We heard a market pundit today mention the Fed will soon begin to taper its reduction in the balance sheet. The pundit seemed convinced the balance sheet reduction is on track to total $600 billion per year as far as the eye can see. Not so, Joe!

The balance sheet reduction is on automatic pilot in so far as the monthly maturities coming due in the Fed’s SOMA portfolio of Treasury securities and MBS are not rolled over. That is the total monthly size of QT is dependent on the maturity profile of the SOMA portfolio. The second derivative – the change of the change in the SOMA portfolio – is sharply negative as the maturity profile in each successive year gets smaller (see table). No Fed tapering needed, Joe!

If the total Treasury maturities for any month exceed $30 billion, for example, the difference of the total less $30 billion is reinvested back into the monthly auctions across the curve.

The mechanics of the MBS run-off are more opaque as not only we don’t have any maturity data there is also uncertainty due to refinancings. We estimate the 2019-2021 MBS run-off based on an assumption of a running rate of 52 percent of the monthly Treasury reduction, which is the ratio since the balance sheet reduction began in October 2017.

Upshot

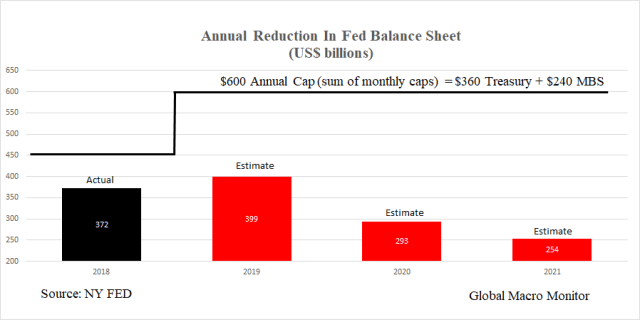

The following table illustrates that the Fed’s balance sheet reduction naturally falls simply due to the profile of its maturities in the SOMA portfolio. Quantitative tightening does not come close to $600 billion that the market clowns were freaking out about over Christmas. In 2021, the balance sheet reduction is estimated to be only $254 billion, which is just 42.27 percent of the $600 billion cap! Still, the Fed balance sheet at the end of 2021 will remain around 3.5x its pre-crisis size in 2007.

Remember the idjits proclamation , “the Fed and Jay Powell know nothing,” at the nadir of the recent crash? What a joke!

This confirms our suspicion the market crash from October to December was likely misdiagnosed. Maybe what ails the market is not solely a cyclical phenomenon and about the Fed, but something more structural, such as too much new debt being floated by the Treasury and the inability of the risk-free rate to rise and find its market clearing level. More on this in a later post.

Nevertheless, it will be interesting to see if stocks can continue to rally on, what we believe, is a false narrative. Stay tuned.

Help keep the lights on at the Global Macro Monitor.

Contribute any amount based on your perception of our value added by clicking the PayPal donate widget at the right side of the screen. Thank you!

PayPal says invalid session when I click on the link

Thanks, Ahsan. Try clicking on the PayPal donate widget on the right-hand side of the blog. Thanks, again!