Excellent video on China’s demographic bomb. An outsized cerebral return on your 15-minute investment. Must view, folks.

Excellent video on China’s demographic bomb. An outsized cerebral return on your 15-minute investment. Must view, folks.

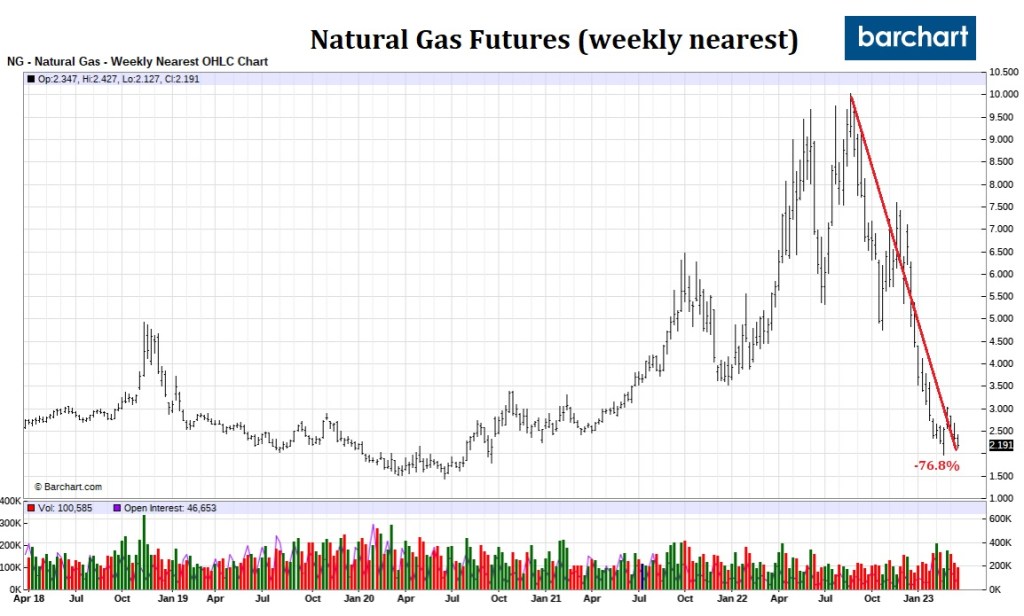

Traders apply the term widow maker to financial investments that cause catastrophic losses or are risky enough to do so…Another famous example of a widow maker trade occurred in natural gas futures, which professional traders have long considered widow makers because of their price volatility. – Investopedia

Jaysus (h/t CG), U.S. natural gas (Nattie) futures are down 76.7 percent from last August’s peak. Moreover, European Nattie prices are down 87 percent from the highs.

Remember the pundits predicting Europe was going the way of Pompei as the Russians cut off their natural gas supplies?

Europe may be about to experience its first winter without Russian gas, risking even higher prices, gas shortages, and a major recession. – IMF

Not so fast. Mother nature had different plans.

Warm weather and a sharp downward shift in demand have contributed to the fall in prices in Europe. At the same time, higher prices also sparked efficiency gains, lower consumption among businesses, and in some cases reduced industrial activity. In the United States, warmer weather also reduced the demand for natural gas. – World Bank

California Reamin’

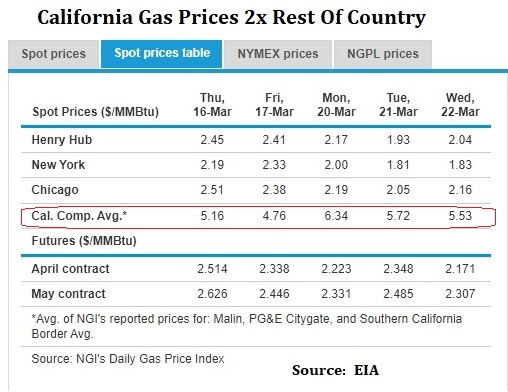

It is said that everything is bigger in Texas. We will match and raise that and tell you everything is [more] expensive in California, including Nattie.

California imports 90 percent of its gas from other states and Canada, so it’s reliant on pipelines. But many of those pipelines were closed for unplanned maintenance in November and December, limiting supply flowing to California and other Western states… A pipeline explosion in 2021 had already reduced capacity to move gas from Texas and neighboring states, where much of California’s supply comes from.

Additionally, the past few months in California have been especially cold, creating an unusually high demand for heating…That came after a historically hot summer strained the state’s electricity grid, which is largely powered by natural gas… NY Times

Thank You, Natttie

We do owe Nattie a big debt of gratitude. The widowmaker, after almost causing us to have a widowmaker, forced our trading book into retirement. We now sleep better at GMM. Thank you, Nattie!

Here is a follow-up on last week’s chart with some excellent granular detail.

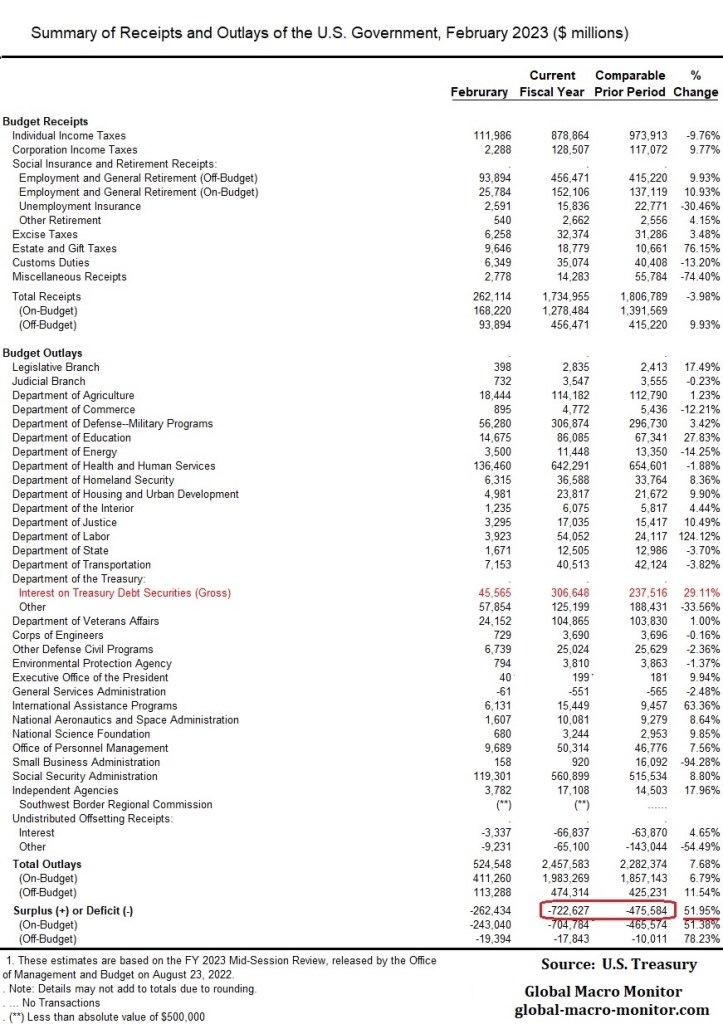

Interest payments on the national debt during the current fiscal year (October to February) are up 29 percent y/y, one of the fastest-growing expenditure components of the Federal budget (see table).

Revenues are down, especially individual income taxes, which may reflect the slowing economy. Theory dictates (ceteris paribus) that government tax revenues should be rising with inflation, however. Hmmm.

The fact income tax receipts are lower but self-employment tax revenues (1099 employees) are higher, coupled with what is happening with the employment data, can we hypothesize that high income earners are leaving the workforce (or getting fired) and starting their own businesses, such as consultants, for example? Or could it be just a timing issue?

The overall deficit is exploding, btw, up 50 percent.

If the current situation normalizes and Treasury securities lose their flight-to-quality bid, interest rates are going to spike faster than one of Elon’s rockets.

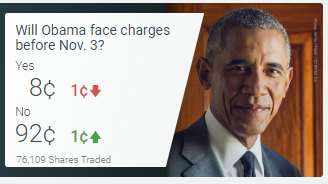

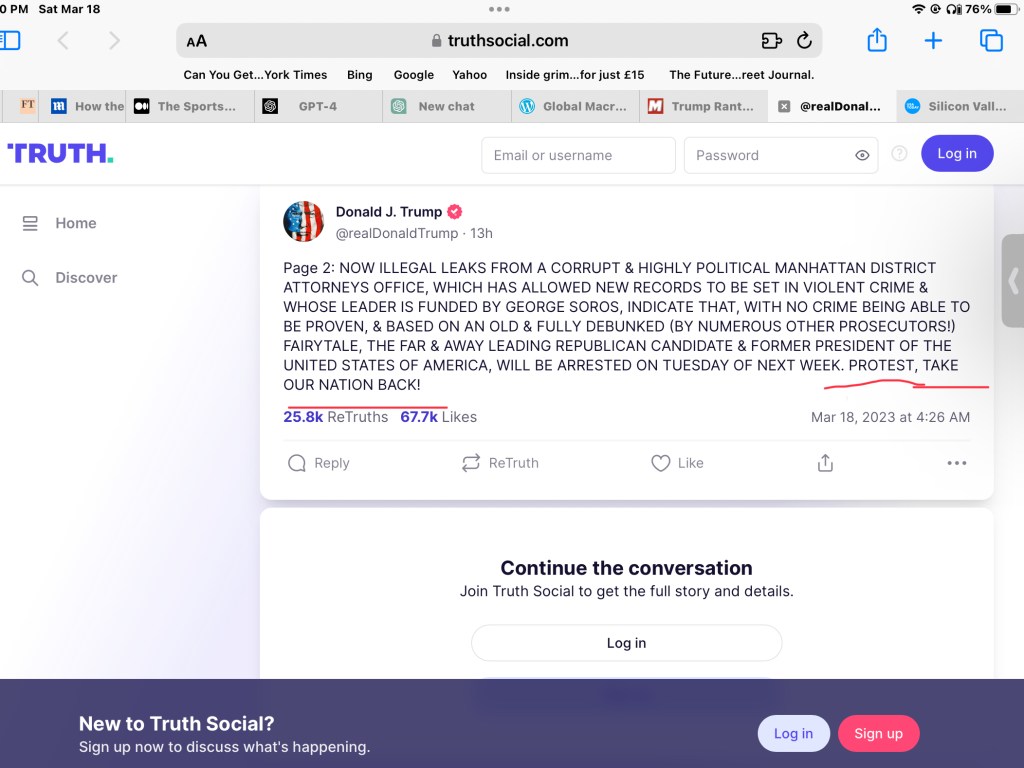

Here’s a repost to keep on your radar, given the expected fireworks on Tuesday. Getting long water canons and the National Guard.

The question is which side does the National Guard side with in the Red States? Will Biden have to federalize the Guard? Arkansas, redux?

On September 23 [1957] President Eisenhower issued Executive Order 10730, which put the Arkansas National Guard under federal authority, and sent 1,000 U.S. Army troops from the 101st Airborne Division to Little Rock, to maintain order as Central High School desegregated. – History Channel

Remember Sarah? Trump’s former press secretary, and now governor of Arkansas. Hmmm….

I used to go home every night as a young Wall Street trader worried about how instability on the “Arab Street” would adversely impact my long unhedged positions. If you have been a reader of the Global Macro Monitor over the past few years, you know we have been concerned about U.S. political stability.

All good traders worth their salt worry 24/7 about just about any and everything, which, by the way, was one of the first traits I would look for in hiring a new trader. A high propensity to worry about losing money but not afraid to pull the trigger.

POTUS Gone Wild

Now we are really getting worried

Rather than being a stabilizing force and a voice of reason and calm, the President of the United States delights in stoking the divisions and tensions in the country while spewing his conspiratorial garbage 24/7.

In the words of Anderson Cooper, “Man, we are in trouble.”

It’s totally outrageous and moves the country closer to a critical tipping point.

November To Remember

Here’s to hoping we can limp to a fair election in November. Let’s not let the Russian GRU and China’s MSS take a victory lap, America.

We owe it to the men and women in uniform making great sacrifices for us and what America has stood for, and, more importantly, to our children and grandchildren.

Fear The Street

It’s time for investors to fear the “American Street” or to, at the very least, keep it on your radar. If that is, markets are still a market and not a tool of the state, which is becoming increasingly debatable.

Stay tuned, folks

Source: PredictIt

Tough week, especially for European banks and equities.

Blast From The Past (BFTP).

For my late grandmother from Cork.

Happy St. Patrick’s (Maweyn Succat) Day!

St. Patrick, Ireland, St. Patrick’s Day. Simple, right? The man wasn’t even Irish! He was actually born in Britain around the turn of the 4th century. At 16 years old, Irish raiders captured him in the midst of an attack on his family’s estate. The raiders then took him to Ireland and held him captive for six years. After escaping, he went back to England for religious training and was sent back to Ireland many years later as a missionary. St. Patrick was actually born Maewyn Succat, according to legend; he changed his name to Patricius, or Patrick, which derives from the Latin term for “father figure,” when he became a priest. – Time

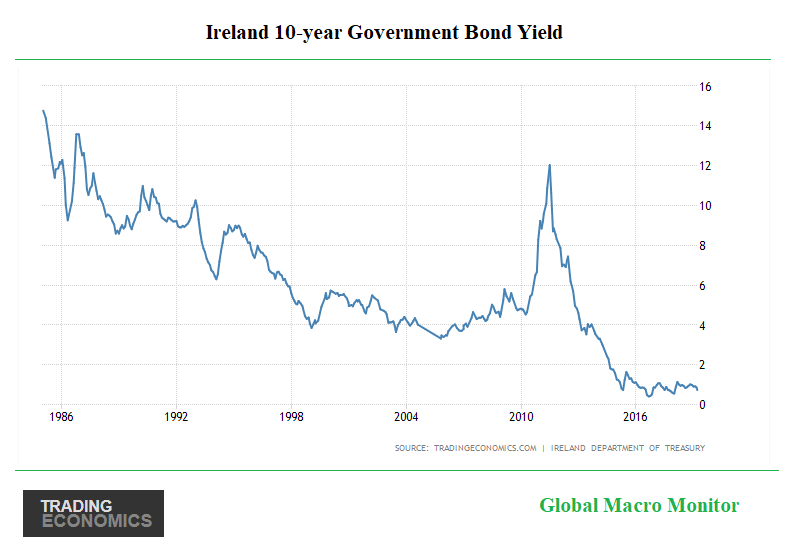

The Irish Comeback

Ireland has come a long way since this post, which was just after the European debt crisis. The government just placed €1.03 billion of 10-year bonds in mid-February at a stunning yield of 0.85 percent. The auction had a bid-to-cover of 2.24.

Yeah, got it, distorted due to ECB asset-buying program. But still well below the Euro periphery bond yields.

Though the Irish economy is slowing and there is much uncertainty around Brexit, still it’s been one helluva comeback, and the Irish are a resilient bunch, now positioning themselves with U.S. and Canadian companies as the “only English-speaking common-law country in the whole of the European Union.”

Me “finks [sic]” part of the success was thumbing their nose and ignoring the advice and dictates of the Eurocrats in Brussels.

Plus, Ireland still has Bono and U2, Andrea and the rest of the Corrs, and the many, if not all the great people of Ireland, we love so much, including my late grandmother and her side of the family. That is the upside of being an American. We are all mutts and can claim to be citizens of many cultures. Don’t think POUTS has got the memo quite yet.

Rory

How great would be to see an Irishman win the PGA’s coveted Players Championship on St. Paddy’s Day? Rory tees it up in today’s final round one back.

Getting long Rory as I write. Pour me one in Dublin and Hollywood, CD in the wee hours tomorrow to celebrate! You heard it here first. Unleash the Leprechauns!

Source: Golf Digest

In case you’re wondering, Maweyn Succat was St. Patrick’s real name and he wasn’t even Irish!. Click here for some great background and history of St. Patrick’s Day.

Go Paddy, Rory, Graeme, and Darren!

Happy St. Patrick’s Day! Not too many green beers, folks!

By the way, there has been one huge bond rally in Ireland over the past year.

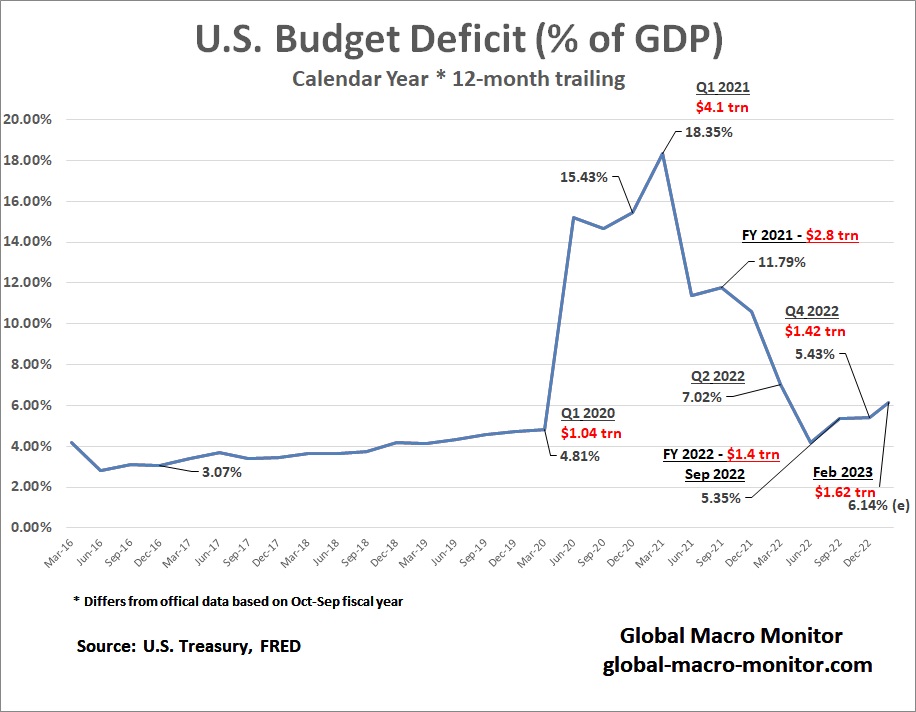

After normalizing post-COVID, the U.S. budget deficit is starting to turn up again. The 12-month trailing deficit was $1.62 trillion at the end of February, or around 6.14 percent of GDP. Good luck bringing inflation down to 2 percent, given those digits and trend. Moreover, financing the gaps during normal times without the Fed and a flight-to-quality bid for Treasury securities will be a challenge for the markets and will put upward pressure on interest rates.

The U.S. Deficit As the 15th Largest World Economy

For context, the current U.S. budget deficit in nominal dollar terms is larger than the economies (gross domestic products) of 178 of the 192 countries in the IMF WEO database. That is, the difference between what the U.S. government spends and takes in is greater in dollar terms than 93 percent of the world’s economies, or about the size of the Australian economy and more than 3x Ireland’s GDP, folks. Stunning.

Prepare to hear all about it as the debt ceiling debate heats up. Tax hikes or spending cuts to reduce the hole is the political question…or just ignore it and wait for the mother of all crises to wash ashore. Most likely, the latter.

After last September’s budget debacle in the U.K. and the resulting market turmoil, which ultimately forced the prime minister’s resignation, we now know deficits do matter.