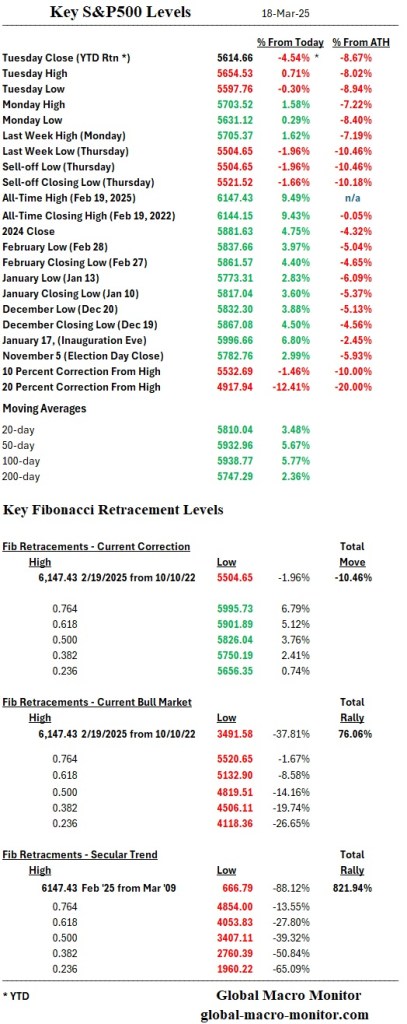

The bounce lacked sufficient momentum to reach the 200-day moving average but managed to hit 5700 before pulling back. We suspect the index will chop between 5500 and 5700 for the next few days or possibly a couple of weeks before testing and breaking the recent low.

Key levels to watch:

5504.65 – Recent low and key support

5647.29 – First Fibonacci retracement of the correction

5703.52 – Yesterday’s high and near-term resistance

For now, our priors are the index will remain in a consolidation phase, with sellers capping upside moves and buyers stepping in near support. A break below 5504.65 could accelerate downside momentum, while a move above 5703.52 would indicate renewed buying strength.

Nice distillation of the macro driving markets by (Pe)ter (Bo)ockvar. The dude gets it.

“There are like megatrends that I think that are reversing to the point where the playbook that worked so well over the last couple of years, throw it away, it’s not going to work. The world is changing, we’re at major inflection points I believe in the markets….” – Peter Boockvar on CNBC

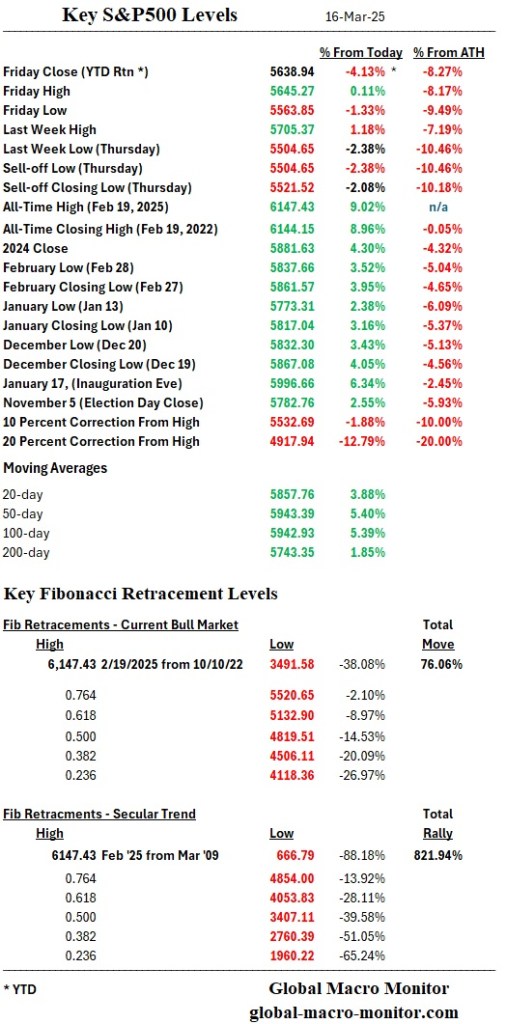

The bounce we were anticipating came Friday, with futures leading the way. After Thursday’s close, buyers stepped into the futures market and commenced to bid the index up. The 200-day is now the upside target (+1.85%), which could come quickly as the fast money shorts will be forced to cover as the market creeps higher. We could be wrong and keeping it close.

Nevertheless, we still believe we are in only the second inning of a nine inning game of pain as the global political and economic order is being demolished by the Trump Administration. Markets seemed to like the old world order, in our opinion, and we have no idea what will replace it. Meanwhile, there will be great uncertainty about the emerging New World Order, and you know how markets love uncertainty.

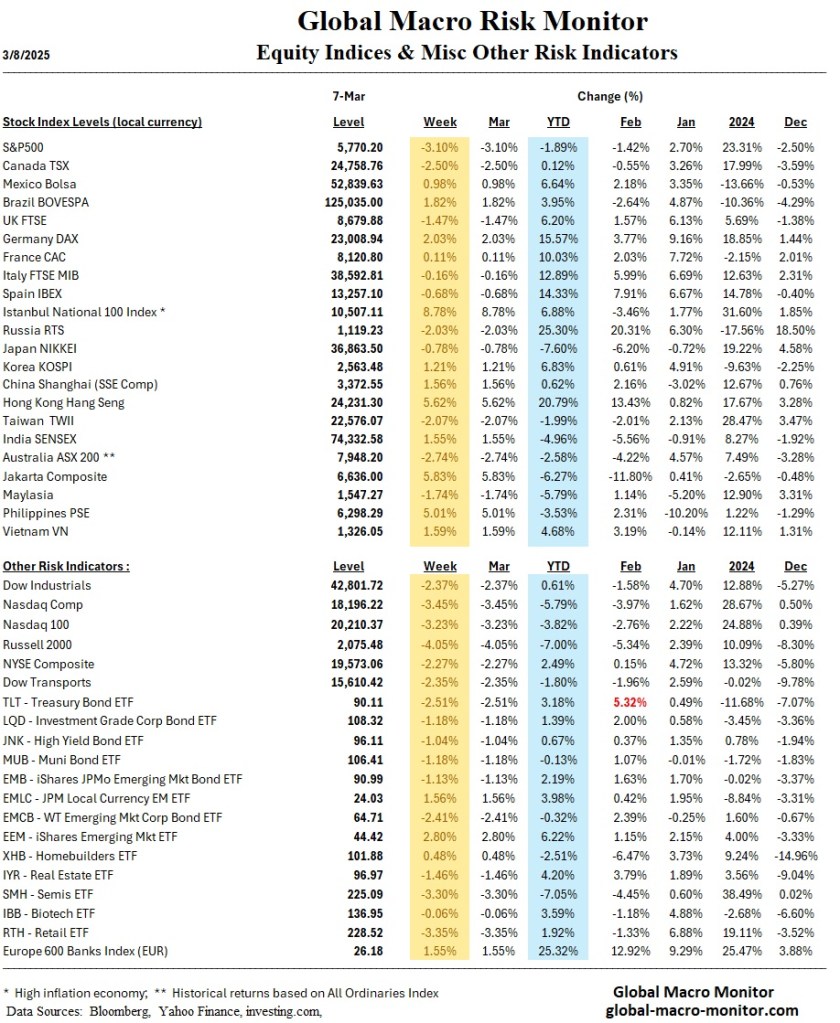

U.S. stock markets saw their fourth consecutive weekly decline, driven by recession fears and trade policy uncertainty.

The Fed will keep rates unchanged, but inflation expectations have risen, raising concerns about stagflation.

Eurozone faces economic headwinds, with ECB policymakers debating the timing of rate cuts amid geopolitical risks.

Japan’s strong wage growth could lead to further interest rate hikes, while China struggles with deflationary pressures.

Bond markets rallied on soft inflation data, but credit spreads widened amid economic uncertainty.

Upcoming economic reports, including U.S. retail sales and industrial production, will shape market sentiment next week.

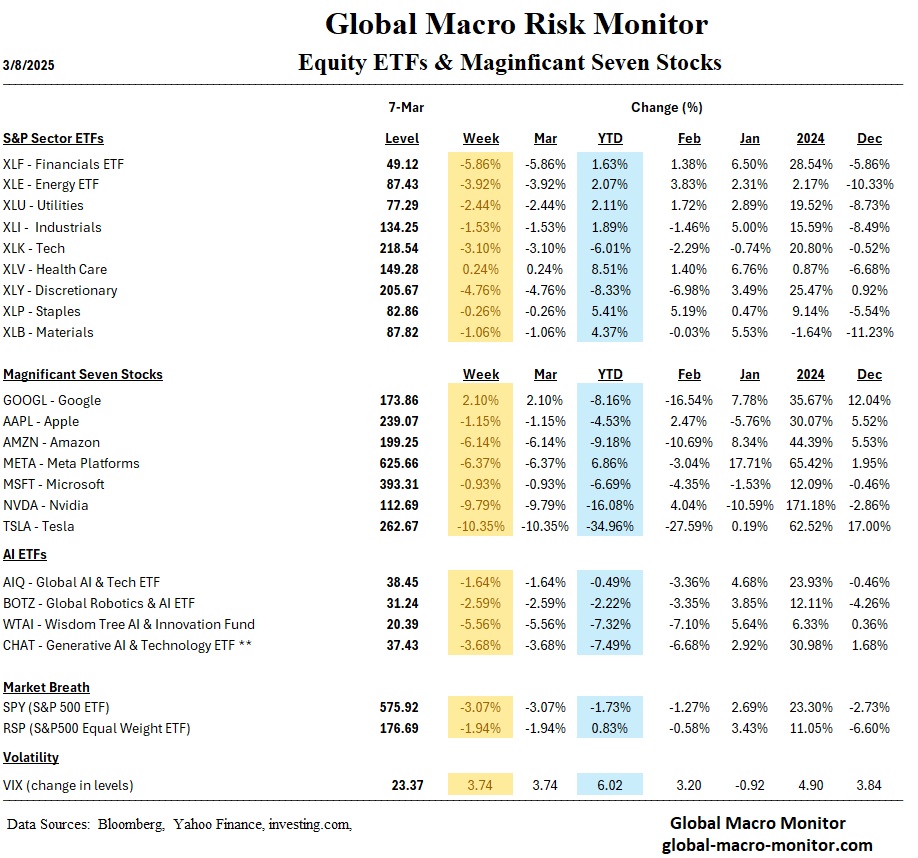

Nvidia’s GTC conference and major corporate earnings will be key market movers in the tech sector.

Financial conditions in the U.S. are tightening, as indicated by the Chicago Fed’s NFCI, reflecting widening credit spreads and declining equity prices.

Markets

The past week saw heightened volatility across global financial markets, driven by recession concerns, trade policy uncertainty, and mixed economic data.

U.S. Stock Market Downturn: Major U.S. stock indices suffered losses, with the S&P 500, Nasdaq, and Dow Jones all recording weekly declines. The sell-off was fueled by persistent trade tensions and economic uncertainty, particularly surrounding the Trump administration’s new tariff announcements.

Bond Market Movements: U.S. Treasuries advanced as lower-than-expected inflation data softened rate hike expectations. Investment-grade bond spreads widened, while municipal bonds underperformed due to seasonal weakness.

European Equities Weakness: The STOXX Europe 600 Index fell by 1.23%, weighed down by concerns over U.S. tariffs impacting European exports. The ECB remains cautious on rate cuts, as inflation concerns persist.

Japan & China Markets: Japan’s stock market posted modest gains, helped by a weaker yen boosting exports, but uncertainty over auto tariffs from the U.S. dampened sentiment. China’s markets rebounded on stimulus hopes, even as inflation data showed deflation risks.

Economics

Economic updates from key regions indicated slowing growth, inflation concerns, and monetary policy uncertainties.

U.S. Inflation & Economic Sentiment: CPI data showed that consumer prices rose 0.2% in February, easing fears of stagflation. However, consumer sentiment plummeted, with inflation expectations climbing to 4.9%, the highest since November 2022.

Eurozone Growth Challenges: The ECB’s future rate-cut path remains uncertain as policymakers worry inflation will stay above target. Germany’s new EUR 500 billion infrastructure plan aims to stimulate economic activity.

Japan’s Wage Growth & Rate Outlook: Japan’s largest wage increase in three decades could push the Bank of Japan (BoJ) towards another rate hike later in the year.

China’s Deflation & Trade Woes: Data suggests prolonged deflation risks, with consumer prices falling 0.7% YoY in February. Trade uncertainty with the U.S. remains a concern for China’s manufacturing sector.

Emerging Market Trends: Latin America’s labor market shows strong momentum, but growth remains sluggish. Hungary’s inflation acceleration may delay central bank rate cuts.

The Week Ahead

Looking ahead, investors and policymakers will focus on key economic data and policy decisions.

U.S. Federal Reserve Meeting (March 18-19): The Fed is expected to hold interest rates steady, but Chair Jerome Powell’s comments will be scrutinized for guidance on future rate cuts.

Retail Sales & Economic Data Releases: Key reports include U.S. retail sales, industrial production, and housing market data. A weak retail sales print could reinforce recession concerns.

Corporate Earnings & Market Events: Nvidia’s annual GTC conference and major earnings reports from Nike, FedEx, and Micron Technology will be in focus.

Geopolitical & Trade Policy Developments: Markets remain on edge over further tariff escalations from the U.S. and updates on ceasefire talks in Ukraine.

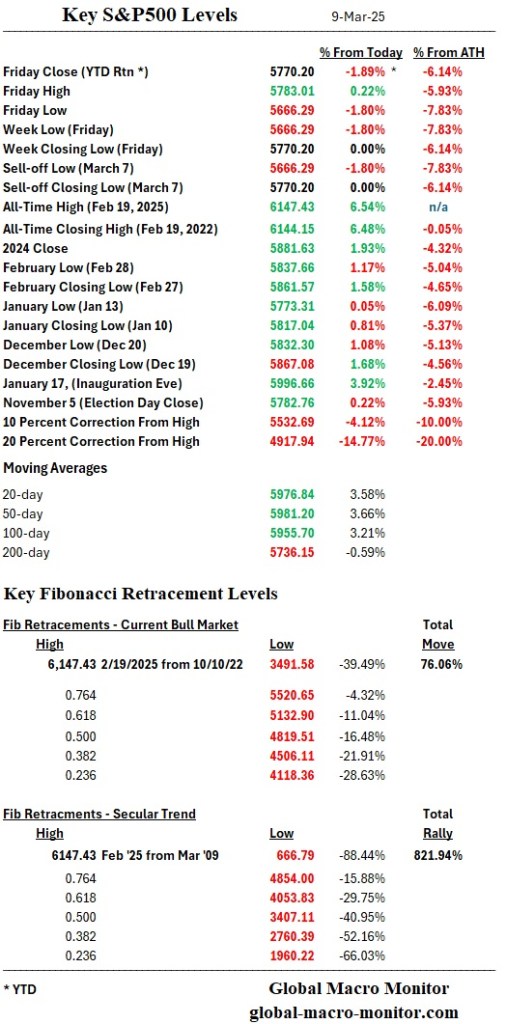

It is hard to believe the S&P 500 reached its all-time high on February 19, only 14 trading days ago. Since then, the index has traded lower in 10 of those 14 sessions, though today, it bounced exactly where expected—at the 10% correction level and the first key Fibonacci support (see highlighted purple boxes in the table below).

Nasdaq Doji Candlestick Also of note is today’s Doji candlestick in the Nasdaq composite. Today’s long lower wick indicates that sellers initially drove prices down, but buyers later stepped in to push the price back up to close near the opening level. This suggests that bearish momentum may be waning, and a potential reversal or consolidation phase could be forthcoming.

However, market liquidity remains weak, and price action has been poor.

That said, stocks are deeply oversold, and if a tradable bounce materializes, the first key resistance is today’s high at 5636.30, followed by Monday’s high at 5705.37. A breakout above these levels could bring the 200-day moving average at 5738.94 into play.

RSI Below 30 The S&Ps Relative Strength Index (RSI) closed at 28.35 today. When an asset is oversold (RSI < 30), it often indicates that the selling pressure has been excessive, and a reversal or bounce could be near. However, oversold conditions don’t guarantee an immediate reversal. The market could continue moving lower in the short term if there are strong fundamental pressures, which, given the policy lunacy in Washington, is certainly the case.

Downside Support Levels On the downside, today’s low at 5528.41 serves as immediate support. Below that, an “air pocket” could accelerate selling toward the thin support line at 5400 and the next Fibonacci support at 5132.90.

A full 20% correction at 4917.94 would officially mark bear market territory, which we believe is much more likely than what the market expects.

Staying cautious, keeping risk controls in place, and looking to sell at higher levels.

Major U.S. indices declined significantly due to tariff uncertainties.

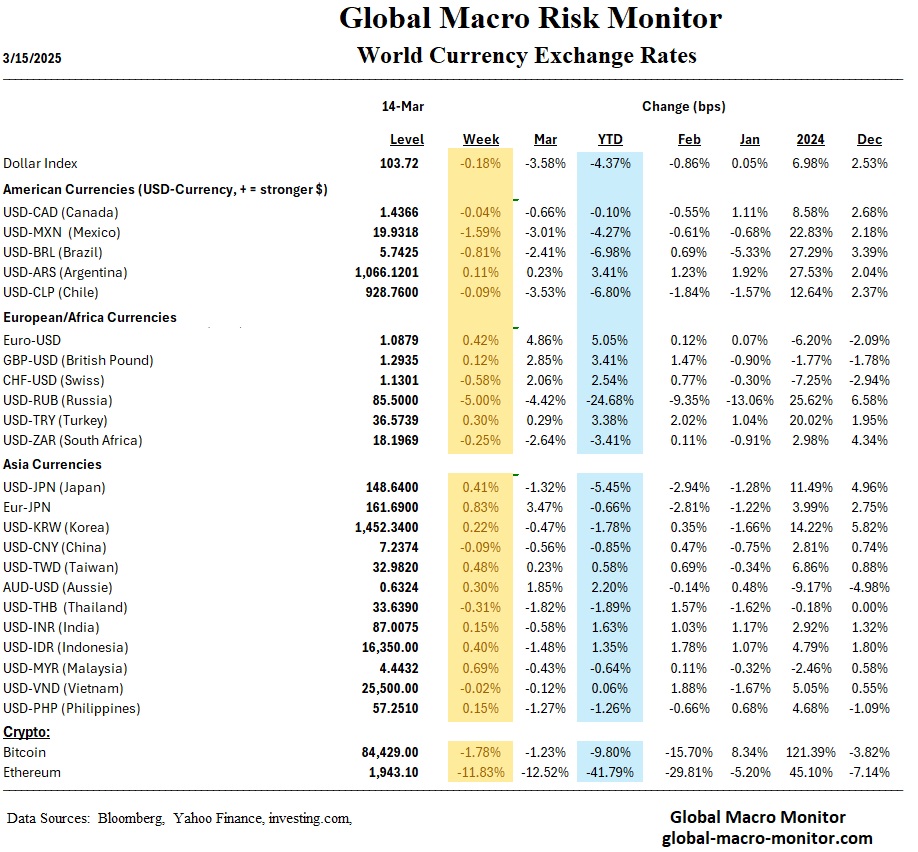

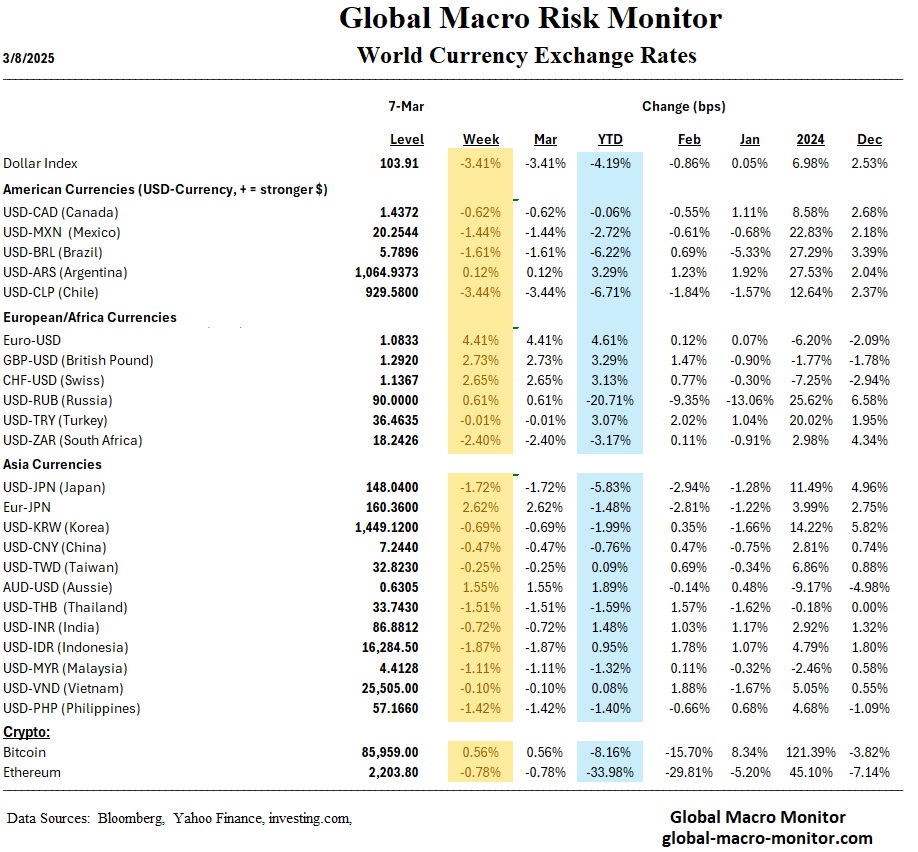

The euro currency spiked after Germany announced a massive fiscal spending package.

Germany’s new budgetary strategy caused historic bond yield increases.

ECB lowered rates amid slowing inflation and substantial uncertainty.

Japan’s bond yields reached the highest levels since 2008.

China’s fiscal stimulus aims to combat deflationary pressures.

Employment and manufacturing indicators in the U.S. signal economic moderation.

Markets: U.S. and Global U.S. markets experienced considerable volatility this past week as Trump’s shifting tariff policies caused uncertainty among investors. The announcement of 25% tariffs on Canadian and Mexican imports and an additional 10% on Chinese goods led major indices, including the S&P 500 and Nasdaq Composite, to suffer their sharpest declines since September. The S&P 500, after penetrating key support, managed to rally into the Friday close.

Global markets echoed this instability, with European stocks ending a 10-week winning streak and Japanese markets showing mixed results amidst yen appreciation and rising bond yields. Chinese markets, conversely, rallied modestly after signals of further fiscal stimulus.

Economics: Domestic and International Domestically, the inconsistency of tariff decisions has started to influence U.S. economic performance negatively, evidenced by sluggish manufacturing growth and increased concerns reported in the Federal Reserve’s Beige Book. Internationally, Trump’s policies prompted significant reactions: Europe’s strategic fiscal expansion, notably Germany’s EUR 500 billion infrastructure and defense spending, marked a historic policy shift resulting in dramatic rises in bond yields and Euro valuation. Japan is facing rate hikes due to inflationary pressures partly linked to trade uncertainties, and China faces ongoing growth headwinds despite new stimulus measures, highlighting broad global economic implications.

The Week Ahead Attention will shift towards upcoming economic indicators, particularly the U.S. employment report, following signs of moderating job growth and rising unemployment. Germany’s fiscal announcement, causing a spike in European bond yields, will remain a focal point, alongside the appreciation of the Euro. Investors will closely monitor these developments as they navigate the ongoing financial market volatility stemming from Trump’s unpredictable trade stance.