We have ranked the world’s 2016 Current Account Balances (CAB) by country from largest deficit to largest surplus in the ginormous table below. The data are from the October 2016 IMF’s World Economic Outlook database. Note, 2016 are IMF estimates.

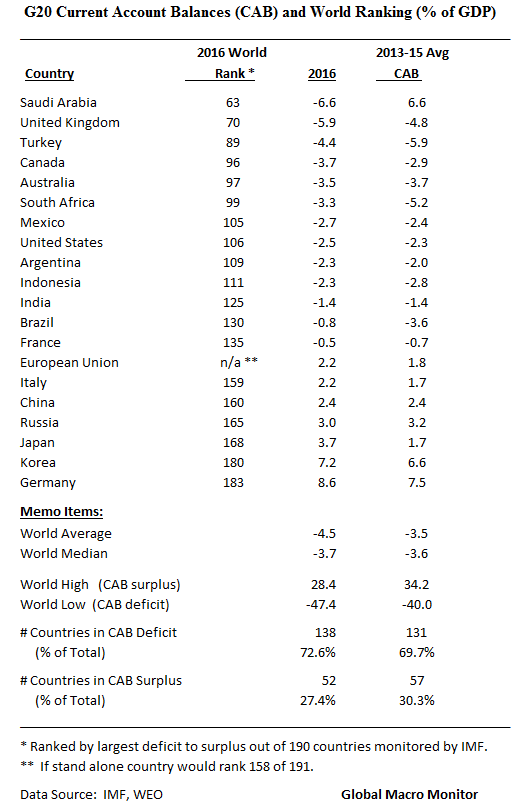

But, first, check out the current account balances of the G20. The world has come along way from the big imbalances at the beginning of the Obama Administration, x/ Germany. Note, only seven countries of the 190 that the IMF monitors has a larger current account surplus with respect to GDP than Germany.

Some economists argue that a large current account surplus limits growth in other countries. German exports to other countries but is not important. The large current account surplus and undervaluation of currency was good for Germany, but it was holding back exports in other countries. If Germany boosted domestic demand and allowed slightly higher domestic inflation, they would provide a much needed boost to global demand and help to overcome unemployment in other countries.

The real problem of the German current account surplus is not for the US (they can still devalue against the Euro and have their own monetary policy). The real problem is faced by countries in the south of Europe who are experiencing severely depressed domestic demand.

Given the imbalances in the Eurozone, southern European economies face a long period of deflation as they slowly seek to restore competitiveness against their northern competitors. However, given European wide austerity, this period of deflation is proving very costly in terms of lost GDP and high unemployment.

If Germany was willing to boost domestic consumption, and temporarily target higher inflation, this would provide greater export demand within Europe. A lower German current account surplus would help increase economic growth in southern Europe. Given the debt crisis and lack of growth, export led growth would be very welcome for easing the depth of the recession.

However, Germany is currently unwilling to pursue any policy which risks a slight deviation from the inflation target. (The ECB increased interest rates in 2011 over concerns about inflation). Therefore, with domestic demand constrained, the German current account surplus is likely to remain. This will be a factor in keeping demand elsewhere in Europe depressed. – Economics Help

G20 current account balances,

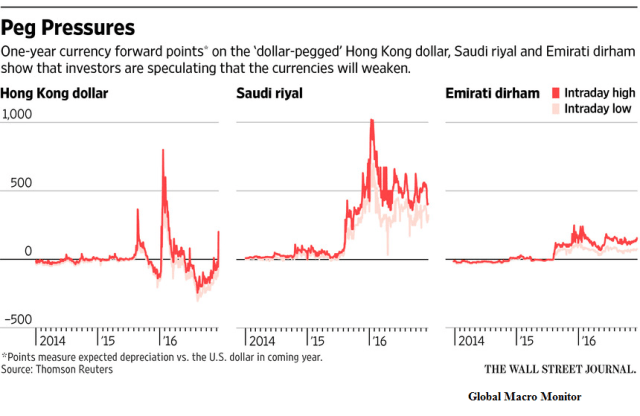

What stands out is the big flip in Saudi Arabia. A perennial exporter of foreign savings, the Kingdom is now running a current account deficit and has to import capital or use up foreign reserves to support it and maintain a stable exchange rate. The Saudi currency and financial markets have come under pressure as the current account surplus has flipped to deficit due to the collapse in oil prices. Hence their desperation to raise oil prices.

The next few years are going to be interesting. If Mr. Trump gets his fiscal policy approved and implemented – large tax cuts and large increases in fiscal spending — by definition, the U.S. current account deficit is going to explode as it did under President Reagan, moving from a small surplus in 1980 to a deficit in 1987 of 3.3 percent in 1987.

Remember the National Accounting Identity,

(S-I) + (T-G) = (X-M)

(S-I) is the ‘private savings balance’ or the difference between private sector savings (S) and investment (I); (T-G) is the ‘government balance’ or the difference between tax receipts (T) and all government expenditure (G); (X-M) is the difference between exports (X) and imports (M) and is usually called the simple ‘current account balance’. –

Given future fiscal policy, unless, private investment or consumption (savings increases) collapses – which is contrary to expectations they both will increase — coupled with a stronger dollar, which we think the index goes to 120 due to rising relative real U.S. interest rates: Presto! — an exploding current account deficit. That “sucking sound” (somethings never change) you will hear in the next few years will be capital flowing in to the U.S. from the rest of the world.

President Trump will thus be very conflicted as we know he doesn’t like trade deficits.

Sum of Current Account Balances

Like all data, there are discrepancies in the IMF data. The world’s current accounts should some to zero. That is, individual current account balances are a zero sum game.

In theory, the sum of world current account balances should be zero. In practice, it never is, and discrepancies can be large. Where do they come from, and what can be done about them? – IMF

Pingback: World Current Account Balances (CAB) – Significance Level