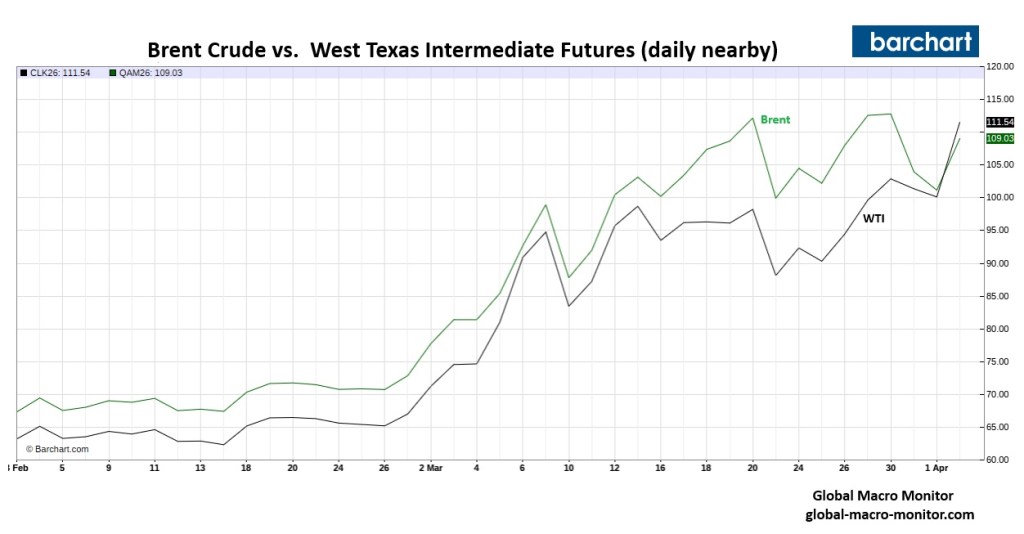

The oil market just delivered one of those “stop what you’re doing” moments: U.S. benchmark WTI trading at a premium to Brent. That’s not just unusual, it’s a signal flare for acute market dislocation.

What Happened (and Why It Matters)

OilPrice.com highlights a rare inversion where WTI surged above Brent, flipping a long-standing global pricing hierarchy. Traditionally, Brent commands a premium given its role as the seaborne global benchmark. When that relationship breaks, something is fundamentally wrong in the plumbing of the oil market.

The driver? Immediate supply scarcity, localized, acute, and geopolitical.

Recent developments—particularly escalating tensions involving Iran and disruptions to the Strait of Hormuz—have choked off a meaningful portion of globally traded crude. Markets are now pricing availability, not just fundamentals.

WTI’s premium is less about U.S. oil being “better” and more about it being accessible. Domestic barrels, sitting in Cushing or flowing through U.S. infrastructure, suddenly look like the cleanest shirt in a very dirty laundry basket.

Microstructure > Macro (For Now)

A key nuance emphasized in the article—and corroborated by broader market commentary—is that this inversion is partly technical:

- WTI futures reflect near-term delivery (May)

- Brent reflects later delivery (June)

In a market gripped by backwardation, front-month barrels command a premium. Traders are paying up for immediacy.

But don’t dismiss this as just calendar spread noise. The magnitude of the move signals something deeper:

The market is pricing physical scarcity today, not theoretical abundance tomorrow.

The Bigger Picture: A Supply Shock, Not a Demand Story

Let’s be clear—this is not 2008-style demand exuberance. This is a supply shock with geopolitical teeth:

- Up to 10–20% of global oil flows are at risk through Hormuz

- Insurance, shipping, and security premiums are exploding

- Russian exports remain impaired

In other words: this is a multi-node disruption across the global energy network.

The result? Oil prices have surged over 50% in a month, with WTI pushing into the $110+ range intraday.

Market Implications for Portfolio Managers

1. Inflation Is Back (and It’s Sticky)

Energy is once again the marginal driver of CPI. This isn’t transitory—it’s structural while geopolitical risk persists.

2. Term Structure Is the Trade

Backwardation is screaming tightness. Front-end crude, refined products, and crack spreads are where the action is.

3. U.S. Energy Assets Gain Strategic Premium

Domestic producers and midstream players are suddenly geopolitical hedges. The U.S. is becoming a relative safe haven in oil supply.

4. Tail Risks Are Fat and Getting Fatter

Options markets are now pricing scenarios north of $150 crude if disruptions persist.

The Global Macro Monitor Take

This isn’t just an oil rally, it’s a regime shift in pricing power.

When WTI trades above Brent, the market is telling you one thing loud and clear:

“I don’t care about benchmarks, I care about barrels I can actually get.”

In that world, liquidity fragments, correlations break, and macro models built on stable relationships start to wobble.

The playbook here isn’t about forecasting demand curves, it’s about mapping geopolitical risk onto physical supply chains.

Welcome to oil markets where geography Trumps economics.