We received some interesting pushback on our recent post, Is the U.S. Government Bankrupt? Not Even Close.

The purpose of the post was to remind readers to not ignore the left side of a government’s balance sheet — assets — and only focus on its liabilities. We quoted President Trump on how he is kicking around ideas about selling some of the federal government’s assets to reduce the national debt.

Readers wrote in — some nasty, probably because we didn’t affirm their doom and gloom views — saying this was not politically feasible and would never happen. We agree on the difficulty of such a policy being implemented. It is not easy for a sovereign, due to domestic politics and even legal issues, to sell assets to pay off its creditors.

Much of our career focused on sovereign debt and working on and working out such issues.

Debt-for-Equity Swaps

During the 1980’s LDC debt crisis, however, there were mechanisms set up to allow the creditors of a sovereign borrowing to swap their debt holdings for equity in, say, a state-owned company. There were many cases of these debt-for-equity swaps. They were not perfect solutions and without problems, but they did exist.

Even now, in Greece, for example, the country’s external creditors always insist on the government pursuing the privatization of state assets with programs negotiated directly into the country’s bailout packages. Greece usually misses the targets and drags its feet on implementation. Imagine, if you will, the domestic political blowback to a government of, say, selling off the Parthenon to pay back German and EU creditors. Yikes!

Sovereign Risk and Debt Crises

But that post is history. We really want to focus on the concept of sovereign risk and debt crises in this post. Why is it that sometimes highly indebted countries experience runs on their currency or can’t roll over their debt? These are complicated issues and should be analyzed case-by-case. But, for this post, we will speak in wide-reaching generalities.

Local Currency vs Foreign Currency

First, it is important to distinguish the difference of a local currency or foreign currency debt problem. As long as the government has an independent central bank, the local currency debt problem can be monetized, which, if happens during a rollover crisis, usually results in hyperinflation and the collapse of the exchange rate. See Bulgaria in the mid-1990’s.

Rarely does a reserve country experience rollover risk, especially since the introduction of mass quantitative easing (QE). We were moving close in the Eurozone in 2011, however, as European financial system was on the brink. Super Mario to the rescue.

We do think that the next major global financial crisis, which a major stock market correction/bear market is not, will be a major industrialized country entering into a period of high rollover risk. That is when we must worry the House of Debt comes tumbling down.

Monetize or Default?

Many now believe that a sovereign borrower with an independent central bank can’t default on its local currency obligations. That the markets will never question its ability to pay.

We disagree, however, as Russia did and defaulted on local currency debt in 1998. In this sort of crisis, where a country falls into the trap where it can’t roll its maturing debt, it comes down to a political decision and who is going to take the pain.

Monetize the debt and the resulting hyperinflation hurts the local population. Default and restructuring the local currency debt hurts the country’s creditors. In Russia’s case, many of the creditors were foreigners, such as hedge funds. Enter the political calculus. Note Russia also devalued the rubble simultaneously with the decision to default, which further hurt its local currency creditors.

Foreign Currency Debt

Most of the recent debt crises — 1980’s LDC Debt, Mexico Peso Crisis (a little more complicated), and the 1997 Asian Financial Crisis – involved transfer risk. This occurs when the debt is denominated in foreign hard currency and the central bank runs out of FX reserves or they fall below a critical level. Even though local currency is available for payment, there are not enough hard currency reserves to convert the local currency thus debt service is disrupted.

Major Reasons for Sudden Stops

Why is it a country gets itself into a debt crisis as the market cuts them off from financing resulting in the sudden stop of capital flows?

We are going to speak into generic terms that can apply to both local and foreign currency debt crises and briefly focus on four major flaws in the structure of the global financial system that contribute to sudden stops and debt crises.

- Lack of Clarity on National Capital Structure – Unlike the private sector sovereign creditors do not have access or explicit knowledge of a sovereign’s capital structure. That is who will be paid first — who are the junior and senior creditors in the capital structure? As reserves decline and rollover risk increases, this only magnifies the nervousness and panic, which accelerates the run or sudden stop of capital flows. The positive feedback loop is to hard break and the restoration of confidence is challenging. In practice, however, countries have implicitly created a de facto capital structure through prioritizing payments. For example, many of the heavily indebted Latin countries would pay some creditors and not others. The IMF and World Bank were de facto senior creditors. Korea restructured the country’s commercial bank interbank lines (not sovereign obligations) and paid its sovereign bonds. Russia defaulted on its domestic debt and paid its euro bonds. The case-by-case, ad hoc nature adds uncertainty. Markets don’t like uncertainty. In the upcoming debt ceiling debate in the U.S., we will probably hear a lot about prioritizing payments as the U.S. government runs low on liquidity.

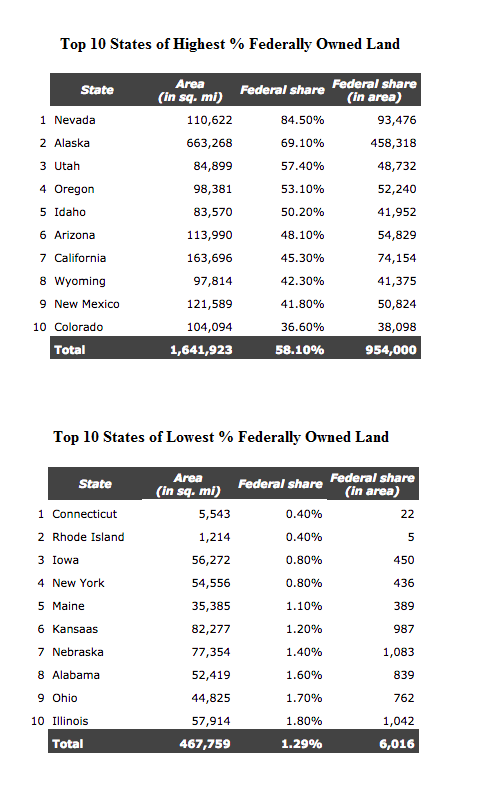

- National Balance Sheet and No Clarity on Assets – In most countries, the markets understand the country/government will be unlikely to use its assets as collateral or sell them to pay down its debt. Therefore the concept of the net worth – assets minus liabilities – is meaningless to the markets. If it were understood upfront the government would allow creditors access to real assets, for example, it would lower the probability of a run on the country and triggering a debt crisis.

- No International Bankruptcy Court – The lack of an international bankruptcy court to adjudicate sovereign debt issues also adds to uncertainty and contributes to country runs and debt crises. However, the recent U.S. court rulings, including the U.S. Supreme Court, in siding with Argentina’s holdout creditors giving them access to the country’s assets seems to be the start of building a body of jurisprudence regarding sovereign bankruptcy issues. This should raise the terminal value of a restructured debt instrument, leading to a less onerous feedback loops during a crisis, less uncertainty, in general, and a greater willingness of buyers to step in during a bond market collapse. What is key here is clarity of the legal jurisdiction under which the bond agreements were written and contracted. We will see if a formal international bankruptcy court for sovereign debt is ever constituted. Maybe when one of the big ones goes down.

- Lack of Clarity of Off-Balance Explicit and Implicit Obligations – One of the lessons of the Eurozone debt crisis was the importance of understanding destabilizing feedback loops. For example, sovereign credit in the periphery countries rapidly deteriorated and reduced confidence in the region’s banking system in a very significant manner. This increased the probability, and in some cases, resulted in the sovereign assuming the liabilities of the banks. This further impaired the sovereign credit and increased the lack of confidence in the banks. This feedback loop was not broken until Mario Draghi at the ECB threatened to use “nukes” in his “whatever it takes” speech.

-

QE by the big four has broken and squashed price discovery in the major global bond markets. What does it mean on a fundamental basis that Italian 10-year yields trade 8 bps through the U.S. 10-year note yield? Absolutely nothing! At least in the emerging markets, there is still a modicum of fundamentals in the determination of sovereign credit spreads.

Upshot. Other than Venezuela (Puerto Rico doesn’t count) and some upcoming noise over raising the debt ceiling in the U.S. there doesn’t seem to be much risk of a major sovereign debtor getting into trouble in the near-term, though some smaller countries are defaulting on their external debt. QE and the threat of QE have changed much in the discipline.

Maybe a credit crisis and accelerated capital flight in China could morph into a crisis, but we are too far from that and have not looked at it closely enough.

A geopolitical event could trigger a sovereign crisis somewhere in the world.

An unexpected political event could trigger a crisis.

A sudden loss of confidence in the Japanese bond market, where the debt ratios are off the charts? The Bank of Japan owns almost half of the JGBS outstanding. And will buy more. In our opinion, there is a greater risk of a currency crisis in Japan than a bond market crisis, but we could be wrong.

A rapid rise in inflation could trigger a sovereign crisis if bonds are allowed to price it in and we enter into a feedback loop of higher deficits, due to higher interest payments, and higher interest rates due to higher deficits. Keep it in mind, but currently not on radar.

President Marine Le Pen? Bingo!

Existential crisis in Europe would trigger a massive blowout of credit spreads and sovereign CDS. Low probability, but high impact event.

We would be buying any panic unless polling changes dramatically, which now puts Macron up around 30 points in the second round. The polls in Brexit and the Trump victories were much closer if not spot on in the last few days. A 30 point lead is a yuuuge and unlikely poling mistake. Buying panic is easier said than done, however, as the changing polls would be why the panic would ensue.

A lot of French voters are still undecided and upset. Who knows what they will do in the privacy of the polling both. Launch the “Molotov” cocktail as the Americans did? Stay tuned.