One of the smartest hedge fund managers we know spends most of his day locked away in his office analyzing how the market consensus could be wrong. He hangs with au contraire crowd, breaking bread with contrarians and demands you check your cheerleader pom-poms at the door when visiting his office. Not that he takes action or trades on all or any of this, but his rigorous discipline of stress testing his perspectives, positions, and the conventional wisdom of the market is a lesson for all of us.

Our hope is the policymakers, especially the Fed, do the same. The world is experiencing the adverse consequences of negative real interest rates and yet the monetary policy prescription of choice is for more negative real interest rates.

In his September 6th FT piece, Bill Gross writes,

…monetary policy at the zero interest rate bound introduces a new dynamic that may conflict or even reverse standard logic that lower interest rates across the sovereign yield curve are everywhere and always stimulative to economic growth.

This potential paradox arises not just from observation of the Japanese experience over nearly two decades, but from an analysis of our modern-day financial system and its potential inadequacies. Fractional reserve banking, where only a portion of bank deposits are backed by hard cash, as well as unreserved collateral-based lending on overnight repo have allowed for an expansion of credit beyond the bounds of a central banker’s imagination.

Mr. Gross concludes the Fed’s pancaking of the yield curve through Operation Twist will destroy the banking system’s incentive to create credit by reducing the opportunity for banks to leverage a positively sloped yield curve

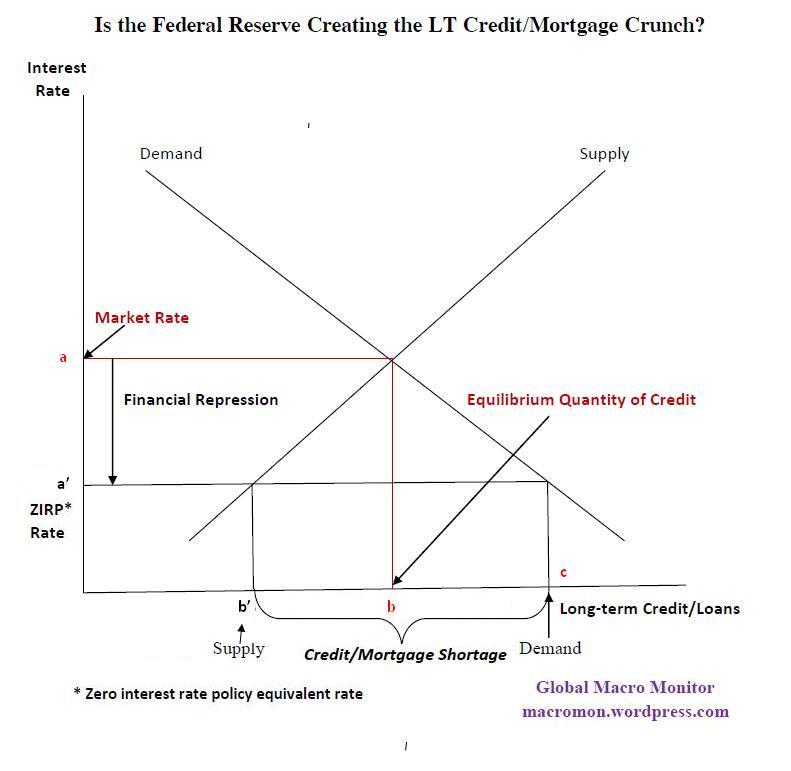

We add our two cents to the Bond King’s skepticism of current policy using the basic supply and demand curves of microeconomics, or what graduate students call “price theory.’ Recall how we were taught as freshman that rent control creates a shortage of rental apartments and housing when government policy distorts or represses market prices.

Take a look at the chart below, which should look familiar as it is simple adaptation of the rent control analysis. The vertical axis shows the interest rate with the horizontal the quantity of loans/credit/mortgages.

It is also important to note demand and supply curves are not observable in the real world. What we see are prices and quantity. But like any economic model, supply and demand curves help us understand the underlying dynamics and the factors that determine the prices and quantity/volume which we observe.

The graph shows that points a and b are the equilibrium market clearing interest rate and quantity of long-term credit/loans/mortgages. The implementation of zero interest rate policy (ZIRP) and Operation Twist represses the rate to point a’. This reduces the supply of credit/loans/mortgages from point b to b’.

After all, who in the private sector will lend long-term money at such repressed and non-economical interest rates? Fannie and Freddie? Yes. Bill Gross and PIMCO? We suspect it’s possible for a trade. Asian investors? NFW!

Furthermore, demand increases to point c at the repressed interest rate forcing either public sector lenders to expand their balance sheets or the market to ration credit through a tightening of credit standards, higher down payments, or by other means. This analysis doesn’t even consider the reduced income on savings and the crowding out effect of the federal deficit. There’s no doubt, in least in our mind, the government is going to get funded first even if the FED has do it alone.

It’s our sense, and we could be wrong, this simple model reflects current reality and one can easily conclude that zero interest rate monetary policy may be what ails the economy and not the prescription that is going to cure it. We throw it out there to help Mr. Bernanke, at least, consider a contrarian perspective, which, like our friend, will make him a better hedge fund manager. Maybe he already has. He’s a smart guy and a professor.

(click here if the graph is not observable)

(click here if the graph is not observable)

{kind=link}

{kind=link}

Pingback: Is the Fed Contributing to the Credit/Mortgage Crunch? | The Big Picture

Pingback: Wednesday links: better forecasting | Abnormal Returns

Pingback: QE and the “Crowding Out” of the Bond Market Vigilante | The Big Picture

welcome to moncler product sales!moncler Down Jackets on hot. sale up to 50% discount.moncler products store online is your best choice.

Pingback: Today’s Links September 30, 2011 | JDreport news and more, Read between the headlines and wake-up.

Pingback: Today’s Links September 30, 2011 | JDreport news and more, Read between the headlines and wake-up.

Pingback: The current housing bust is much worse than the Great Depression | Credit Writedowns

Pingback: Current Housing Bust Much Worse Than Great Depression | The Big Picture

It’s hard to believe that demand for money is as high as it would be per the chart, given the accumulated retained earnings at many companies of any size. I don’t follow rates, but actual rates on closed business loans are not at the Feds rate! Whatever lenders are charging is based on inflation expectations and risk metrics (sometimes).

Certainly the banks are willing and able to borrow near the 0% mark, but they aren’t setting rates that allow that money to flow into the economy. The spread they would need for successful business loans (that properly factor in risk and inflation) would be obscene.

The govt is the only lender that can afford to supply money at that rate.

So the retail credit markets aren’t necessarily screwed up by the disconnect, but bank borrowing and lending is feeding the asset bubble.

Perhaps I shouldn’t try to speak for the author, but what the heck… I don’t think he was trying to show a graph that was accurate and to scale, but rather to show a simple model as to why artificially suppressing interest rates could have the opposite effect that the Fed desires and is trying to promote by forcing the rates down.

Separately, the Fed funds rate etc. may be the rate the Fed will loan to banks and not the rate the banks will loan to *their* customers, but it does tend to lower the retail rates as well. When the money is flowing and the banks are flush with cheap cash, it’s a lot easier for them to loan it out at a lower rate than if they’re having to pay depositors (savers) a higher rate to attract enough savings to loan out.

The banks just need to set a rate with enough profit margin between what they’re paying for the capital and what they’re loaning it out at. If the Fed starts funneling them more money and at lower rates, that’s going to flow out as lower rates to the retail customer eventually.

But the artificially low rates have a tendency to foster inflation, so you’re absolutely right that the banks have to factor in risk of default AND inflation when setting rates and making loans. I think that could be where they get nervous and don’t want to be borrowing short term, even at very low rates and loaning long term without factoring in a premium for inflation taking off. Inflation and rising interest rates is what bankrupted so many Savings and Loans back in the day.

I’ve learnt from the business report in The Wall Street Journal that the recent awful jobs report has sent down the rates. What is your thoughts on this? Could a bad economy be great news for the price of credits?

Jonas, Thanks for the comments. Bad economy is good news for Treasuries as money comes into perceived risk-free rates, which the U.S. government securities is seen as one of the last bastions of zero credit risk. That is, until it isn’t.

I love the power point presentation Roger W. Garrison, professor of economics at Auburn University gives on this topic. He makes the same point, and then some about how the Fed’s intervention by artificially suppressing interest rates has many disastrous effects on an economy. His talk is shown on YouTube here: http://www.youtube.com/watch?v=zhoFOyy7rbo

Unquestionably believe that which you stated. Your favorite reason appeared to be on the internet the simplest thing to be

aware of. I say to you, I definitely get annoyed while people think about

worries that they plainly don’t know about. You managed

to hit the nail upon the top and defined out the whole thing without having side

effect , people could take a signal. Will likely be back to get

more. Thanks