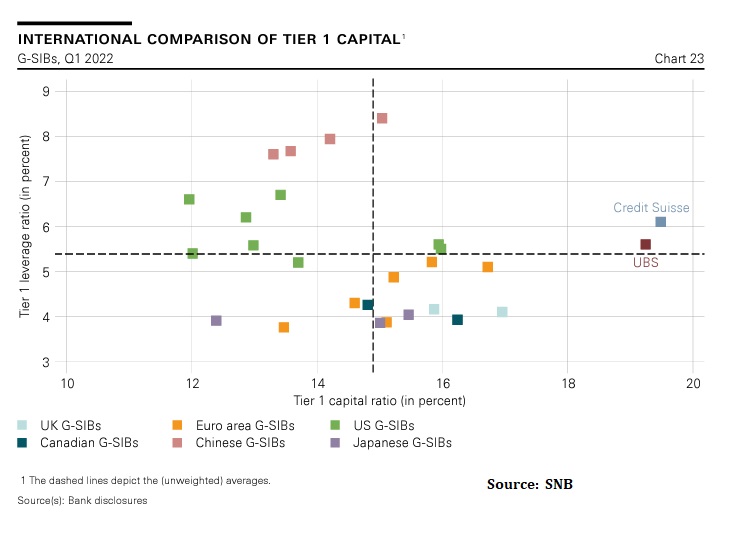

Stare, or should we say, “glare” at the following chart from the 2022 Swiss National Bank (SNB) Financial Stability Report, then you decide. The chart is an update from an earlier post, which included an outdated version.

The SNB also notes,

The Swiss banking sector is distinguished by its size, the dominance of a small number of banks and its international integration. At the end of 2021, total banking sector assets stood at roughly CHF 3,900 billion. This is equivalent to about 520% of Swiss GDP – a high ratio by international comparison (cf. chart 15). A look back over the last 25 years shows that this ratio climbed steadily to over 800% until the beginning of the global financial crisis of 2007/08. Then it fell sharply before rebounding a little recently (cf. chart 16). While both the pre-crisis rise and the post-crisis decline are exclusively attributable to foreign assets – especially those held by the two largest Swiss banks, Credit Suisse and UBS – the recent rebound has been driven by an increase in domestic assets. Against this backdrop, domestic employment in the Swiss banking sector has remained relatively stable. – SNB, Financial Stability Report

The data show that Europe is still ginormously overbanked and needs a further deepening of its capital markets.

Capital Ratios, Smack Those Ratios

Credit Swissie, where art thou? Always question, dig deeper, and be skeptical and contrarian, folks.

Largely Contained

Here’s to hoping, and our priors are, though we have not been following the situation closely, that the deposit instability of the past few weeks and the banking “mess is largely contained.” Wait, that sounds familiar.

Stay frosty, folks.