Summary

- The market is irrationally obsessed with the “$600 billion” annual roll-off in the Fed’s balance sheet

- The actual reduction in the balance sheet will be much smaller and is determined by the profile of monthly Treasury and MBS securities maturing in the SOMA portfolio

- The balance sheet reduction will not come even close to the zip code of a $600 billion annual reduction

- The asymmetrical liability accounting of QT versus QE makes the runoff look similar to a quasi-deficit financing

- By conveying to the market the balance sheet will not be reduced by $600 billion annually and announcing an annual cap of, say, $450 billion, the Fed Chair could spark a massive nutcracking short-covering rally, in our opinion

- Maybe he should. Maybe he will

It is truly stunning to watch, what some academics believe to be, an efficient market come unglued over the Fed’s “$600 billion annual balance sheet reduction”

Recall the Fed announced to its “Normalization Principles and Plans” at the June 2017 FOMC meeting,

Source: FOMC

Those are frickin’ caps, not levels!

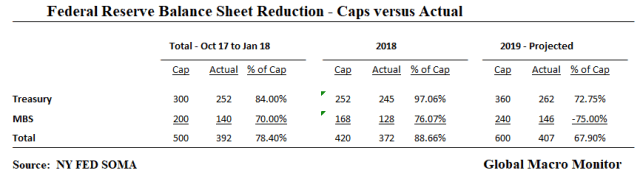

The Fed began their balance sheet reduction in October 2017 and has reduced, as of January 23rd, its holdings of Treasury securities by $252 billion and MBS by $140, which is only 78.40 percent of the cumulative monthly caps mentioned in the normalization statement. Why is this so?

Maturity Profile Verus Monthly Caps

Simply because the balance sheet run-off depends on the profile of Treasury and MBS securities maturing in the SOMA portfolio in any given month. For example, this month – January 2019 – only $11.7 billion of Treasury securities mature in the Fed’s SOMA portfolio, not even close to the $30 billion cap, which the market tends to get all worked up over.

Next month, however, $56 billion will mature. The Fed will not rollover $30 billion — that is the cap will be binding — reducing the Treasury’s cash balance held at the Fed (the liability side) by $30 billion. The remaining $26 billion will be rolled over into the February monthly Treasury auctions across a spectrum of maturities.

Only four out of the twelve months in 2019 will the $30 billion cap on Treasury securities be binding and gets better in the out years.

The MBS portfolio is less transparent and harder to measure due to prepayment uncertainty. Moreover, we don’t have the data on the maturity profile and use an assumption that MBS maturities are equal to around 55 percent of the Treasury securities. which has been the case since October 2017 beginning of QT.

Our estimates are very sensitive to this assumption and could likely be too low. Only the Fed know, or knows better.

Fed’s Accounting Difference of QE versus QT

Given the asymmetric liability accounting of quantitative tightening (QT) – a reduction of Treasury cash balances at the Fed – versus quantitative easing – an increase in bank reserves – we conclude that QT is much more like a fiscal operation than monetary policy. There is little evidence the balance sheet reduction is restricting credit and loan creation.

The Treasury has to issue more bonds and notes to maintain its cash balances (checking account) at the Fed, which makes it similar to quasi-deficit financing.

During QE, however, the Fed bought Treasury securities in the secondary market through increasing reserves in the financial system (liability), allowing among other things, investors to reallocate into riskier securities while keeping interest rates down.

The extra liquidity in the banking system did not translate into credit expansion (an increase in endogenous money), no surprise, but counter to our expectations, no panic over money printing as it would have in an emerging market resulting hot potato money. Ergo no goods and services inflation, only asset inflation and FOMO panic. The advantages of a reserve currency.

We are not so sure the next round of QE will be so benign, however. Sorry, my MMT brothers and sisters.

Changing Mr. Market’s Perception

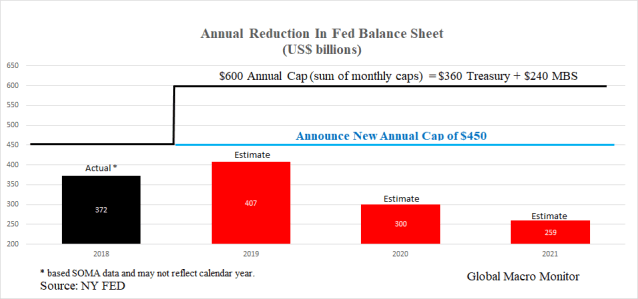

Nevertheless, as illustrated in the tables and chart, and unless our estimates are wrong, Mr. Powell and the FOMC can ease the market fears by simply announcing the annual cap on the balance sheet will be reduced to $450 billion from $600 billion through 2022. Markets will rally on this nonsense even though the $600 billion annual cap was never binding in the first place, simply due to the maturity profile of the SOMA portfolio.

There are times when Mr. Market doesn’t do its homework and is repulsed by the details and the minutiae of monetary policy. We believe this is one of those times.

Totally absurd but it’s today’s reality and we have seen much worse.

Potemkin monetary policy. Just as in the Korea-U.S. Free Trade Agreement.

South Korea, meanwhile, negotiated a permanent steel-tariff exemption in exchange for allowing additional U.S. auto imports. But the claim of a “renegotiated” Korea-U.S. free-trade agreement should be viewed with skepticism. U.S. automakers already don’t export the allowable number of cars into South Korea today, let alone the expanded number. And South Korean car exports, the main sources of the trade imbalance, were left alone. It was a limited, face-saving deal that everyone can tout as “preventing” a trade war. – New Republic