 50 percent rent increase! That is frickin’ hyper, folks.

She has been levied a 50 percent rent increase! That is frickin’ hyper, folks.

We hope it’s not a nationwide trend in terms of percent increases lest the country’s homeless rate is about to double.

Where is the supply chain issue here? Anybody?

Housing makes up over 40 percent of the CPI basket, including rents at a little over 7 percent.

The Post-1983 Housing Inflation Measurement To Be Tested

We suspect some strange (as in upside suprises) CPI prints coming as shelter goes vertical. The new methodology (post-1983) of using survey data to measure housing ownership inflation has never been tested in a high inflation environment.

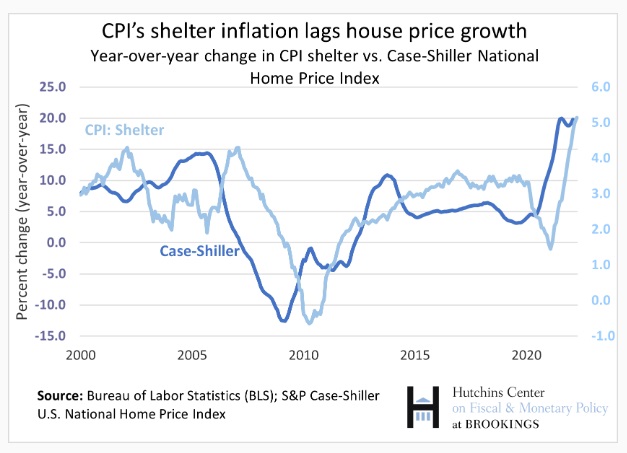

Over time, changes in house prices do predict changes in rents—although the relationship is far from 1 – to-1 and occurs with long lags. Xiaoqing Zhou and Jim Dolmas of the Dallas Fed find house price growth’s correlation with OER inflation peaks at about 0.75 after 16 months; the correlation with rent inflation peaks at after 18 months. – Brookings

Brace for weirdness.

CPI Inflation’s Big Problem: Housing

Updated: Post-CPI release @ 9:12 pm PT, May 11, 2022

But the Fed seems to be learning lessons from its 2021 experience. – NY Times

The Fed is under a lot of heat for letting inflation get out of control, which is now generating super hawkishness even among the most gentle of monetary doves. The scorching is illustrated in the above NY Times headline.

We are reposting our piece from last April 2021, Just In Case, You Think The Fed Has A Clue, in which we questioned the Fed’s economic sanity to keep buying mortgages while the housing market was in a massive bubble.

Bond yields are now spiking, and the stock market suffers because of the monetary authorities’ ineptitude as the economy contemplates a bond and stock market without central banks. The major buyers of Treasury securities since the beginning of the century have now morphed into net sellers in aggregate.

Nevertheless, making monetary policy is difficult, especially in the last few years, so we grant policymakers considerable grace.

Valuations and multiples have to come down as interest rates rise.

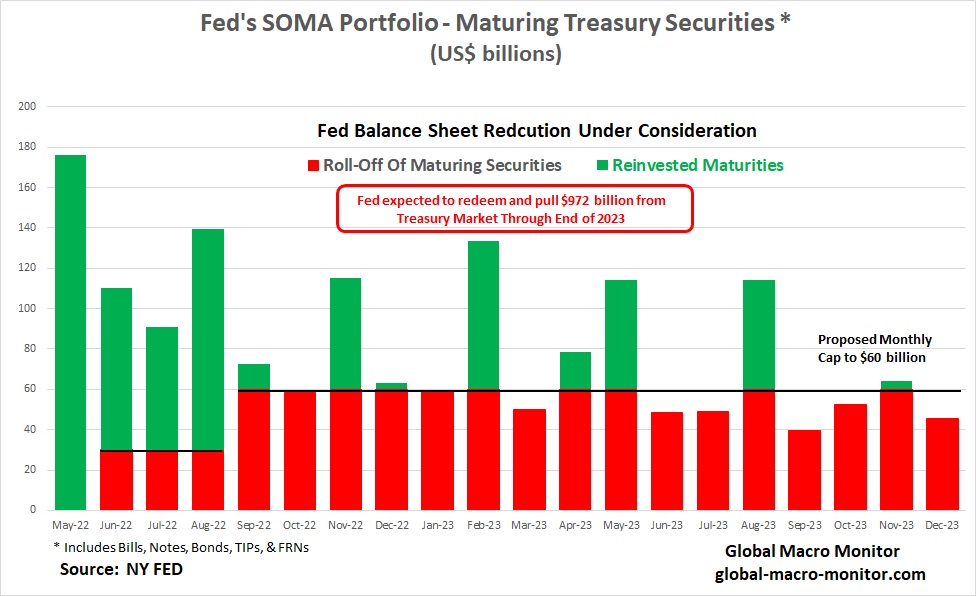

Given the FOMC’s latest statement on balance sheet reduction, we estimate the Fed will be extracting almost $1.5 trillion from the economy throughout 2023, approximately $972 billion from the Treasury market, and a maximum of just over $500 billion in mortgages.

Inflation As The End Game

However, we doubt the Fed and the American body politic have that high of a pain threshold for the subsequent economic and financial pain such a monetary tightening will bring. We, therefore, expect inflation will be the end game but only after, at the very least, a few deflation scares. When the going gets tough, the Fed will default to the mantra of most central banks and monetary authorities throughout history,

Print [debase], baby, print [debase]!

Housing Is Now The Problem, And Its Measurement Is Fatally Flawed

We estimate the Fed bought over $525 billion in mortgages between March 2021 and March 2022. During this period, the housing market was in Fuego with FOMO panic buying, driving up the National Price Index by 18 percent during the same period.

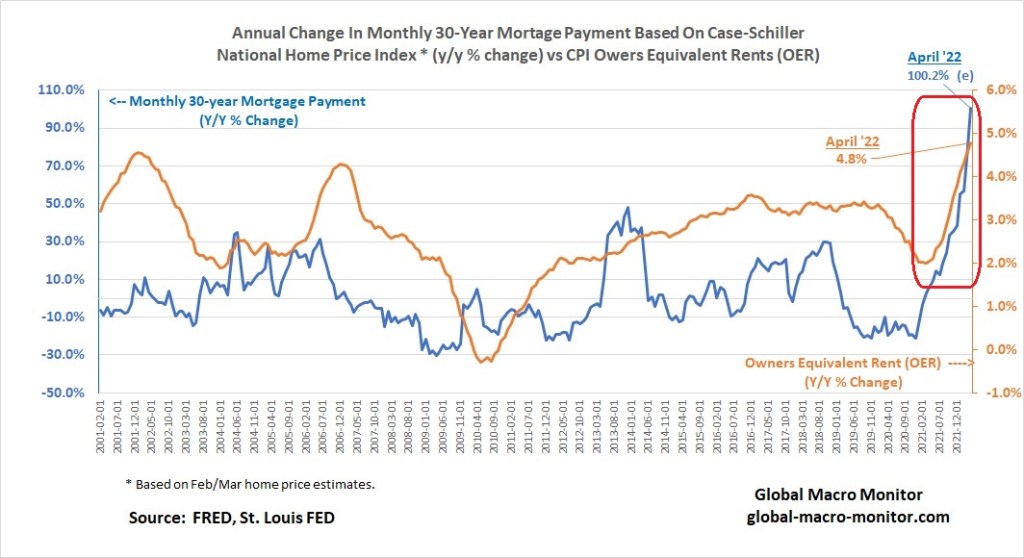

Moreover, the 30-year fixed-rate mortgage rate was up 150 bps, or 47.3 percent, driving up the cost of the monthly mortgage payment on the average house price in the United States by almost 75 percent. Let’s repeat that, folks, our best approximation of the cost of a monthly 30-year fixed-rate mortgage payment is up 75-100 percent in the past year.

The official measure for owners’ residential home inflation in the CPI basket is up a relatively measly 4.5 percent year-on-year as measured by Owners Equivalent Rent (OER), 24 percent of the CPI basket. What a complete joke.

Watch this space in tomorrow’s CPI release. [OER came in today up 4.8 percent y/y, which kept the overall number hotter than expected.]

The spike in mortgage payments has priced out most first-time buyers, forcing them into the rental market (7.4 percent of the CPI), raising rents by over 4 percent in the past year.

Different Housing Market Than The GFC

Of course, the housing market is in a much different condition than it was at the onslaught of the Great Financial Crisis (GFC), as all cash payments — an acute reflection of too much “money” in the system — have replaced the funky, highly levered subprime mortgages.

The result should be the reverse of the GFC, where housing prices collapsed almost overnight. This time, we expect a slow and chronic leak in housing prices with fewer forced bankruptcies, and less sensitivity to mortgage rates as they continue to climb until the Fed gets rolling in draining the excess money from the economy.

OER Starting To Track Real Housing Costs

Let us beat this dead horse one more time.

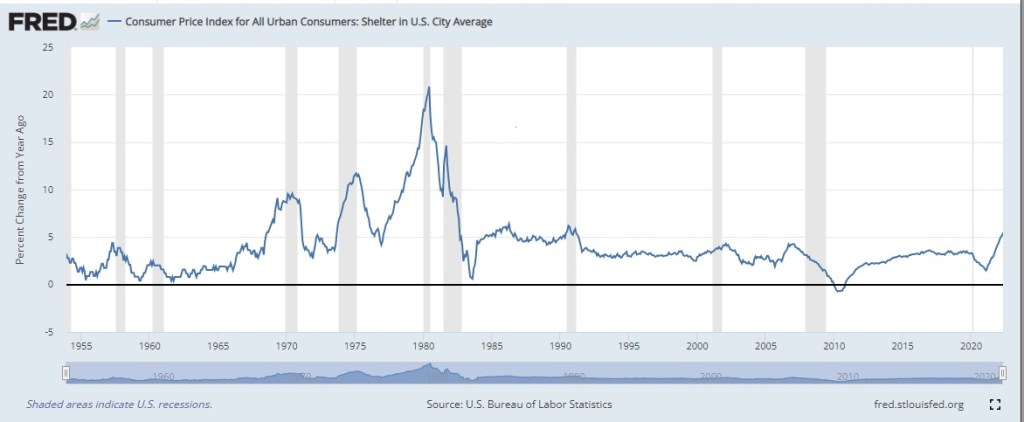

The above chart also illustrates that OER is starting to track the monthly mortgage payment for the first time, which is not a positive for the Fed or inflation.

The reason for this apparent disconnect is that most homeowners and renters did not move in 2021. They thus did not have to pay the spot price for shelter as it rose rapidly. Instead, many had to pay the rate that they signed for earlier in the year or the rate they signed for years earlier that had been modified slightly by their landlord or bank. These prices should tend to converge to the market price, but the lag time may be significant and the convergence incomplete. – VOX.eu

If homeowners have changed their perfunctory answer to the BLS survey question used to calculate 24 percent of the CPI

“If someone were to rent your home today, how much do you think it would rent for monthly, unfurnished and without utilities?” – BLS

to one where homeowners perceive themselves as real renters that track real mortgage costs, or if they get the Airbnb bug, the measured inflation rate for shelter will continue to rise. This may or may not be happening but keep it on the radar.

If it does, expect the Washington bureaucrats to start tinkering with the cost of shelter in the CPI as they did in 1983. See our post, Today’s Inflation Rate And Nolan Ryan’s Fastball.

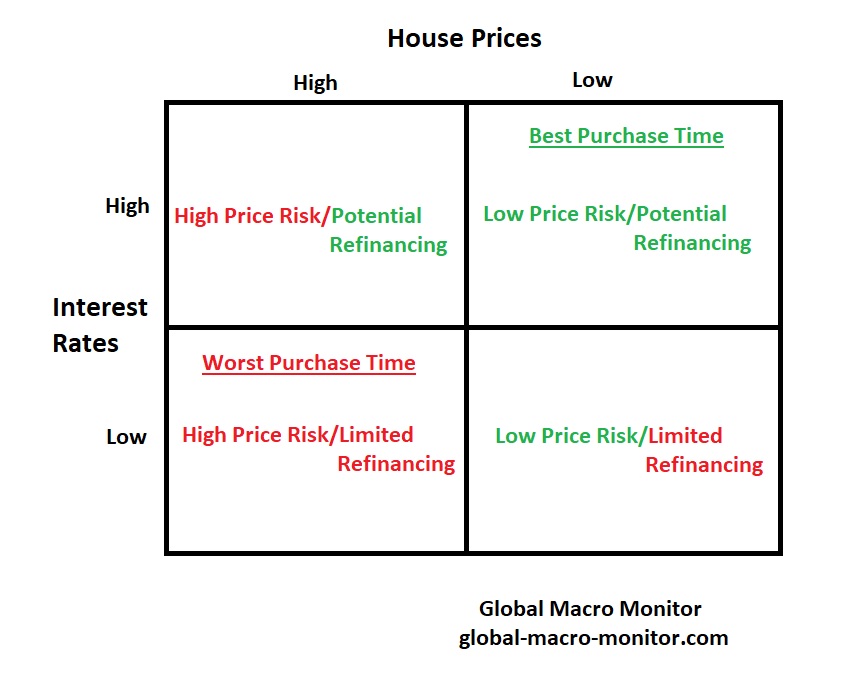

Best & Worst Time To Purchase A House

We feel for first-time homebuyers caught up in the FOMO bubble of the past year. We concede they may have some inside knowledge of a potential spooky inflation to come, but stretching to buy a starter home on a limited budget when interest rates are at artificial and historic lows, and prices at record highs can, and most likely, will be a toxic cocktail. Of course, we are not talking about the properties or “LifeStyles Of The Rich And Famous.”

Just In Case You Think The Fed Has A Clue

Originally Posted on April 29, 2021 by macromon

This should dispel the notion.

Can’t wait to hear the Chairman justify zero rate policy and deficit monetization with inflation roaring at > 5 percent. It would be entertaining if it weren’t so damaging.

Where To Inflation?

Here’s a pretty good theoretical model (follow the entire thread) estimating that U.S. inflation may reach double digits by Q1 2022. One of the premises is that monetary authorities have no way out of this rabbit hole and are constrained by the risk of severely disrupting financial markets in an asset dependent economy.

Recall our view that deflation/inflation is a corner solution and Wall Street’s “Goldilocks” scenario is still just a marketing gimmick. Deflation as markets try to move back to mean valuations – a lot lower – or inflation, and lots of it.

h/t CG

Anyone with a better model, lay it on the table. Stop with the “fake news” or “don’t worry” nonsense. CPI prints > 4 percent in May and you heard it here first.

GMM’s Health Wars

CK and I are battling some serious health issues. Mine, an acute skirmish, which I am now recovering.

CK’s, a three-front protracted war. Her courage to get up and fight everyday has been such an inspiration during my little battle. She also saved my life by forcing me to “ignore my primary doctor’s diagnosis of “all is well” and aggressively pursue my symptoms.” If not for that, the Grim Reaper would have liquidated my position and GMM would be no more. Thanks, CK.

Pingback: “Gimme Shelter” Stones Today’s CPI Report | Global Macro Monitor