Monetary policy history made today.

The Federal Open Market Committee (FOMC) confirmed it would begin its long-awaited quantitative tightening (QT).

In October, the Committee will initiate the balance sheet normalization program described in the June 2017 Addendum to the Committee’s Policy Normalization Principles and Plans. – FOMC, September 20

They also left another rate hike on the table this year. The average dots remained fairly constant: 2017 – 1.41 percent; 2018 – 2.04 percent; 2019 – 2.63 percent; 2020 – 2.85 percent; and Long Run – 2.78 percent.

The dots imply about seven more rate hikes in this cycle. The longer run median dot came in a bit from the last meeting (see Yellen’s comments below).

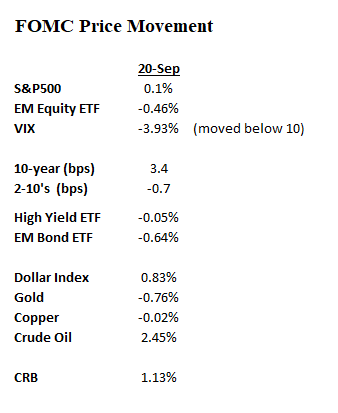

Market Reaction

The markets took it all in stride as in one big double cheese non-burger. Just as we expected.

It may take the markets a few days to digest the FOMC actions before we get a clearer picture of the direction of the markets.

All other things remaining equal — and they never do – it is going to take a while for this tightening cycle to start biting. Rates are still too low, and there is too much central bank liquidity in the system.

Just check out the bull market in almost everything since the Fed began Orwellian tightening nearly two years ago, albeit at a snail’s pace, just as they said they would.

On the margin, we do expect volatility to pick up a bit, however. QT is just another grain of sand piling up in the structured criticality paradigm of global markets that could cascade into a series of avalanches.

Time to be a tourist and not a permanent resident.

All Eyes On European Bonds

Now we turn our eyes to the European bond market bubble.

We will be posting a daily table of interest rate changes and movements in various sovereign spreads to the German Bund. Whoever is left holding euro-denominated bonds has to be nervous after the Fed move today. They surely know the ECB beckons.

Who is going to buy those bonds at such low rates with growth and inflation picking up?

Prayers for those who took down the mega-long duration 100-year Austrian bonds at 2.10 percent. A move of 100 bps will almost slice the bond price in half. The Austria 30-year currently yields around 1.60 percent. A great deal, no?

Will the euro be around in 10 years, much less 100 years? We suspect many flippers in that deal gaming a short-term interest rate move.

A sign of the top? Do you hear those bells ringing?

October Sell Off

The soon to come European bond market temper tantrum is the external shock we expect to ignite a decent sell-off in global risk markets in October. There are other events, such as an economic or policy shock coming out of China’s 19th National Congress of the Communist Party, that can also rock the markets.

Don’t discount a potential big macro swan coming out of Washington either.

We are not looking for a bear market, but a decent size flash-type crash that may last a few days or a few weeks, which can be bought. Everyone is waiting to pounce — until volatility spikes and fear takes over. It should be fast and furious, especially with the rise of the buy the dipper algos and trading ‘bots.

Mr. October on deck. Stay tuned.

Money quotes from Chair Yellen’s presser:

- Nonetheless, our understanding of the forces driving inflation isn’t And in light of the unexpected lower inflation readings this year, the Committee is monitoring inflationdevelopments closely.

- we continue to expect that the ongoing strength of the economy will warrant gradual increases in that rate to sustain a healthy labor market and stabilize inflation around our 2 percent longer-run objective.

- That expectation is based on a review that the federal funds rate remains somewhat below its neutral level. That is, the level that is neither expansionary nor contractionary and keeps the economy operating on an even keel.

- Because the neutral rate currently appears to be quite low by historical standards, the federal funds rate would not have to rise much further to get to a neutral policy stance. But because we also expect the neutral level of federal funds rate to rise somewhat over time, additional gradual rate hikes are likely to be appropriate over the next few years to sustain the economic expansion.

- the median estimate of the longer run normal value edged down to 2.8 percent.

- our balance sheet will decline gradually and predictably. For October through December, the decline in our securities holdings will be capped at $6 billion per month for treasuries and $4 billions per month for agencies.

- These caps will gradually rise over the course of the following year to maximums of $30 billion per month for treasuries and $20 billion per month for agency securities, and will remain in place through the process of normalizing the size of our balance sheet.

- by limiting the volume of securities that private investors will have to absorb as we reduce our holdings, the caps should guard against the outsized moves in interest rates and other potential market strains.

- changing the target range for the federal funds rate is our primary means of adjusting the stance of monetary policy. – Chair Janet Yellen, September 20

Appendix:

Here is the Addendum, from the June FOMC meeting referenced in today’s release.

Addendum to the Policy Normalization Principles and Plans

All participants agreed to augment the Committee’s Policy Normalization Principles and Plans by providing the following additional details regarding the approach the FOMC intends to use to reduce the Federal Reserve’s holdings of Treasury and agency securities once normalization of the level of the federal funds rate is well under way.1

- The Committee intends to gradually reduce the Federal Reserve’s securities holdings by decreasing its reinvestment of the principal payments it receives from securities held in the System Open Market Account. Specifically, such payments will be reinvested only to the extent that they exceed gradually rising caps.

- For payments of principal that the Federal Reserve receives from maturing Treasury securities, the Committee anticipates that the cap will be $6 billion per month initially and will increase in steps of $6 billion at three-month intervals over 12 months until it reaches $30 billion per month.

- For payments of principal that the Federal Reserve receives from its holdings of agency debt and mortgage-backed securities, the Committee anticipates that the cap will be $4 billion per month initially and will increase in steps of $4 billion at three-month intervals over 12 months until it reaches $20 billion per month.

- The Committee also anticipates that the caps will remain in place once they reach their respective maximums so that the Federal Reserve’s securities holdings will continue to decline in a gradual and predictable manner until the Committee judges that the Federal Reserve is holding no more securities than necessary to implement monetary policy efficiently and effectively.

- Gradually reducing the Federal Reserve’s securities holdings will result in a declining supply of reserve balances. The Committee currently anticipates reducing the quantity of reserve balances, over time, to a level appreciably below that seen in recent years but larger than before the financial crisis; the level will reflect the banking system’s demand for reserve balances and the Committee’s decisions about how to implement monetary policy most efficiently and effectively in the future. The Committee expects to learn more about the underlying demand for reserves during the process of balance sheet normalization.

- The Committee affirms that changing the target range for the federal funds rate is its primary means of adjusting the stance of monetary policy. However, the Committee would be prepared to resume reinvestment of principal payments received on securities held by the Federal Reserve if a material deterioration in the economic outlook were to warrant a sizable reduction in the Committee’s target for the federal funds rate. Moreover, the Committee would be prepared to use its full range of tools, including altering the size and composition of its balance sheet, if future economic conditions were to warrant a more accommodative monetary policy than can be achieved solely by reducing the federal funds rate.

- The Committee’s Policy Normalization Principles and Plans were adopted on September 16, 2014, and are available at www.federalreserve.gov/monetarypolicy/files/FOMC_PolicyNormalization.pdf. On March 18, 2015, the Committee adopted an addendum to the Policy Normalization Principles and Plans, which is available at www.federalreserve.gov/monetarypolicy/files/FOMC_PolicyNormalization.20150318.pdf. Return to text

Last Update: June 14, 2017

Pingback: lemeaex2

Pingback: Caught in the Political Crosswinds | lemeaex2