#CKStong

Imagining A Treasury Market Without Central Banks

In their discussion, all [FOMC] participants agreed that elevated inflation and tight labor market conditions warranted commencement of balance sheet runoff at a coming meeting, with a faster pace of decline in securities holdings than over the 2017–19 period. – FOMC, March ’22 Minutes

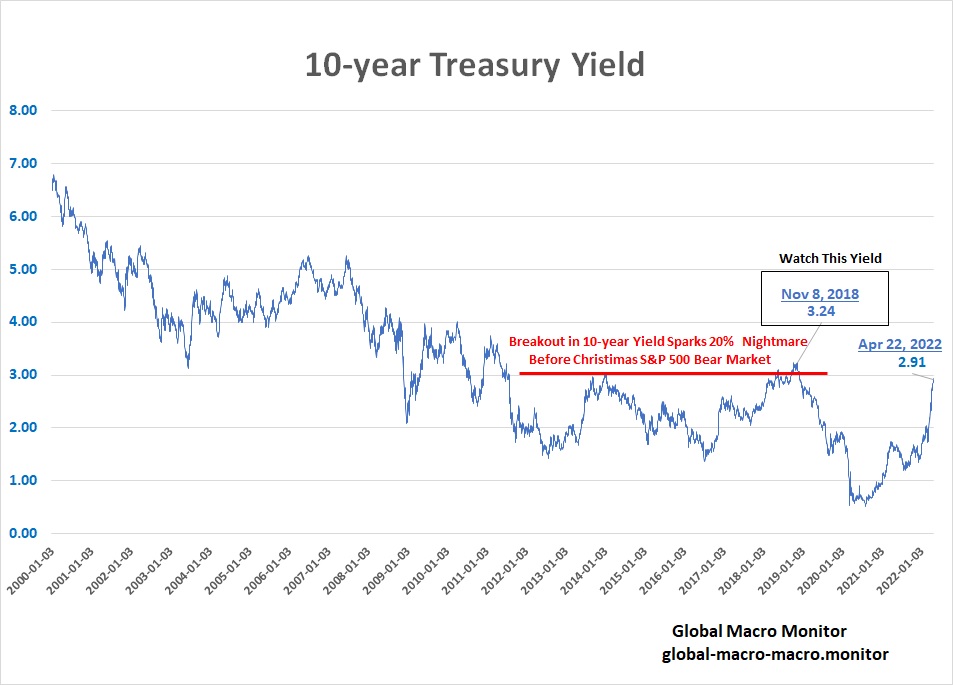

- The 10-year bond yield certainly is:

The 10-year yield is up 172 bps (144 percent) since our July 2021 post, Ignore The Bond Market Flapdoodle. Bond yields had collapsed almost 40 bps in less than a month, bringing out the “doom and gloom” crowd preaching “the bond market is signaling something bad is about to happen in the economy.” Like, inflation?

To which we countered,

Longer-term Treasury yields are so distorted by central bank buying they are now and have been for years worthless in providing any sound economic signal. – GMM, July 2021

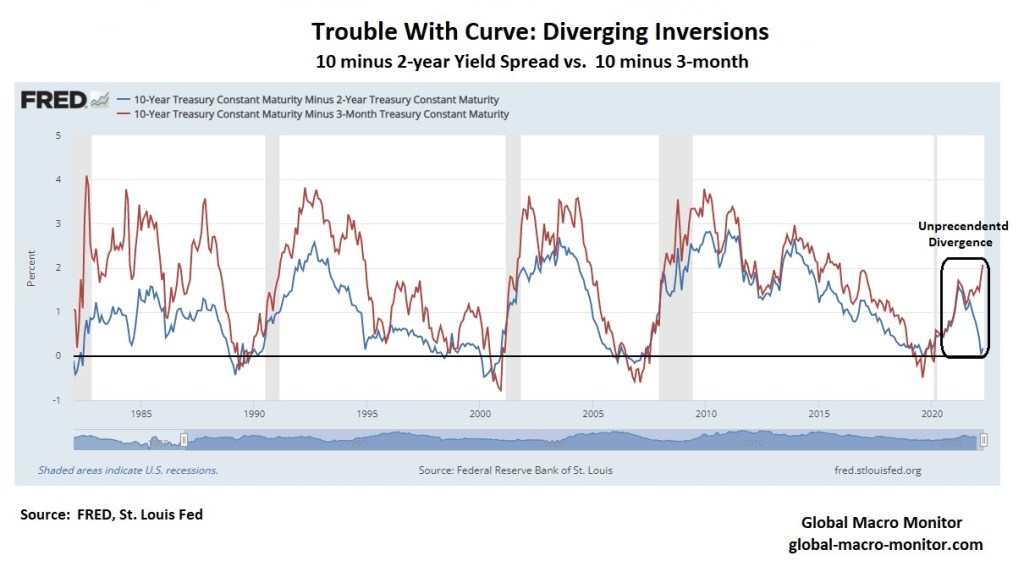

The 10-year is up 37 bps since the April 6th FOMC release of their minutes detailing a more aggressive balance sheet reduction. Before the announcement, the doom and gloomers were out with their “recession is imminent” call as the 10 minus 2-years spread inverted (went negative). Someday there will be a recession, but we doubt we will divine it from a severely distorted yield curve. Until then the bond market will be busy pricing in a new inflation and monetary regime.

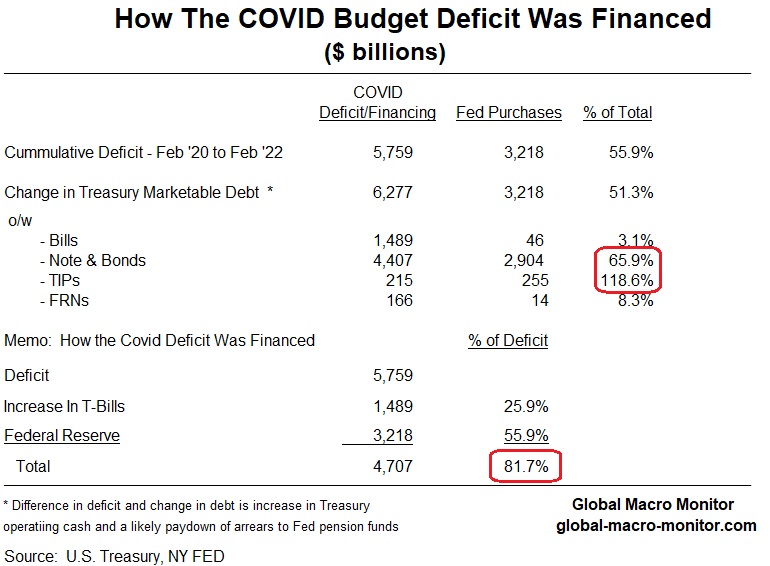

- Eighty-two percent of the COVID deficit was financed by the Fed and an increase in T-Bills. The Fed purchased, albeit indirectly, 66 percent of the notes and bonds and 119 percent of the TIPs issued during COVID. Though extraordinary circumstances often call for extraordinary monetary policy, the massive intervention to finance the COVID deficit, which the Fed and global central banks overshot – by no fault of their own — but overstayed their welcome and is THE primary reason inflation has spiked. Market interest rates? Laughable. Deficit without tears, then came nontransitory inflation.

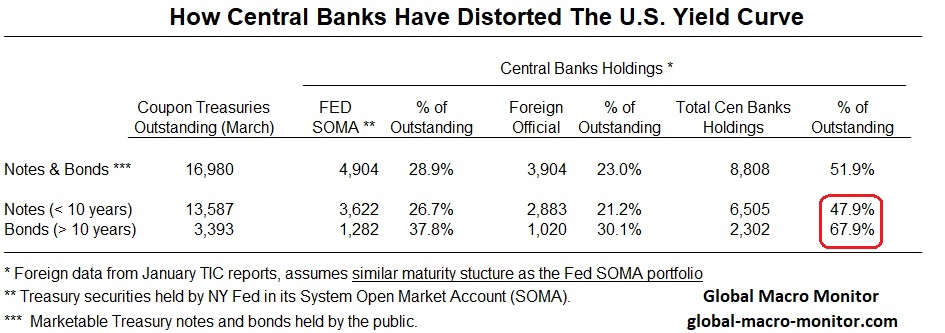

- Central banks have been the major buyers of Treasury coupon securities. The Fed and foreign central banks hold almost 70 percent of outstanding marketable Treasuries longer than ten years, ergo an engineered shortage of risk-free duration.

Our analysis assumes that the maturity structure of foreign central banks’ U.S. Treasury portfolios match the Fed’s – about 74 percent in securities less than ten years and 26 percent longer than ten years. It may be off slightly, but it’s the best approximation we can find.

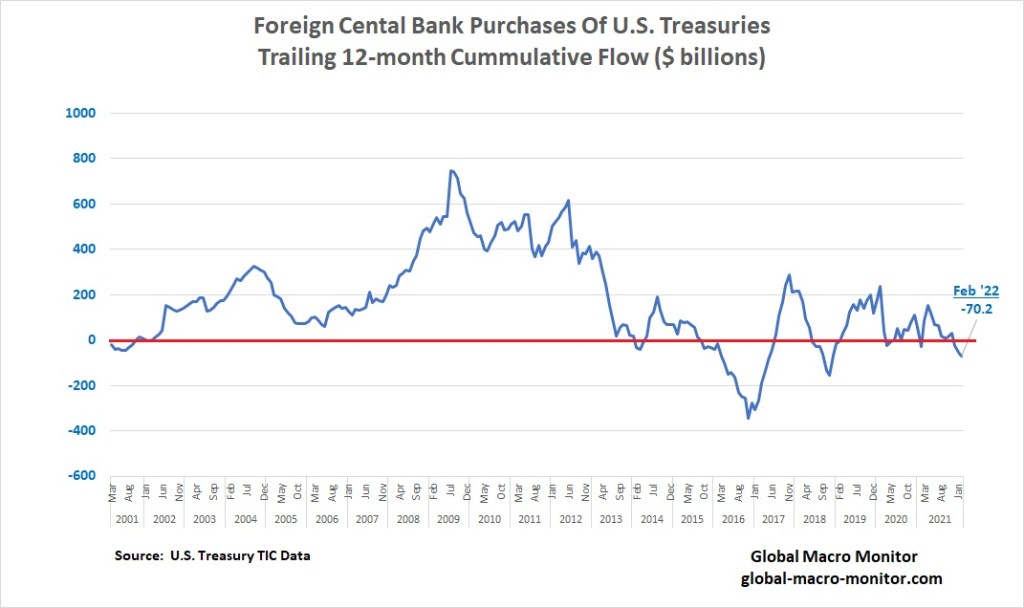

- Foreign Central banks, which are not price or market-sensitive with their securities holdings, are now net sellers of Treasuries. During the last decade, central banks held almost 75 percent of total foreign holdings of Treasury securities as they recycled their current account surpluses back into the Treasury market to protect their exchange rates from strengthening and becoming overvalued. Today, the central banks hold a little more than 50 percent of foreign holdings of Treasuries.

- Will China Dump Their $1 trillion in Treasuries after the sanctioning of the Russian Central Bank? February is the latest TIC data, so we don’t know yet but suspect they will. It would be foolish for them to keep $1 trillion of their $3 trillion in reserves in Treasuries in a country they perceive as an increasingly hostile power.

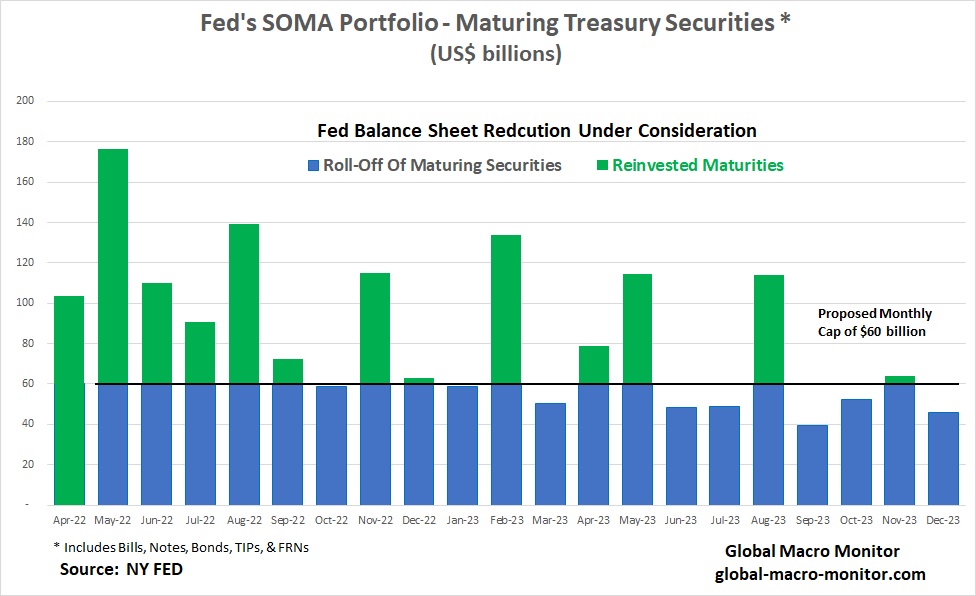

- The FED is about to become net sellers of Treasuries in aggregate — unlikely in individual securities, however – in May or June of a maximum of $60 billion per month. The monthly cap of a $60 billion roll-off its Treasury portfolio is not set in stone quite yet.

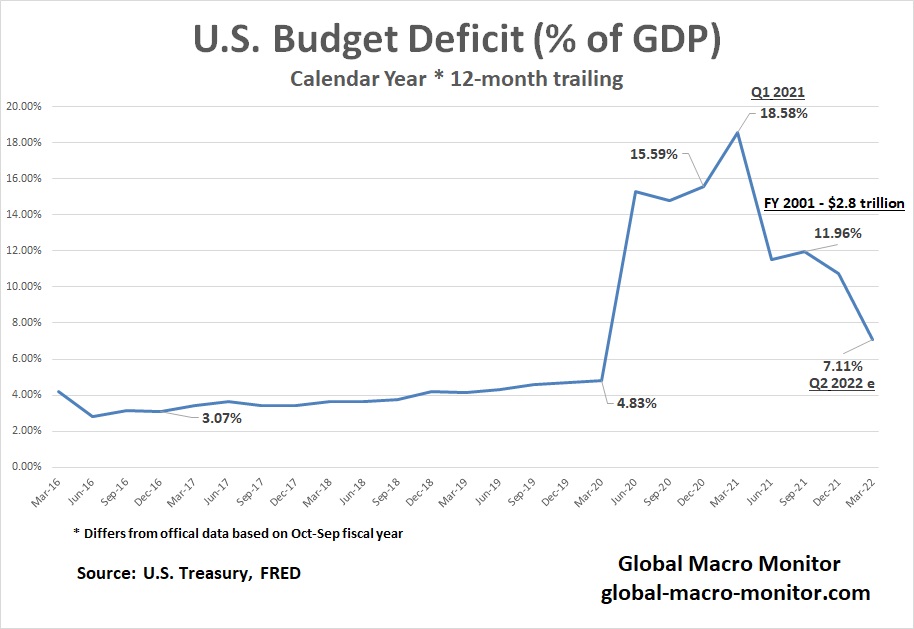

- U.S budget deficit is declining rapidly from the astronomical COVID highs but remains significantly elevated on a historical basis. This should relieve some pressure off yields but is unlikely to offset the exit of central bank buyers.

- The recent 10 minus 2 year yield spread inversion (negative) was not validated or confirmed by the 10 minus 3-month spread. Unprecedented. Yield curve weirdness happens.

This peculiar behavior in the yield curve leads us to believe that the the entire yield curve is about to shift much higher.

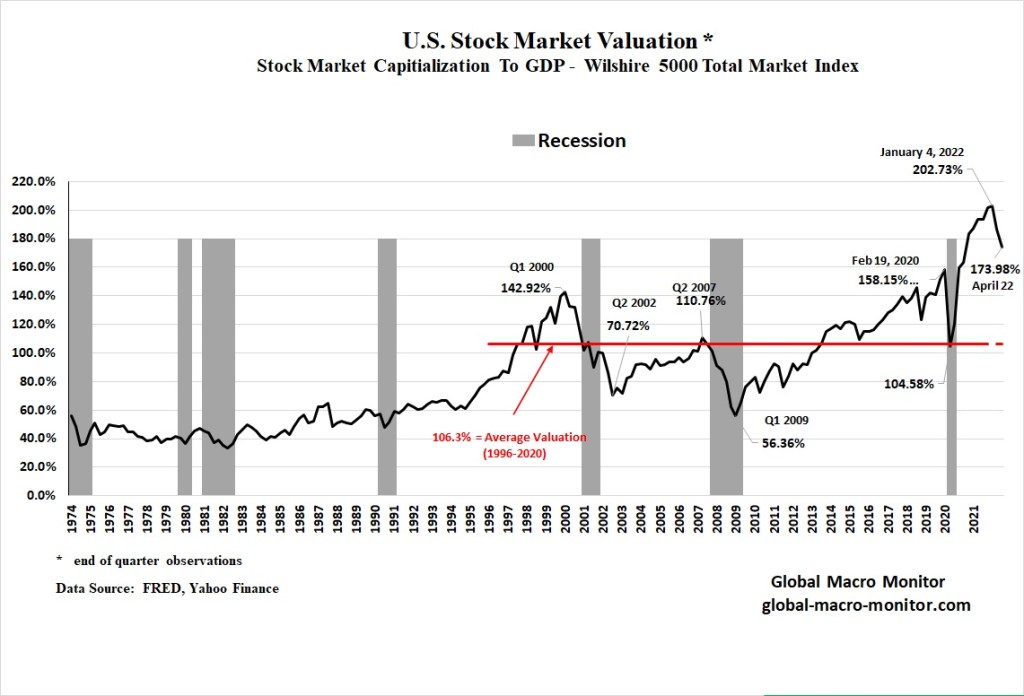

- Stock valuations as a whole have come in a bit due to price reductions and inflation but remain at extreme valuation levels. The rise in Treasury yields is doing a number on valuations, particularly growth stocks, as equity premiums rise with interest rates.

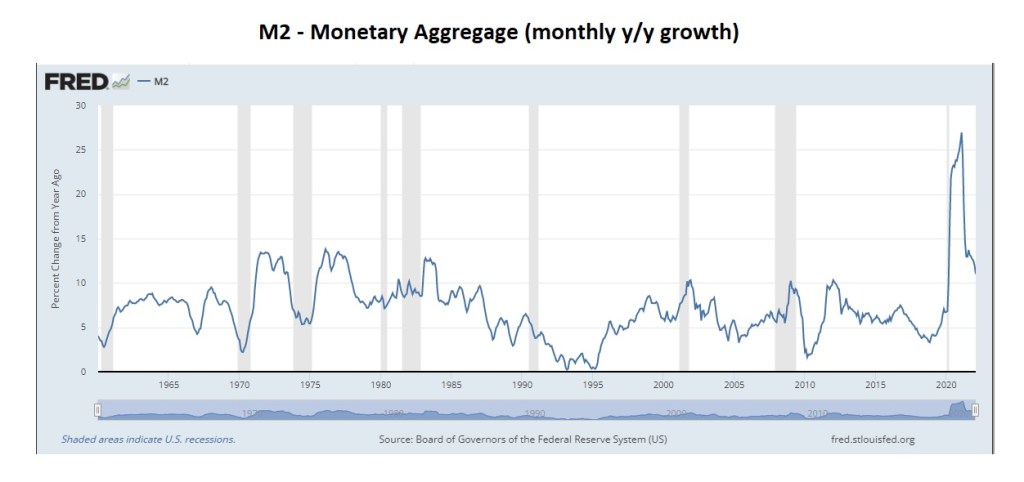

Why we are experiencing high inflation? I spent half my career asking finance ministers and central bankers, especially in high inflation emerging market countries, “What will be your budget deficit this year and how do you plan to finance it.” Large deficits financed by digital money printing without a corresponding increase in production almost always leads to inflation.

Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output. – Milton Friedman

Yes, supply shocks matter but much of the supply shocks result from too much demand. Supply shocks generally result in relative price shifts and not a general rise in the price level.

Money is an elusive concept and difficult to define, even more so as technology progresses. Still, many dismissed the link between the monetary aggregates and inflation as nominal GDP began to diverge from the official money figures in the mid-1980s.

We define money as base money, deposits, cash, credit, global wealth, crypto, and among other things, which allow economic agents to purchase goods, services, and assets. M2 — demand deposits, cash, and near money — doesn’t do service to the concept of money but is one of the best official approximations we have.

What about my securities margin account that I can write checks on?

- Upshot

Yields are set to move higher in search of their actual market value as the nonmarket buyers have exited stage left and become net sellers.

We could be wrong if asset markets collapse (doubtful in the short-term given the vast amounts of money in the system) or another economic shock hits the global economy, bringing the duration jockeys, safe haven buyers, and hedge funds, who use the long Treasury market as a safer proxy to stock shorts, back into the Treasury market.

Beware of recency and complexity bias, folks. Globalization, which is about to accelerate and we rid ourselves of denial, and the inflationary forces are real and hazardous to the global economy and valuations. We are in a new era.

Stay tuned.

Pingback: CPI Inflation’s Big Problem: Housing | Global Macro Monitor

Pingback: Gimme Shelter…Inflation Receding? | Global Macro Monitor

Pingback: “Gimme Shelter” Stones Today’s CPI Report | Global Macro Monitor

Pingback: Bond Market Fundamentals: Rising Risks | Global Macro Monitor