Carol K.’s ANC broke above 1200 today. Absolute Neutrophil Count (ANC ) measures a type of white blood cell that kill and digest bacteria and fungi to help the body fight infections and heal wounds. At a time around Day 0 of her stem cell transplant, it was below 100, which is severe neutropenia and often fatal for cancer patients. Her fight and grit coupled with the combination of the miracle of modern medicine, deep resources, and all of your support — prayers, positive thoughts and energy, and other — around the world produced this miracle. Thank you so much to all of you. She will be discharged after a 5 1/2 month hospital stay in isolation in early Novie. Halle-freaking-lujah!

A very close friend posed the question in this post’s title to me the other day.

I laughed and said, “are you kidding me? I mostly ignore the bond market flapdoodle as it was nationalized long ago. Bond yields and breakevens are about as relevant as the price of sausage, Back In The USSR! Ergo, the bond market is not a real market with real price discovery.

Baby, It’s Foggy Outside

Unfortunately, policymakers continue to make policy based on totally distorted flight instruments, which is very dangerous when it gets foggy. The economy is foggy today, folks.

It looks like PK is starting to waffle, and seems, to us, he may be considering playing out his option on Team Transitory,

Why is it so hard to make a call on inflation right now? Because the current economy, still very much shaped by the pandemic, is, to use the technical term, weird. In particular, the standard measures economists use to distinguish between temporary price blips and underlying inflation are telling different stories. – Paul Krugman, NY Times

Krugman’s piece is a must read.

Fed Intervention In The “COVID” Bond Market

Maybe if we had a free bond market, we would have seen this inflation spike coming through a real and true bond yield and breakeven price.

The conventional wisdom is that the Fed has financed 40-50 percent of the debt the U.S. Treasury has put on its books during COVID, and that is confirmed by the data at 46.6 percent of all new issuance, including Treasury Bills. We dig deeper in the following table.

Look at the profile of the new debt that financed the COVID deficit, however.

The Fed has effectively purchased 75 percent of all new note and bond issuance and 160 percent TIPs issuance from March 2020 to September 2021. If they hadn’t, interest rates would have spiked higher, maybe 500 bps higher, and it is possible some of the auctions would have failed.

Why doesn’t the Treasury fund itself with more longer-term debt to lock in the lower rates? Because they can’t, which illustrates why T-Bill issuance was up $2.5 trillion during COVID.

Moreover, if you are going to repress coupon yields from moving to their equilibrium, you must also do the same in the TIPs market, otherwise breakevens would have gone wild and made no sense, especially given its a relatively illiquid market.

If there was real price discovery in the bond market, it may have tipped us off about a coming inflation spike and what markets really think about the path of future inflation. After all the supply chain lbroke last year, so there was plenty of time for the bond market to get it right. See our post, Hot Retail Sales Not Supply Chain Positive.

Financing Of The Monthly Budget Deficits

The following chart illustrates the path of the U.S. monthly budget deficits (red line) during COVID and how they were financed.

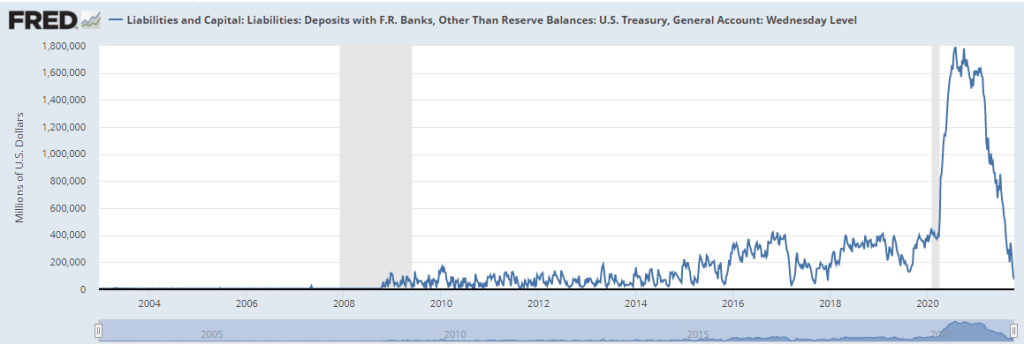

Treasury finances itself either through: a) borrowing from the public (black line), b) reduction in operating cash. mainly in its General Account at the Federal Reserve (blue line), which is down from $1.8 trillion in July 2020 to a measly $78 billion on October 13 (see here), and confirms Secretary Yellin’s assertion the government is almost out of cash, and through c) other means, such as running arrears on Treasury contributions to federal government employee pension funds, to suppliers, and other extraordinary ways.

We suspect “defaulting on the debt” as an “other means” form of financing is a bluff as the government will look for other bills and/or entitlements to run up arrears on to conserve cash and prioritize spending.

Tapping The Market When It Can

The chart also shows that Treasury seems to be very good at tapping the market when there is a flight to quality bid. Note how almost 70 percent of all COVID borrowing from the public took place during March 2020 to June 2020, and exceeded the cumulative deficit during that period by 50 percent. The positive difference went to build their reserves in the Treasury’s General Account.

Even still, the Fed bought, albeit indirectly, the equivalent of about 55 percent of all new borrowing during March 2020 to June 2020.

Debt Ceiling Politics

Nevertheless, the political cost to the Administration of using other means as a source of financing, say, suspending Social Security payments, if legal, is certain political death, and that, folks, is the game that is playing out in Washington today.

Forget about advancing the national interest, just destroy the opposition, and to be fair, it always seems M&M is on the wrong side of this issue.

(the sum of the three non red lines in the chart above will always equal the red deficit line)

It is interesting that the Treasury’s borrowing from the public (black line) is constrained by the debt ceiling and has been negative over the past few months, all while the Fed is taking $80 billion per month in Treasury securities out of the market. No wonder why bond yields dipped during the summer, which some took as “everything is perfect,” deflation is coming, and, though we hope not, the policymakers took “as inflation is under control.”

It is almost laughable to hear comments, such as,

Is inflation caused by [monetary] inflation or by the supply chain problems?

These are coming from major market pundits, who appear, and we could be wrong, they don’t even understand the basic concepts of inflation, much less where it comes from and how to stamp it out.

My experience working with the high to hyperinflation central banks back in the day was there were lots of shortages throughout the economy. No bread on the shelf at grocery stores because of hoarding and a breakdown in…wait for it…local supply chains.

We seriously doubt we get there and will be speaking “Argentine” anytime soon if the FOMC does its job. They tell us they have the tools but do they have the stomach given such lofty and stretched asset valuations? Starting to smell a bit of panic the Fed is way offsides and needs to move quicker.

Stay tuned, folks.

As always, we reserve the right to be wrong in our conclusion as we are pretty certain we have the facts (data) right. We like to tell this story about getting our conclusion wrong.

Facts Right, Conclusion Wrong

President Lincoln, a great storyteller, had something to say about drawing different conclusions from the same established or, what economists like to call “stylized facts,”

During his days as an Illinois circuit court lawyer, legend has it Lincoln would persuade juries with the use of his funny but truth piercing stories,

The story goes that Lawyer Lincoln was worried he had not convinced the jury during the closing argument of a civil case against a railroad. The jurors had gone to lunch to deliberate. Lincoln followed them and interrupted their dessert with a story about a farmer’s son gripped by panic,

“Pa, Pa, the hired man and sis are in the hay mow and she’s lifting up her skirt and he’s letting down his pants and they’re afixin’ to pee on the hay.” The farmer responded to his panicked boy, “Son, you got your facts absolutely right, but you’re drawing the wrong conclusion.”

The jury ruled in Lincoln’s favor.

Chart Appendix

Treasury General Account Balance At The Fed, October 13

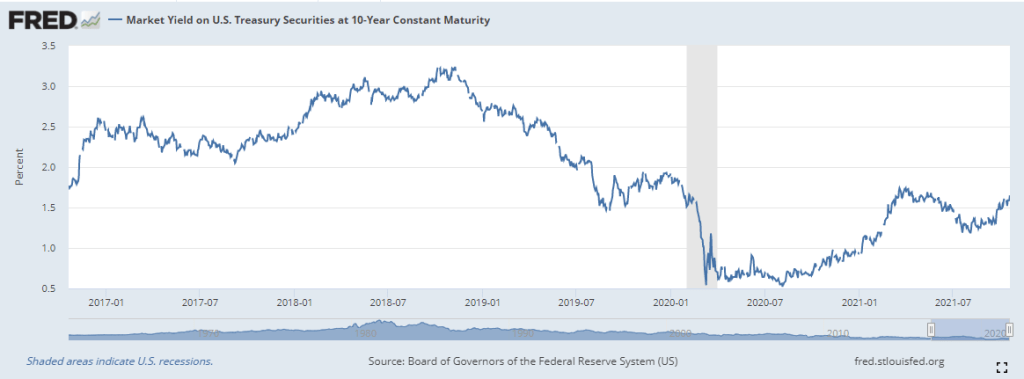

10-Year Treasury Yield

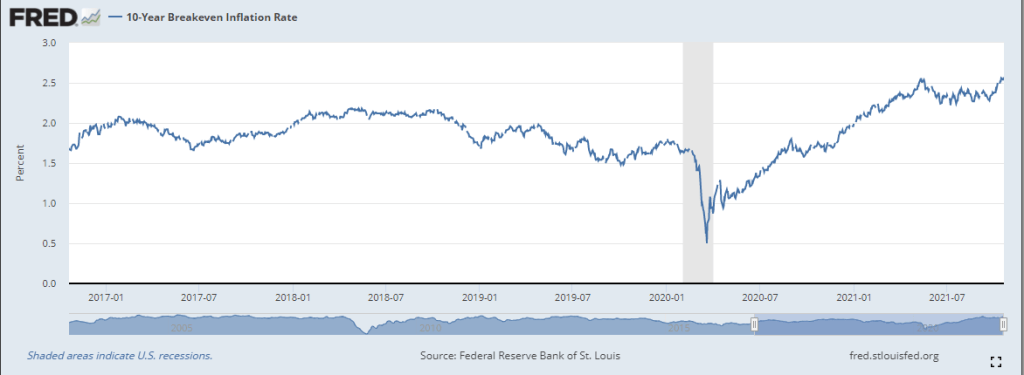

10-Year Breakeven Inflation Rate