Markets Navigate a Hawkish Fed Surprise as Asia Surges on AI Wave

Week Ending June 19, 2026

Markets delivered a split verdict this week — a resurgent Asia riding the AI/semiconductor wave higher, while Wall Street grappled with a Fed that just reminded investors it still has a trigger finger.

The Fed Drops the Hawk

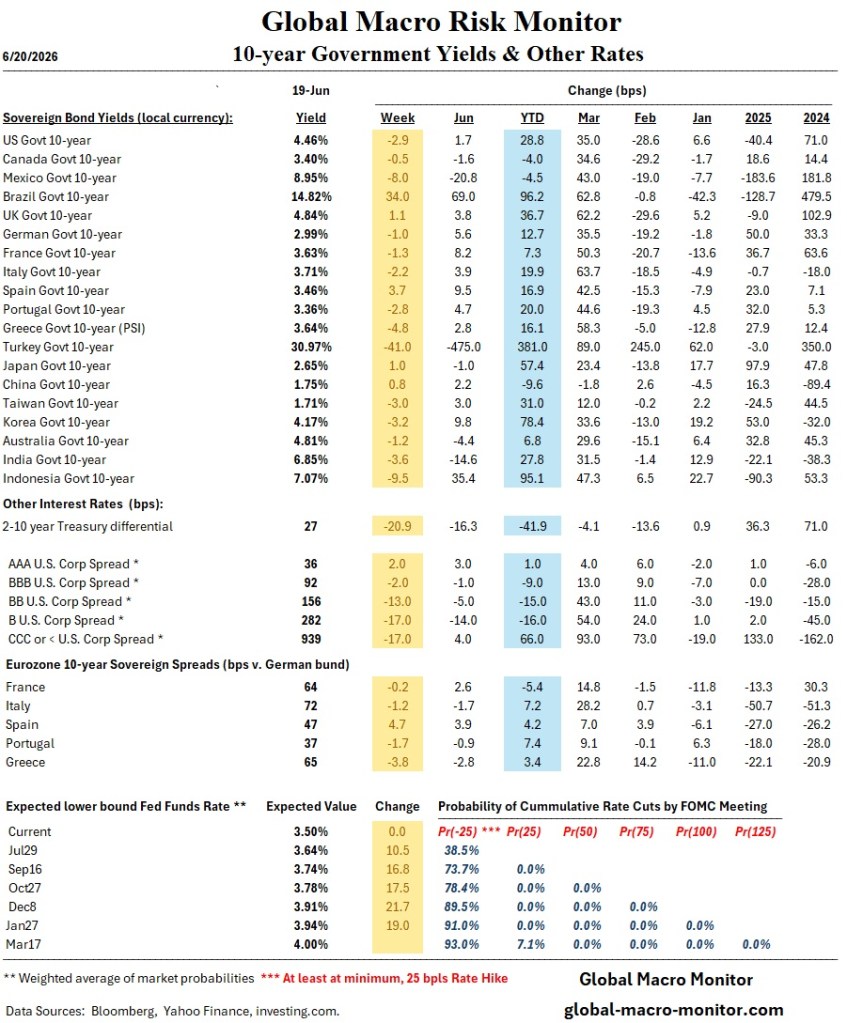

The week’s defining event was Kevin Warsh’s first FOMC meeting as Fed Chair, and he wasted no time establishing his credentials as an inflation hawk. Rates were held steady at 3.50–3.75%, but that was the last dovish thing about Wednesday afternoon. The updated dot plot was a gut-punch: nine of 18 officials penciled in at least one rate hike in 2026, with six projecting two or more. Warsh declared price stability the committee’s “North Star” — strong, unanimous, and unambiguous. Translation: the Fed’s easing narrative is dead.

The market reaction was swift. The 2-year Treasury yield spiked 15 basis points, briefly touching a 52-week high of 4.21%. The S&P 500 shed roughly 1.4% and the Nasdaq dropped 1.5% on Wednesday, though dip buyers salvaged the week by Thursday’s close.

The rate market is now doing the math. The probability of a July hike has jumped to 40%, and markets are pricing a 90% chance of at least one hike by December. This is a seismic shift from just two weeks ago, when a 2027 rate hike felt like a stretch.

Warsh also buried forward guidance — he stated it’s no longer suited to the current policy environment. Buckle up. Every data release now matters.

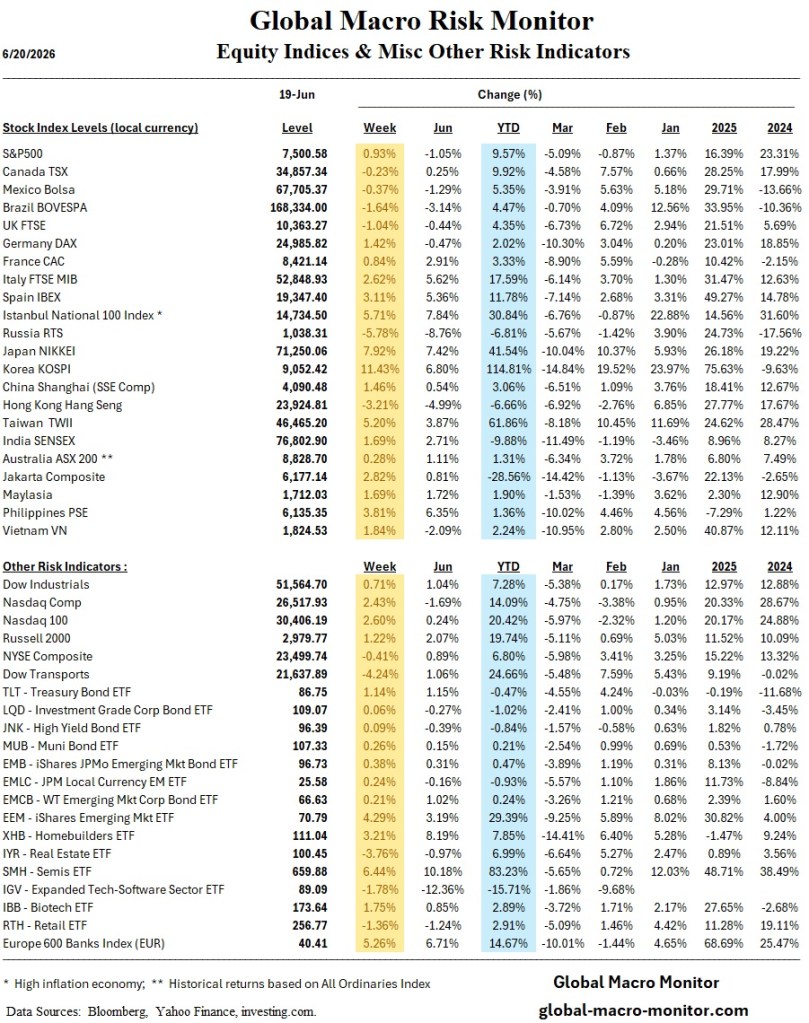

Asia Rips; Semiconductors Lead the Charge

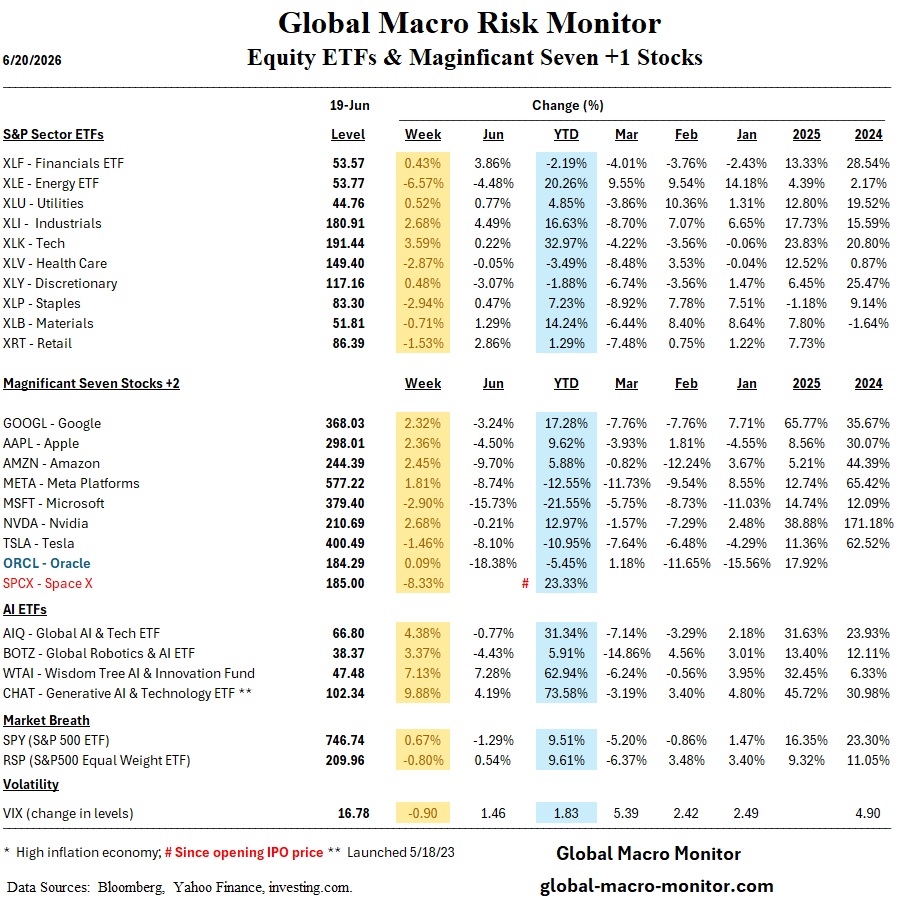

While Washington rattled nerves, Asia was ripping. Japan’s Nikkei surged 7.6% on the week, hitting fresh all-time highs, with semiconductor equipment and AI-linked tech stocks leading the charge. Korea exploded over 11%, powered by the global semiconductor rally. The PHLX Semiconductor Index (SOX) also notched fresh all-time highs stateside, and AI names broadly outperformed. The AI infrastructure buildout theme remains firmly in its expansionary phase — compute demand still outstrips supply, and the market is rewarding that scarcity aggressively.

Geopolitics Provides a Tailwind

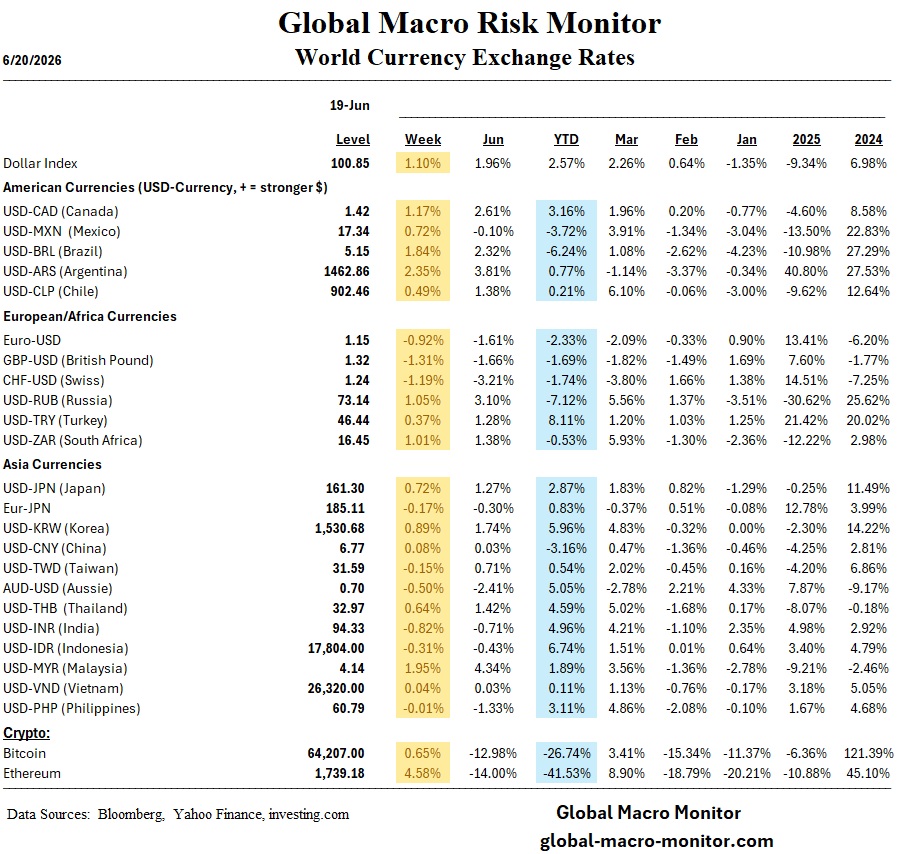

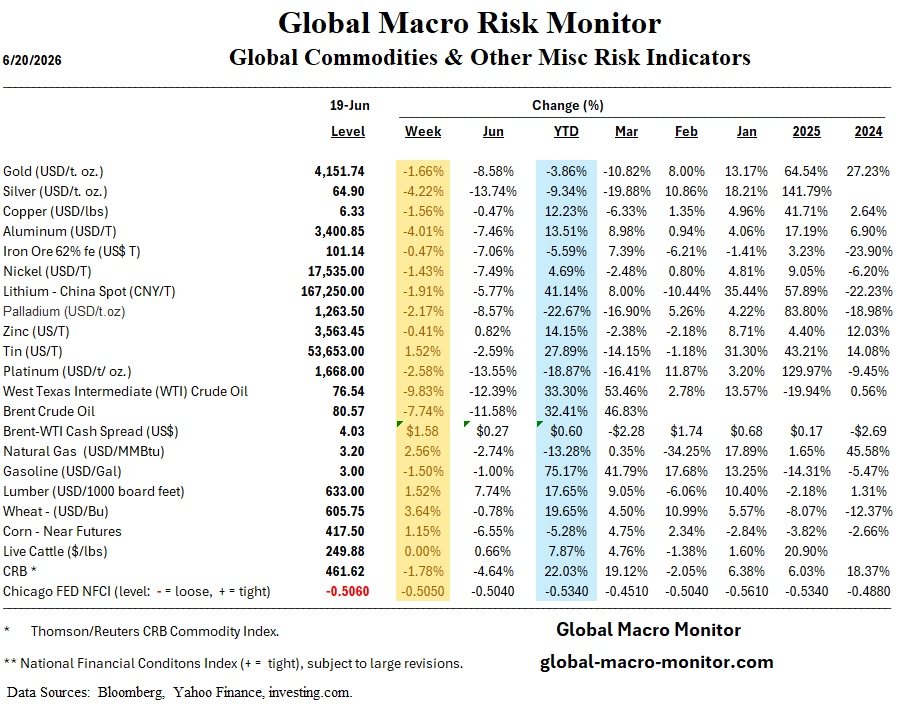

A U.S.-Iran memorandum of understanding, clearing a path to reopen the Strait of Hormuz, sparked a sharp Monday rally and sent oil prices tumbling toward $75/barrel — down nearly 40% from conflict peaks. Lower energy prices provided some inflation relief, though the hawkish Fed quickly overshadowed that narrative.

The Bottom Line

The bull market’s two pillars — 20%-plus earnings growth and AI infrastructure spending — remain intact. But the Fed has drawn a line. With rate hike odds surging and Warsh signaling data-dependency without a policy roadmap, volatility is the price of admission going forward. Asia’s momentum is real, AI is real — but so is the Fed.

Watch the PCE report Thursday and Micron’s earnings next Wednesday. Both could move markets significantly.