CK is still in the fight of her life. Again, we ask that everybody, everywhere please bring all and whatever you got in the form of prayers, thoughts, positive energy, manifestations, visualizations, anything and everything with powerful intensity her way.

We have been working on this post for some time and want to get it out before the data are too stale. We will break it up into three or four pieces because our analysis of the Treasury market usually results in exceptionally long reads. One reader wrote about our last big research piece on the T market:

This post is so big you can see it from outer space!

We also do not want to bury the lead.

Longer-term Treasury yields are so distorted by central bank buying they are now and have been for years worthless in providing any sound economic signal.

Nothing new here, but we provide you with some good fresh data.

An Ugly Feedback Loop

We have speculated in many posts over the years about the “what if.” That is, what if the Treasury market began to rally purely on technical reasons, yields fall dramatically, and other markets take their cue and act accordingly. You know, kind of like the past week, when equities sold off big on Monday.

The fake yields give a false signal that something nasty is coming; other markets close ranks, and “the bond market distortion yield” kicks the economy into a deep global recession.

Another scenario: What if policymakers base their decision on the distorted yields or “break evens?” The data below show the Fed has bought up the equivalent of almost 200 percent all new TIP issuance during the pandemic.

COVID Budget Deficit

Let’s first answer how bond yields can be so low if the government just ran up such a massive debt from the COVID crisis?

Those are humungo deficits — albeit mostly “transitory” — even by 1980’s Latin America standards, and they do not include large interest payment expenditures, as many of those countries experienced during their high inflation days.

To evaluate the government’s fiscal situation, analysts typically reference the total deficit — the gap between total federal spending and revenues. However, another measurement — the primary deficit — focuses on the difference between government revenues and spending, excluding interest payments. By excluding debt service, the primary deficit highlights the underlying structural imbalance between the amount of money that the federal government brings in each year (mostly through taxes) and how much it costs to provide government goods and services. – Peterson Foundation

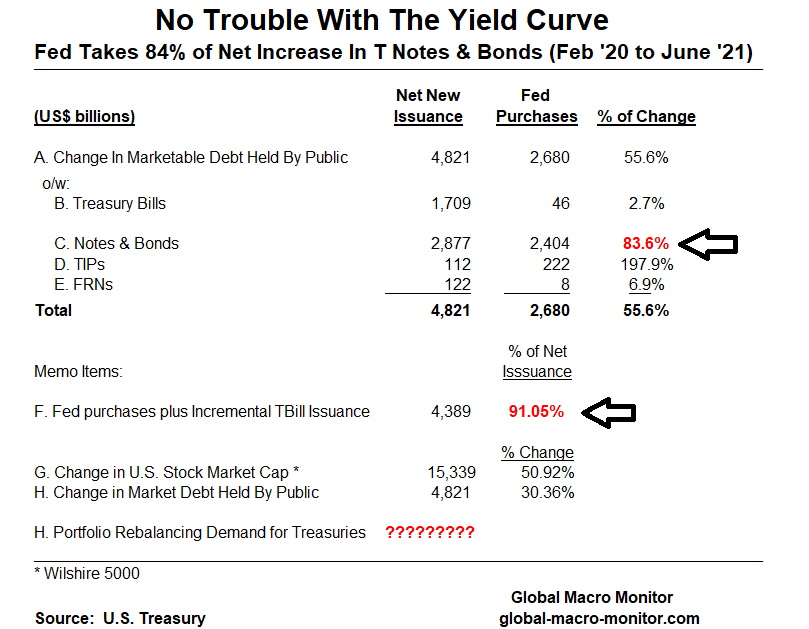

Change In Marketable Debt Held By The Public

So how could the government float another $4.8 trillion of debt in the market without significantly spiking interest rates? Is the bid for U.S. government debt that strong?

No.

In fact, one of our most prophetable (yes, spelling is correct) posts came in early March 2020, warning there was no way the government could finance what we expected to be huge deficits to support the economy during COVID.

Can the U.S. government finance its $1.2 trillion plus annual deficits with an entire yield curve at less than 1 percent?

We seriously doubt it and the Fed is going to have to step-up big time with QE, non-QE, or let’s just call it for what it is, monetization. – GMM, March 8, 2020

One week after our post, the Fed announced their massive Treasury purchase program and later effectively nationalized almost all U.S. bond markets.

COVID Debt Issuance

Take a look and stare a bit at the following table.

That data show the U.S. G increased its stock of marketable debt held by the public by $4.8 trillion from the end of February 2020 through June 2021. Treasury Bill issuance increased by $1.7 trillion, something that many analysts miss when they make statements, such as

“the Fed has financed 50 percent of the COVID deficit.”

True statement but dig deeper.

Fed Purchases

The Fed purchased a total of $2.7 trillion of Treasury securities during the period, of which 90 percent went to the purchase of Treasury notes and bonds. Thus, the Fed COVID purchases amounted to almost 84 percent of all new note and bond issuance by the U.S. government, putting relatively little pressure on the yield curve.

Add the $1.7 trillion of net new issuance of T Bills, with the stock increasing from $2.6 trillion (15.2 percent of marketable debt) in February 2020 to $4.3 (19.7 percent) and that takes care of over 90 percent of the deficit. Easy money, no pressure on the yield curve.

Also note the Fed’s purchase of almost 200 percent of the TIP issuance during the period, which, no doubt was to manage the “breakeven rates.” The U.S. central bank now owns 22 percent of the TIPs market.

Once down the monetization rabbit hole, more dikes have to be plugged.

Rebalancing

The $473 billion difference between the new issuance of notes and bonds and Fed purchases during the period could have easily been absorbed and then some by just the rebalancing effect alone. The U.S. stock capitalization increased $15 trillion during the period bloating the equity allocation in many portfolios and forcing a reallocation to fixed-income, some of which to the Treasury market. No price sensitivity, auto pilot buying. No signal, bad noise.

Upshot

Now you can LOL, well, at least smile, next time you hear,

What is the bond market telling us?

We will concede that though yield levels are meaningless and should be much higher, direction may, at times, provide some some useful information.

Coming up in the next chapters of this post, we will look at the changing ownership of the Treasury market, the timing of how Treasury financed its COVID deficit, how foreign central banks are reducing their allocation to Treasuries, and how central banks — the Fed and foreign — own almost 60-70 percent of all Treasury notes and bonds with a maturity longer than seven years. Stunning.

Stay tuned.

#CKStrong

Pingback: This Week’s Best Value Investing News, Research, Podcasts 7/23/2021 | The Acquirer's Multiple®

Pingback: What Are Bond Yields & Breakevens Telling Us? | Global Macro Monitor

Pingback: The Off The Charts Bull Market | Global Macro Monitor

Treasury market is not the point

The point is the Dollar

Strength here shows as bad the US is, the row (EU, Japan) is worse

The point is also Yuan

Despite all the emerging issues in China, refuses to correct (forget a breakdown)

Pingback: Globa Macro ChartFest: Synopsis Sunday | Global Macro Monitor

Pingback: The Great Reset: The Bond Yield-Dollar Feedback Loop | Global Macro Monitor