A reasonably informative video below, especially regarding inflation.

Not much mention of the growth of money driving excess demand, however.

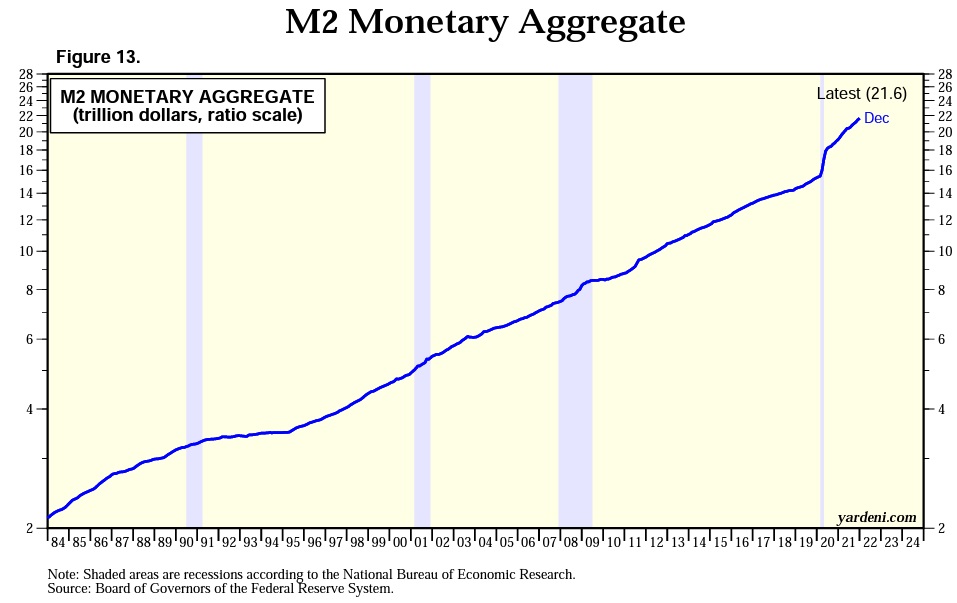

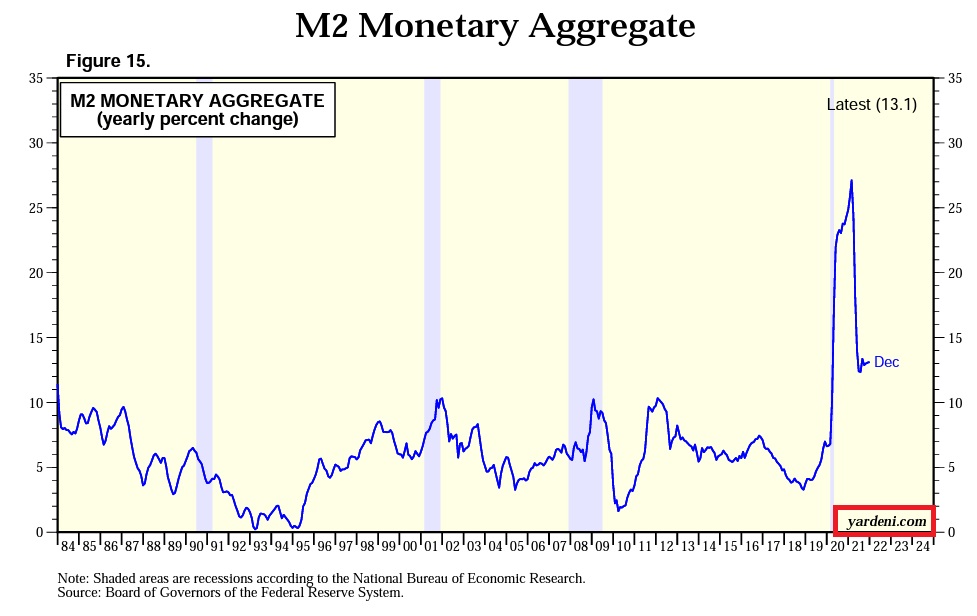

M2 (thanks to the great Ed Yardeni for the charts) is still growing over 10 percent, in the U.S. and most other major economies are or have also experienced rapid money growth. This monetary aggregate is a feeble measure of “money,” which is now almost impossible to define in our age of rapid technological change.

We question, shouldn’t a brokerage account, where you can lever up, say, the gold ETF and still write checks against it, as I used to do, be counted as money? What about crypto?

During the dot.com boom, for example, some restauranteurs in Silicon Valley took stock options as payment from new startups using their dining booths as offices and a dining hall. Is that considered money? It certainly met two of the three criteria: a medium of exchange and a unit of account, at least while it lasted.

When I worked in the Federal government back in the day as a grad student, I attended seminars where some economists advocated including stock mutual funds as part of the money supply measures when the monetary aggregates began to diverge from nominal GDP.

US Monetary Aggregates

Monetary Policy Is A Blackbox

Even Alan Greenspan said as much 25 years ago in his famous Irrational Exuberance speech, which is more true today than it was then.

There is, regrettably, no simple model of the American economy that can effectively explain the levels of output, employment, and inflation. In principle, there may be some unbelievably complex set of equations that does that. But we have not been able to find them, and do not believe anyone else has either.

Consequently, we are led, of necessity, to employ ad hoc partial models and intensive informative analysis to aid in evaluating economic developments and implementing policy. There is no alternative to this, though we continuously seek to enhance our knowledge to match the ever growing complexity of the world economy. — Alan Greenspan, Dec. 1996

Inflation Accelerating

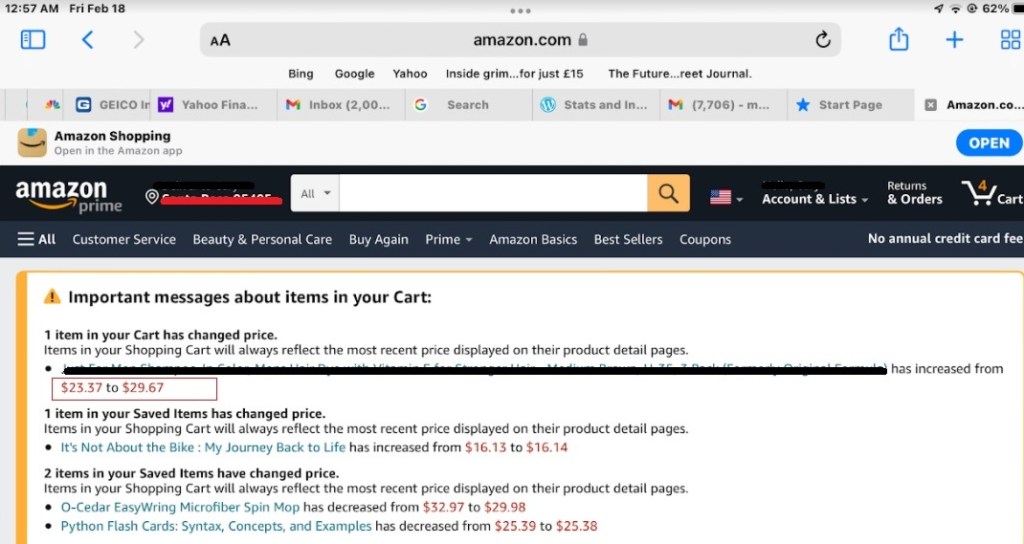

I woke to a ping on my iPad the other night to the following message from Amazon warning some prices in my basket had gone up overnight and gone up big. I am certainly not going to reveal my monthly hygiene product, but you get the point.

The upshot is companies continue to raise prices, not because they are greedy or evil, but because the point-of-sale demand is there, and they can pass on any rise in input costs, and then some. That is why businesses are in business, to make a profit, folks.

Profits, like fire, are amoral. A fire burned down my house in the NorCal 2020 wildfires but also cooks my food and keeps me warm at night.

Understanding Inflation In The Context Of Global Monetary Policy

Monetary policy is a challenging concept to grasp. Witness Greenspan’s quote above.

In my undergraduate American Presidency class, I recall reading about JFK, who would pen cheat notes on his hands before press conferences. Fiscal policy on one hand and monetary policy on the other as not to confuse the two.

I taught undergraduate economics for years, including several money and banking courses, and tried to use simple analogies and heuristics to help my students grasp these very complex issues.

Bathtub Overfloweth

If I had to use one today to explain what is going on with inflation and the supply chains, it would be the following simple picture of a bathtub overflowing:

Assume the water in the tub above is the global liquidity in the world economy. It consists of the base money created by the central banks, endogenous money created by the credit markets (my 18-year daughter just received an offer for an $18k line of credit), and all the other faux wealth created and associated with the ‘everything bubble,” which is extremely difficult to quantify.

The overflow is the inflation now wreaking havoc in the goods & services market. It will cause significant structural and political damage if it continues, such as the floor caving in and flooding the downstairs — ditto for the economy.

If inflationary psychology takes hold in the economy at large, as it has in the supply chain, well “Houston, we have a problem.” It is baffling to us that market analysts maintain, and even the central banks, that inflationary expectations are well anchored in, say, the 5-year breakevens.

Can we really infer an economic signal when the U.S. central bank has bought up, albeit indirectly, around 75 percent all coupon Treasury securities and almost 200 percent of the TIPs issuance since COVID? That price is about as well managed and meaningless, at least to us, as the price of sausage “back in the USSR…where the Ukraine girls really knock me out.”

We can sit here and wish inflation away, and it’s almost laughable that some “so-called” economists do so, but that ain’t going to happen, folks. The major central banks need to take action.

The bathtub as is the global economy are in significant disequilibrium.

What To Do?

The central banks control the faucet with their balance sheets and the temperature with interest rates.

The solution is quite simple, in theory.

Immediately, turn off the spigot (the Fed and ECB are still stunningly pumping away as we write), drain the liquidity to a more acceptable level (quantitative tightening), and increase the temperature to a comfortable level by raising interest rates, where the economy can bathe in a more stable and comfortable equilibrium, if one does exist.

Easier said than done, however.

Asset markets are addicted to the excess liquidity, where even the most worthless rubber duckies have floated to the rim as their excess valuations overfloweth on a monster scale. The market is, however, starting its dangerous speed wobble as the “dogs [rubber ducks] that don’t hunt” are rolling over hard and quite rapidly, as more than 40 percent of all Nasdaq stocks are now down over 50 percent from their highs.

The Fed and other major central banks almost certainly fear the coming asset devaluations, which need to adjust and regress down to their historical valuation water line.

Because the global markets and economies are so hooked on the crack of free money coupled with both the leads and lags of monetary policy and lack of clarity, the use of monetary policy to fine-tune economies is equivalent to threading a needle with boxing gloves. The central bankers are most certainly facing a difficult next few years.

Godspeed, Chairman Powell and Madame Lagarde.

As always, we reserve the right to be wrong.

Stay frosty, folks.