Q1: Lake Placid To The Mavericks

The markets closed out the quarter trying to recover from one of the biggest volatility shocks in history, which began in early February. The question for Q2 is: Was the v-shock a one-off or a regime change? We lean toward the latter.

The next quarter will likely be a battle between the cyclical bulls and structural bears.

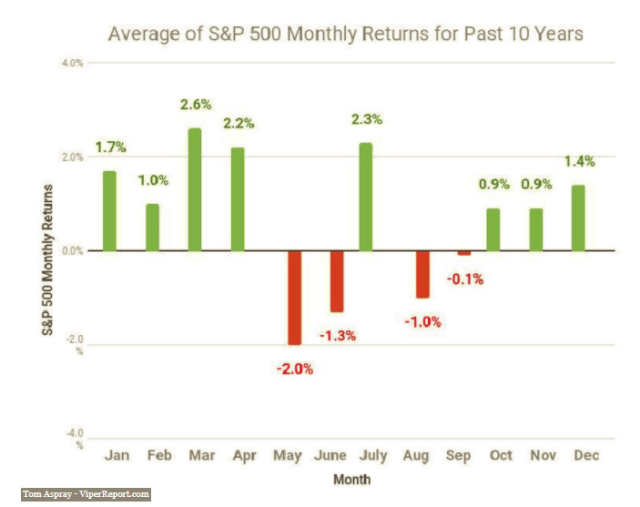

The bulls have the strength of current earnings, which may, or may not be priced (probably the later as the market is still at extreme valuations). Furthermore, short-term indicators reflect too much bearishness – put-call ratio high at 134 percent. Thus, we wouldn’t be surprised by a big push and full on frontal assault by the bulls in the first part of the quarter. Seasonals also favor April.

Da’ Bears

The structural bears have, what appears to be, a shifting of the tectonic plates underlying the global bull market in stocks. That is the ground in shifting before the markets’ feet.

Structural Shifts

Growing wealth and income inequality – just eight people own as much wealth as half of the world’s population; the decline of the liberal economic and political order, which has been the backdrop of the bull market; the end of the bull market in bonds; the end of quantitative easing (QE); the erosion of U.S. world leadership; increasing trade and geopolitical frictions; the rise of populism; increased concern over U.S. budget deficits and excess debt; and the growing doubts about dollar supremacy, among others.

But those macroeconomic outcomes result from policy decisions abroad and the market-clearing movements of financial prices. Officials in important emerging-market economies chose to accumulate Treasury securities, because US yields, albeit low, were higher than in other advanced economies. A confrontational stance on trade, together with greater reliance on government debt, may well extract a higher toll to balance flows of goods and services and of capital. Moreover, the US will be paying for its current excesses with the promise of future payments, and inefficient stimulus now will not give future generations the productive resources needed to make good on it. – Carmen Reinhart, Project Syndicate, March 30

That is more than a wall of worry, in our opinion.

The Coming Donnybrook

We expect a major donnybrook between the cyclical bulls and secular bears in the coming quarter, which may be the most important quarter in the financial markets in the past 50 years. The natural trajectory are for markets to move north.

Finally, the markets are going to be the final political arbiter on whether the Trump administration: is #Making America Great Again (MAGA), or ruining the country and its standing in the world.

No political statement here, we will leave it to the markets to decide.

The biggest risk is that we now live in an asset driven global economy, which is prone to perverse feedback loops.

Stay tuned.

.

.

.

.