We hear a lot these days about how all assets are overvalued. Very and don’t disagree.

Lots of gurus and big money managers engaging in market crash talking. Doubt it, but could be wrong. Too much liquidity and cash in the system.

The repressed -lower than non-market – risk-free interest rates provide the theoretical foundation for overvaluation as cash flows are discounted at an artificially low discount rate. However, though over/undervaluation is a theoretical/subjective/historical concept, price is the reality that determines valuation and is driven by good old fashion buying and selling. Capital flows, my friends.

I remember the days when i-banking analysts would come and see me at the hedge fund where I worked in the mid-1990’s talking about where credit spreads should be valued and trading. I always retorted, “let me know when you see the buyers show up that will drive the spreads to those valuations.”

The buyer finally showed and its name was Long Term Capital Management. The problem was they bought with tremendous amounts of leverage and there were no buyers and liquidity when they needed to sell. And, in hindsight, they were just about the only buyers which drove spreads to where they deemed were correct valuations. In other words, they were the market.

Just before the 2008 financial crisis, the justification for overvaluation of almost all asset classes, including housing was “excess global liquidity”. “Can’t fight the wall of money.” “Money, money, everywhere.” I wrote a piece in December 2006, The Global Flood (of Liquidity),

There’s little doubt financial historians will find the first half of the first decade of the new millennium fascinating. The hindsight of history will allow for better analysis of the factors which drove the general and significant repricing of risk in both financial and real assets. Much of the focus will be on improved fundamentals, such as the low inflationary growth “Goldilocks” economy, the rise of China and India, productivity gains and corporate profit growth, and gains from globalization.

The great debate, however, will be over the timing of the move and simultaneous price breakouts in asset and commodity markets. The sharp rise in home prices, collapse of credit spreads, flattening of yield curves, rise in commodity prices, strength of foreign currencies against the dollar, rally in global equity markets, and decline in implied volatility all began in late 2002 – early 2003. Can the longer term fundamentals explain what appears to be the “commoditization” of asset markets, which seemed to take place over night?

There are no mystical forces that drive market prices, which ultimately move on supply and demand. Unlike a relative price move, a general repricing of assets is usually the result of a significant shift in liquidity conditions and monetary factors, which increases global demand for everything from goods and services to financial and real assets. As the economy “dishoards” excess liquidity, prices tend to rise across the board. – The Global Flood (of Liquitidy), Dec 2006

I asked a prominent economics professor to review and comment on that piece. He said I needed to distinguish the difference between liquidity created by central banks and credit in the system. Credit was leverage. How prescient.

It was the global credit bubble that drove all assets markets in mid-2000’s which ended up in, well, you know.

Today we have pockets of credit bubbles, in auto lending, student loans, the fracking sector, for example, but it just doesn’t feel, in our opinion, systemic as it did in 2007-08

No doubt debt has increased, much of it developed market sovereign which has been monetized by quantitative easing, resulting in repressed interest rates and a structural shortage of tradeable risk-free bonds.

The data show the Fed owns about 35 percent of Treasury securities with maturities 10-years or longer. Note the data only include notes and bonds and excludes T-Bills.

The Fed’s holdings combined with foreign ownership of longer maturities — more than 1-year — exceeds 80 percent of marketable Treasuries outstanding. The Fed combined with just foreign official holdings, mainly, foreign central banks, is 65 percent of maturities longer than 1-year. Thus, almost 2/3rds of tradeable Treasuries longer than 1-year are held by entities with no sensitivity to market forces. – The Broken Bond Market, GMM, March 2017

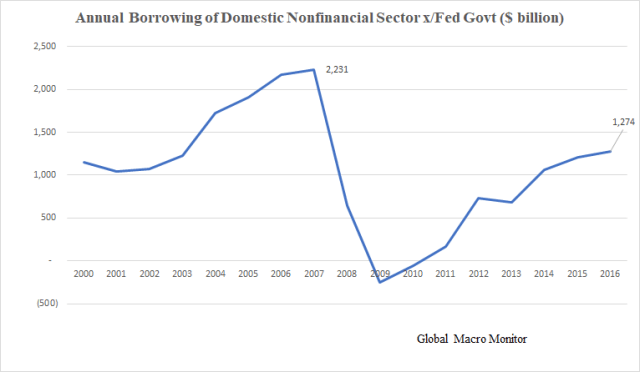

But take a look at the data. The chart below from the Fed’s Flow of Funds data show that total annual borrowing of the domestic nonfinancial sector excluding the Federal government is only back to the levels where it was in 2003. Furthermore, total borrowing excluding the Federal government in 2016 was only 57 percent of the peak borrowing in 2007.

.

Note also the net borrowing excluding the Federal government was net negative during the height of the crisis. No credit growth, no economic growth.

…credit is the mother’s milk of growth; without credit the economy cannot flourish.– Mark Zandi

Nevertheless, the data seems to indicate, at least to us, the economy is not as leveraged as it was in 2007, though big banks are bigger and the Federal government has almost doubled the size of its debt, but most of which, 65 percent of longer-term securities, are held by the Fed and foreign central banks.

Paradoxically, the Federal government has almost doubled its debt over the past 10 years and the markets suffer from a shortage of Treasury securities.

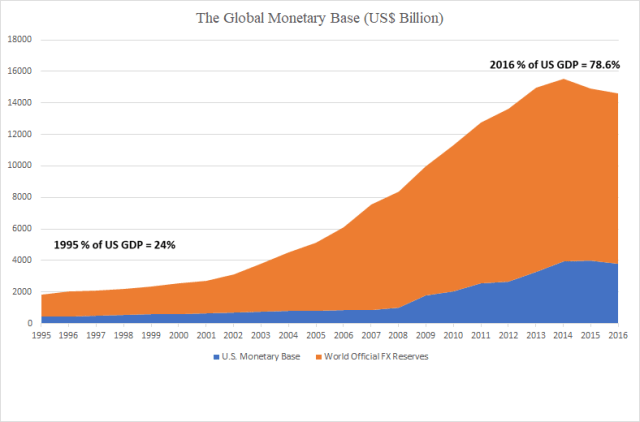

Global Monetary Base

That brings us to the chart that floats all valuation boats.

We have estimated a global liquidity concept called the “global monetary base” which is simply the sum of the U.S. monetary base and the world’s official foreign exchange reserves. Since most of the official FX reserves — about 65 percent — are held in dollars most of the global monetary base is in the U.S. financial system.

Note that in 2007 the global base was at about 50 percent of U.S. GDP compared to almost 80 percent at the end of 2016.

Conclusion

The U.S. financial system is flush with liquidity as measured by the global monetary base and has declined only slightly over the past few years, mainly due to China’s reduction in foreign exchange reserves (which has ended up in NY and California real estate) and some valuation effects of the dollar.

This liquidity, in our opinion, coupled with artificially low rates keeps the overvaluation of assets afloat. Remember, it wasn’t until the deleveraging process began in 2007-08 did overvalued assets crack. Markets need a catalyst to regress back to long-term or overshoot their equilibrium valuations.

Our sense the overvaluation will work off through time unless inflation really begins to pick up and the Fed has to accelerate the pace of balance sheet reduction. Or it could be some type of geopolitical shock, where assets immediately reprice with very little trading. This is not to say there won’t be minor corrections or occasional flash crashes due to the asinine techno geek trading systems that now dominate the markets.

We could be wrong. Godot may just show up tomorrow.

Pingback: 04/27/17 – Thursday’s Interest-ing Reads | Compound Interest-ing!

Pingback: Weekend Reading: Trumponomics – End Of 100 Days | RIA

Pingback: Weekend Reading: Trumponomics – End Of 100 Days – Earths Final Countdown

Pingback: Weekend Reading: Trumponomics – End Of 100 Days | Zero Hedge

Pingback: Weekend Reading: Trumponomics – End Of 100 Days | Domainers Database

Pingback: Weekend Reading: Trumponomics – End Of 100 Days - Investing Matters

Pingback: Weekend Reading: Trumponomics – End Of 100 Days - BuzzFAQs

Pingback: Weekend Reading: Trumponomics – End Of 100 Days | High Priority News

Pingback: George Orwell’s Monetary Policy | NewZSentinel

Pingback: George Orwell’s Monetary Policy | It's Not The Tea Party