Five Key Facts:

- BYD’s Stella Li projects China’s EV market share could rapidly approach 80% of new car sales.

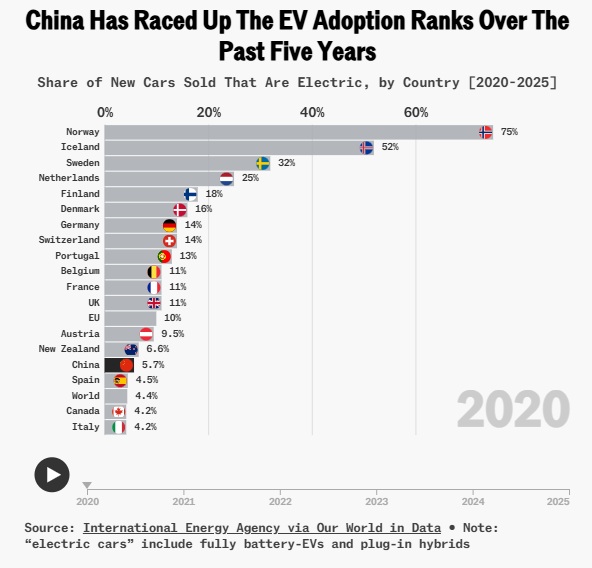

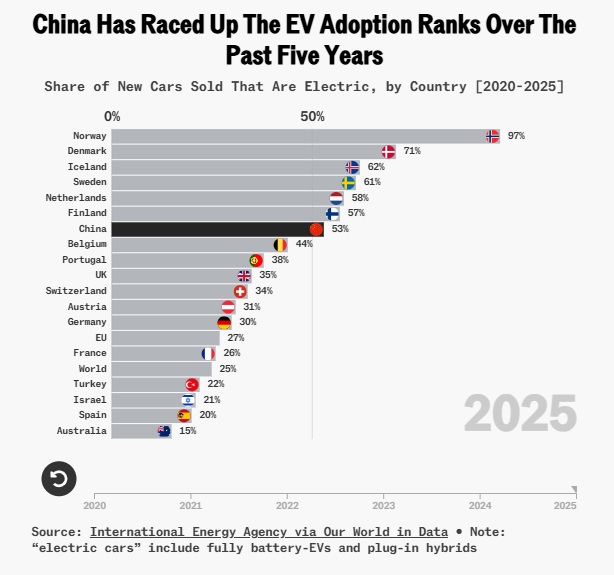

- China’s EV penetration jumped from 6% of new car sales in 2020 to 53% in 2025.

- China accounted for 60% of global EV sales and over half of the global EV sales increase in 2025.

- China’s EV exports rose 78% year-over-year in Q1, with BYD’s European registrations up 115% in April (vs. Tesla’s 47%).

- US EV adoption remains around just 10% of new car sales, hampered by weak policy support and expired tax credits.

China’s electric vehicle market is approaching a structural threshold that international economists and portfolio managers should be watching closely. BYD Executive VP Stella Li recently told CNBC that China’s EV penetration could “very quickly” approach 80% of new car sales, building on a base that the IEA describes as having grown at an extraordinarily rapid pace over the past five years.

The trajectory is striking. In 2020, electric cars accounted for just 6% of new car sales in China; by 2025, that share had surged to 53%. For context, that’s a near-tenfold increase in five years — a pace of structural transformation rarely seen in any major economy’s transportation sector, let alone the world’s largest auto market.

China’s dominance isn’t confined to its domestic market. The country accounted for six out of every ten EVs sold globally in 2025, and more than half of the entire global increase in EV sales that year. This single data point underscores why China effectively sets the tempo for the global EV supply chain — from battery materials to charging infrastructure standards.

What’s most relevant for international economists is the export dimension. China’s EV exports surged 78% year-over-year in the first quarter, while BYD’s new car registrations in Europe jumped 115% in April compared to a year earlier, more than double Tesla’s 47% growth in the same market. This export acceleration arrives even as domestic demand growth wobbled slightly after a trade-in subsidy program was temporarily paused, suggesting Chinese automakers are increasingly looking outward to absorb excess production capacity, a dynamic with direct implications for trade tensions, tariff policy, and industrial competitiveness in Europe and beyond.

The contrast with the US is stark. Electric cars still represent only around 10% of new car sales in the US, a market under pressure from weaker policy support, expired federal tax credits, and limited access to cheaper Chinese models.

For investors and policymakers, the takeaway is twofold: China’s EV ecosystem, from BYD to battery suppliers to charging networks, is compounding advantages that will be difficult for competitors to close, and the export wave now hitting Europe will likely intensify debates over tariffs, industrial policy, and “de-risking” strategies. The widening gap between China’s adoption curve and America’s stagnant one also raises longer-term questions about competitiveness in a sector increasingly central to manufacturing employment and energy policy on both sides of the Pacific.

The global EV race has left the starting gate and America’s still checking its tire pressure on a horse-drawn cart.