#CKStrong

During my EM trading days, I realized that all the juice had been squeezed from the more advanced emerging market bonds, such as Mexico, Brazil, Argentina, and Poland. So I started buying up the “exotic penny stocks,” such as Sudan distressed debt, which had been in default for years and trading with a $0.02-$0.04 bid/offer spread. Note the offer price is a 100% mark-up on the cash bid price. Today’s liquid coupon bonds trade with a bid/off differential of at most $0.125, and that’s considered expensive.

We lined up a ton of buyers, mainly hedgies, who really understood the MoMo markets,, at $.04, the offer price. I bought CHF500 million (could have been US$ as my memory is fading). The Swiss Bank trader laughed at me when we did the trade.

Ironically, it was a Swiss based hedge fund that took almost all the floatable Sudan debt at the top, at about $.15, before the market collapsed. I saw that trader in a NYC restaurant about six months later and asked why he was buying at $.15?

“Because we thought it was going to $.30.”

I asked him why. He couldn’t answer.

Useful Delusions

I had learned if you could get the price moving higher, a momentum market with no intrinsic value will always find a way to delude itself, retrofitting fundamental reasons to justify the rising price. Soon after I made the initial purchase of Sudan debt and the price began to ramp, there was a rumor in the market that my firm, and I personally had a United Nations mandate to buyback Sudan’s debt.

We never confirmed or denied the rumor but knew exactly what was going on.

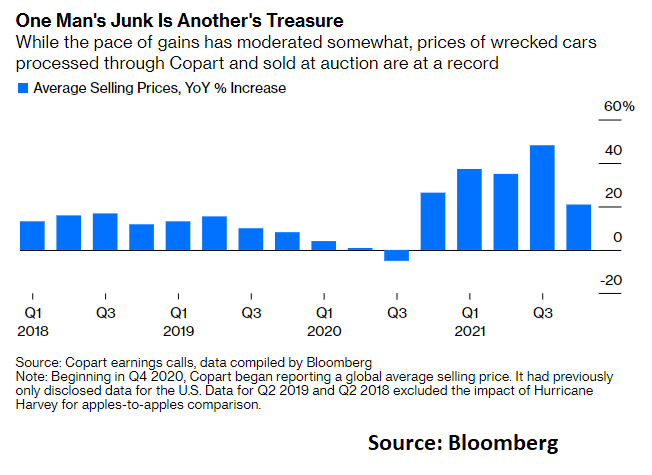

Distressed Junk Cars

Take a look at the price of totaled cars. I just sold one for $1500. Could. Not. Believe. It.

Isn’t the supply of wrecked cars about to spike with all the cars lost to Hurricane Ida?

Though quite a bit different market, some things never change,

Even turkeys can fly in [or after] a hurricane.

Sound or look familiar?

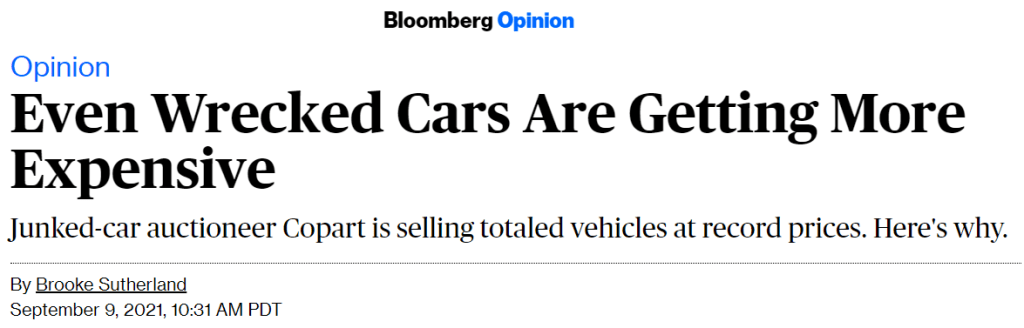

See article here.