Time for the summer holiday, folks.

Happy hunting.

See you in September.

Time for the summer holiday, folks.

Happy hunting.

See you in September.

Stunning.

Imagine how these will be weaponized in the 2020 presidential campaign.

The world is starting to move sideways.

The market talking heads are so clueless.

It’s almost laughable listening to them trying to explain away in isolation how the pieces of the puzzle are starting to converge that will or already have ushered in, what we believe, will be an ugly bear market.

Believing the Fed can rescue anything and everything is so naive and ridiculous. We remain perplexed why JFK didn’t call in the Fed to end the Cuban Missile Crisis, or why President Trump doesn’t call upon Fed Chairman Jay Powell to unleash some QE to bring about peace in the Arab-Israeli conflict.

Global Geopolitical Instability

The rivets are starting to pop both in the U.S. and world.

We won’t mince words here. We believe much of the growing instability is the consequence of the narcissistic and incompetent leader of the free world named Donald J. Trump.

Full Disclosure

Full disclosure, we don’t like Trump as a president nor as a man. But we don’t believe our perspective is steeped in some sort of blind political partisanship but is more the result of a positive analysis of the totality of his policies and character. If the data points were different, we have no doubt our conclusions about Trump would be different.

We are independents or what California’s Secretary of State labels “No Party Preference (NPP).” We have no problem splitting tickets and often do. We generally don’t like voting for incumbents down-ballot.

We are right-of-center on most economic issues but believe the government should provide a strong, efficient, and effective safety net for those less fortunate and not born into the Lucky Sperm Club or who are temporarily down on their luck, which all of us could go there but by the Grace of God. If you are reading this post you are most likely part of the Lucky Sperm Club.

We are also golfers and believe in the handicap system. Those non-scratch economic players, such as people born into poverty with very high hurdles of escaping their plight should be given extra strokes to become competitive and to have skin in the game of life.

We believe in fiscal responsibility and that if the current budget trajectory continues big inflation will eventually come to burn away past liabilities that no way in hell will ever be paid back in hard currency but probably not before the deflationistas have another day in the sun. Can’t you just see this scenario setting up as the street cred of Modern Monetary Theory (MMT) is rising almost as fast as Beyond Meat (BYND) stock?

We are left of center on most social issues but respect others beliefs. Our motto is: no pushy our agenda onto others; especially our California values onto the conservative states unless constitutional issues are at stake.

The following is how we voted in the presidential elections since 2000 with a short justification. We will strategically vote the Republican ticket in the 2020 California primary but for Governor William Weld if he is on the ballot. Not so in the general in November, however.

2000 – George W. Bush: Tired of the lies from both Clintons and their lack of political principles. Though we thought Clinton did fairly well on economics, especially not spending the fiscal surpluses late in his administration as Larry Summers surely knew they were only a windfall and largely the result of the stock market bubble. Totally disagreed with the Clinton/Gore expansion of NATO, which botched efforts to bring Russia into the West, which the world now suffers the consequences.

2004 – John Kerry: Invasion of Iraq and the deception that justified it. Unforgivable. Bush won the election because he won Ohio, period. If Kerry had come out against gay marriage, which was the wedge issue driving that election along with scaring the American people about terrorism, Bush loses the election. Kerry came under intense pressure to denounce gay marriage and support the Ohio initiative opposing it but wouldn’t. That was a true profile in courage, in our book. Like trading, timing is everything in politics. Sadly, the country just wasn’t ready for same-sex marriage in 2004.

2008 – Barack Obama: Loved the Maverick, not so much Sarah Palin. Would have moved out of country knowing she was a heartbeat away from the Oval. Obama’s hope and unity rhetoric was moving. Also, was certain a McCain/Palin ticket, coupled with the Congressional Republican ideologues could not restore the crashing global economy. Was very worried of a complete financial and economic collapse and justifiably so.

2012 – Mitt Romney: Didn’t like Obama’s “fat cat” divisive rhetoric. Was impressed that the Obama administration pulled the global economy out its death spiral, however. Totally underestimated the markets’ confidence in the dollar after massive expansion of deficits and central bank balance sheets. Wasn’t satisfied with the pace of structural economic reform and not putting Wall Street in the dock after the Great Financial Crisis (GFC).

2016 – None of the above: Slim Pickins for POTUS in 2016. Could there have been two worse choices? Would have never thunk of voting for Hillary but if my vote really counted on the margin — it doesn’t because we live in perirenal blue California — would have held my nose and voted for her.

Global Trade And The Decline Of Bretton Woods

Markets still don’t get it. Trump is an economic nationalist, not a free-trader, much less even understands the basic tenets of trade. Most of the 2020 Democratic candidates are not much better but may change their tune once they see the damage the trade war does to most Americans and the global economy.

The following tweets speak for themselves.

President Donald Trump’s trade war with China is increasing the odds that America will be thrown into a recession, according to investment bank Goldman Sachs. – NBC News, August 12t

The Great Unraveling

Hong Kong

What exactly did Trump say to Xi at the G20 in Osaka last month that led to this FT headline? What signal or mixed signals did POTUS send to the Chinese government about the U.S. reaction if China’s PLA starts cracking heads in Hong Kong? The fact that we don’t even know is a problem in and of itself.

The words of the President, who speaks for the United States government and the rest of the free world, have huge consequences and any ambiguity can invite aggression or destabilize global or regional stability.

Go no further than Gulf War I.

Gulf War Documents: Meeting between Saddam Hussein and US Ambassador to Iraq April Glaspie

July 25, 1990. Eight days before the August 2, 1990 Iraqi Invasion of Kuwait

July 25, 1990 – Presidential Palace – Baghdad

U.S. Ambassador Glaspie – I have direct instructions from President Bush to improve our relations with Iraq. We have considerable sympathy for your quest for higher oil prices, the immediate cause of your confrontation with Kuwait. (pause) As you know, I lived here for years and admire your extraordinary efforts to rebuild your country. We know you need funds. We understand that, and our opinion is that you should have the opportunity to rebuild your country. (pause) We can see that you have deployed massive numbers of troops in the south. Normally that would be none of our business, but when this happens in the context of your threat s against Kuwait, then it would be reasonable for us to be concerned. For this reason, I have received an instruction to ask you, in the spirit of friendship – not confrontation – regarding your intentions: Why are your troops massed so very close to Kuwait’s borders?

U.S. Ambassador Glaspie – We have no opinion on your Arab – Arab conflicts, such as your dispute with Kuwait. Secretary (of State James) Baker has directed me to emphasize the instruction, first given to Iraq in the 1960’s, that the Kuwait issue is not associated with America. (Saddam smiles)

On August 2, 1990, Saddam massed troops to invade and occupy Kuwait. — Global Research

North Korea

While Trump exchanges “beautiful letters” with Kim Young-un, North Korea gets stronger and more dangerous by the day,

Trump, meanwhile, has praised Kim during for sending him a “very beautiful letter” last week despite the uptick in tests over the past three weeks — but he shouldn’t be celebrating. The increased pace of tests and revelation of new weapons means his chances of striking a nuclear deal with Pyongyang are slipping, all while North Korea builds weapons that threaten South Korea and Japan — both close US allies that host thousands of US troops.

Which means no matter what Trump says, North Korea has become much more dangerous — not less — since he took office.

“This is an intentional reminder that if diplomacy fails, North Korea will only be stronger and more capable today than it was four years ago,” Lindsey Ford, a former Asia security specialist at the Defense Department, told me. – VOX, August 12th

The following is nothing short of buffoonery.

We were warning of this while our friends were calling for a POTUS Nobel Peace Prize.

How embarrassing for any American with a sense of history and pride.

NATO

We believe the words that have and will be the most destabilizing to the world is what President Trump said about NATO and Montenegro last summer. We wrote about it the day after in our post, The Day Strategic Ambiguity Died,

The hits just keep on coming.

There is a new sheriff in town, the old order is crumbling, and we are afraid the world is going to become much more unstable in the next few years. Assets markets are incapable of discounting or pricing it in.

President Trump Throws Montenegro Under The Bus

In an interview with Fox’s Tucker Carlson last night, President Trump seemed to question the raison d’être of NATO and foreign alliances in general.

Tucker: So membership in NATO obligates the members to defend any member that is attacked. So let’s say Montenegro, who joined last year, is attacked, why should my son go to Montenegro to defend it from attack?

President Trump: I understand what you are saying. I have asked the same question. You know Montenegro is a tiny country with very strong people… They may get aggressive, and congratulations you are in World War III…But that is the way it was set up, don’t forget I just got here.

There are errors and misrepresentations in the above, such as NATO’s Article 5, which has only been invoked once in the aftermath of 9/11, and does not apply when the NATO member is the aggressor.

…

Xi’s One China Policy

What worries us about the Tucker Carlson interview is a potentially destabilizing effect on geopolitics, especially with China.

How do you think Xi Jinping, Trump’s new BFF, who is becoming increasingly aggressive about his “one China” policy, interpreted the interview?

Maybe something like:

“Why should my son go to

MontenegroTaiwan to defend it from attack?”Wars begin with misperception and miscalculation. — GMM, July 18, 2018

Upshot

We are certainly are not blaming Trump for all that ills the world. But he is the leader of the free world and has made things worse, not better, in our opinion analysis.

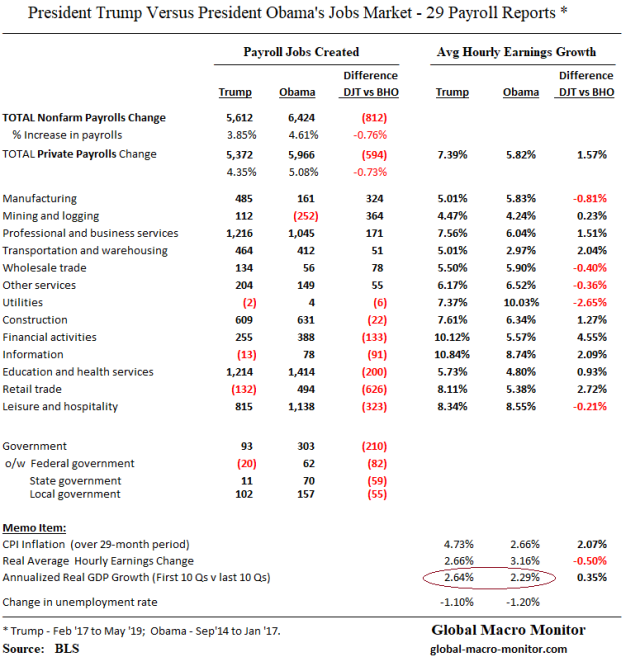

His economy in the first thirty months is only marginally better in a very narrow sense than the economy in the 30 months before he took office.

Economy

After increasing the cumulative deficit by over $2 trillion, almost $1 trillion more than the last 29 months of the Obama administration, the average compounded GDP growth rate is only 35 bps higher. That is an expensive 35 bps of growth, folks.

Moreover, inflation is higher and nonfarm payroll job creation is lagging by almost one million jobs.

Tight Financial Conditions

Trump likes to blame the Fed that “his” economy is not doing better. This is complete nonsense. Financial conditions have been much easier for President Trump according to most measures even though the Fed has been raising interest rates.

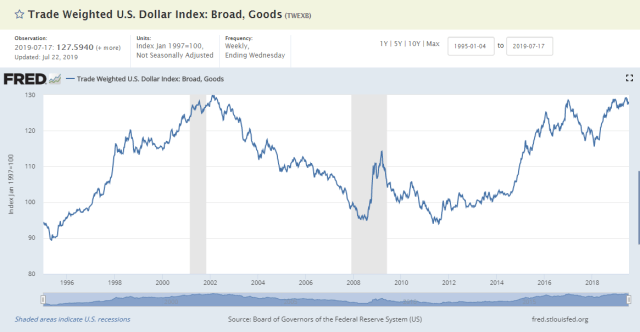

Dollar

Most important is that the trade-weighted dollar index has stabilized under Trump, albeit at a higher price, after strengthing more than 20 percent in the last two years of the prior administration. That was a huge economic headwind in President Obama’s second term and really hit the manufacturing sector hard.

MAGA

If you believe Trump has Made America Great Again, you have been played like a fiddle, folks. The gaslighting has worked.

President Trump likes to play golf, tweet, and watch cable news. No judgment, we do too, but who is minding the store at the USG? He has fired almost everyone and anyone with just a modicum of competence, believing he knows better than anybody , even more than the Generals, for example.

That is what is most scary and echos what President Bush #43 said after listening to the Trump inaugural speech,

‘That was some weird shit,’ George W. Bush reportedly said with characteristic Texas bluntness” – Business Insider

Buckle up.

We sense it is about to get very ugly. We hope we are wrong.

We see a fading confidence in the value of free markets and international trade, forgetting that conflict, instability and poverty follow in the wake of protectionism. We’ve seen the return of isolationist sentiments, forgetting that American security is directly threatened by the chaos and despair of distant places. – President George W. Bush

There is a big difference between a bond with a negative yield to maturity than a bond with a negative coupon rate. Many in the market conflate the two.

We are searching for bonds that pay a negative coupon rate. Rare, but some do exist.

Here is a good clarification.

Because of the complexity of having a negative coupon, it is common on negative-yielding issues to sell the bonds at a cash price higher than par. This means the issuer pays back less than the amount borrowed, removing the need to figure out how to organise reverse coupon payments.

This is one of the reasons negative yields on bond issues remain a rarity and off limits to many investors.

In the corporate bond world, the likes of Deutsche Bahn have issued negative-yielding bonds in the past, and this month Merck sold three tranches of debt, the shortest of which held a negative yield. – Reuters

But they do exist

France issued its first-ever 10-year bond at a negative borrowing rate on Thursday, meaning investors pay, rather than receive, interest for the privilege of owning French sovereign debt, said the state debt management agency, AFT.

AFT said in a statement that it issued 9.996 billion euros ($11.3 billion) in long-term bonds, with just under half — or 4.972 billion euros — in the form of 10-year bonds at a rate of -0.13 percent. – France 24

This is an interesting one.

Copenhagen | In the world’s biggest covered-bond market, a Danish bank says it’s now ready to sell 10-year mortgage-backed notes at a negative coupon for the first time.

It’s the latest record to be set in a world that’s being dragged down by ever lower interest rates. In Denmark, where Jyske Bank will offer 10-year mortgage bonds at a fixed rate of minus 0.5 per cent, average Danes will borrow at rates far lower than those at which the US government can sell its debt. – Financial Review

Hat Tip: Gregory Mannarino @GregMannarino

The bid-to-cover ratio, indicative of the number of investors who put in offers to buy the debt and a gauge of demand, stood at 2.19. That is down from the 2.4 recorded in the last sale last month and marks the second-lowest level since March 2009. – FT, August 8th

We were not surprised at yesterday’s weak 10-year auction though today’s $19 billion of 30-years went off fairly decent.

In our Tuesday post, we raised the question,

…we are watching the Treasury auctions closely and suspect they could get sloppy and ugly down at these yields.

With repressed yields a sort of “rent control” problem arises, where there is a shortage of funds at the given fake or below market yield. Just as the case with a shortage of housing when rents are held below their market rates.

This is just a thought and first cut and needs to be further fleshed out. — GMM, August 6th

Any market observer understands that the marginal price setter doesn’t necessarily reflect the level where large quantities can be liquidated or sold.

Go no further than the LTCM crisis where that hedge fund full of genius Nobel laureates set the level of credit spreads across many markets with help from a boatload of leverage. When it tried to liquidate some of those positions, there were no buyers.

Can the Treasury issue several trillion of new debt over the next few years at these “fake yields,” which have been manipulated lower by central banks and set on the margin by the duration jockeys looking for short-term capital gains with no interest in holding the bonds for the carry? We seriously doubt it and that conflict is indicative in the weak bond auctions.

Upshot

We expect Treasury auctions to get sloppier with the risk of some even failing. That will send a real wake-up call to markets and the policymakers. Zero price discovery in markets has ugly consequences, some of which, take a long time to be realized.

Yes, Virginia, there is a debt overhang. And yes, Vice President Cheney, deficits will matter.

I loved this commercial when everyone was a stock market genius back in the late 1990’s, that time was different, and eyeballs trumped earnings.

We find it interesting that many accuse us of being China apologists because we have concluded from our analysis long ago that President Trump is taking the wrong approach in dealing with the Middle Kingdom. No argument here we have issues with China that need to be addressed. China has outgrown its developing country status and its special treatment within the WTO should be removed. We also are realistic that trying to get China to change its economic model because the U.S. demands it is a nonstarter.

Moreover, going it alone, leaving the TPP, negotiating out of ignorance, impulse, and through tweets, and using tariffs so cavalierly have been, are, and will be a disaster. We believe the deterioration in global trade is the major factor that is tanking the global economy. Go no further than Germany to confirm this.

Cuban Missile Crisis

Compare the current U.S.-China negotiations with how President Kennedy ended the Cuban Missile Crisis. There were many different paths JFK could have taken. Some of his hawkish advisers wanted to bomb Cuba immediately, some wanted regime change in Cuba, as many in Trump’s inner circle want an economic regime change in China.

Nobody disagreed the Soviet missiles in Cuba had to be removed.

President Kennedy had to weigh different advice, including starting a nuclear exchange and, you know, things like the end of the world issues. He knew what was doable and what was not.

JFK had a fluid and strategic plan and executed it. A real Art of the Deal.

He was cool, calm, and collected. Grace under pressure.

Furthermore, President Kennedy didn’t have the psychological need to be the apparent winner in the conflict. He gave the Soviets an out by pulling missiles from Greece and Turkey, which Kruschev could sell to the Moscow hardliners as an American concession. The President took a lot of heat from Congressional hawks for removing the missiles.

Oscar Shindler Jumping Ship

Today, we are finally getting a sense that many of what we call Trump’s Oscar Shindler supporters, those who don’t like him but profit from his tax cuts and economic policies, are starting to wake up to the fact that Trump is an economic nationalist, bad for the country, and is FUBARing the global economy.

Stay tuned.

P.S. Just heard a Freudian slip by a talking head on Bubblevision, “President Chump said…” It begins.

One year to this very day l flew to the east coast to check out colleges with my then 15-year old. Check Penn off the list.

The following is from an economics major from the University of Pennsylvania.

By the way, foreign money has been pouring into the U.S., not so much now, in large part due to the U.S. trade deficit. It is clear POTUS is clueless not only about monetary policy but also about balance of payments.

God help the United States of America.

The most difficult subjects can be explained to the most slow-witted man if he has not formed any idea of them already; but the simplest thing cannot be made clear to the most intelligent man if he is firmly persuaded that he knows already, without a shadow of a doubt, what is laid before him. – Leo Tolstoy

A question has been nagging us for some time. If the current sovereign yields are repressed and fake, many of which are negative, can the borrowers issue any significant amount of new debt at these current yields? Especially to long-term holders?

We are just thinking out loud here but our priors are that of the Big Three — U.S., Germany, and Japan — which have relatively transparent markets as opposed to China, the U.S. is the only government that needs to issue a significant supply of debt and bonds into the market.

Germany

Germany runs a perennial budget surplus and is actually reducing the stock of bunds in circulation with the ECB now contemplating lifting its self-imposed cap of 33 percent of holdings on a single issuer to 50 percent in the event of a new round of QE. Witness the negative 50 bps yield on the 10-year bund. Zero new supply and anticipated central bank demand. See our Bund Dearth post here.

Japan

Japan runs a budget deficit of 3-4 percent of GDP but is a net saver and the BoJ owns almost half of the Japanese Government Bonds (JGBS). We are less familiar with the JGBs x/ our painful memories of shorting them in the 1990s. Need to do further research.

Fake Yields

The current yields do not reflect fundamentals, in our opinion. We suspect the Fed and other foreign central banks now own about 40-50 percent of all marketable Treasuries outstanding with maturities of 10-years or longer and much of the rest of current holders are duration jockeys, such as stock short-sellers to timid to be exposed to the painful and nutcracking equity short squeezes, such as today. We seriously doubt these jockeys partake in the bond auctions.

Auctions

So we are watching the Treasury auctions closely and suspect they could get sloppy and ugly down at these yields.

But there’s general agreement among analysts that the plateau in issuance can last only so long. The bipartisan deal to suspend the debt limit for two years also paves the way for a $324 billion increase in government spending over the period above existing budget caps. That’s emboldening most dealers to pencil in increases in debt sales by fiscal 2021, which starts in October 2020.

“The deficit is rising and the impetus toward higher spending is very strong,” said Stephen Stanley, chief economist at Amherst Pierpont Securities. “By the second half of next year Treasury will have to raise coupon sizes again.” – Bloomberg

Rent Control Problem

With repressed yields a sort of “rent control” problem arises, where there is a shortage of funds at the given fake or below market yield. Just as the case with a shortage of housing when rents are held below their market rates.

This is just a thought and first cut and needs to be further fleshed out.

Poor Bond Auctions

If the price of Treasury’s borrowings is repressed, the excess demand will be 1) cleared by rising rates: 2) supplied by the central bank either directly (not legal in U.S.) or indirectly through some sort of QE, and/or 3) sucked out of other markets, such as equities or corporate bonds, in the the form of haven flows, for example, which means lower prices in those markets.

If foreigners make up the difference, up goes the dollar. Not many good choices, no?

Meet your new crowding out effect, folks.

Are our instincts on to something?

Investors submitted bids for 2.39 times the $38 billion of three-year notes offered by the Treasury Department on Tuesday, the smallest so-called bid-to-cover ratio for that maturity in a decade. This is no anomaly. In May, the bid-to-cover ratio at a 10-year auction was also the lowest in a decade. These are far from failures, and plenty of other factors besides creditworthiness go into investors’ decisions about whether to participate in a bond auction. At the top of the list is monetary policy. But that’s the thing — the Federal Reserve has turned dovish, suggesting an interest-rate cut could come as soon as this month. And while U.S. yields are low by historical measures, they are still higher than investors can get anywhere in the sovereign bond market in developed economies. Even so, foreign holders have cut their holdings to about 40% of the marketable U.S. debt outstanding, from more than 50% before the financial crisis. It’s hard not to come to the conclusion that demand for U.S. bonds isn’t limitless, which is a scary thought with the government on track to borrow $1 trillion to finance a budget deficit by the same amount. Expect to hear more about U.S. borrowing in coming months. Strategists expect the Treasury to exhaust its borrowing authority in late September or early October. – Bloomberg

Stay tuned, folks, this could be THE Black Swan. A low probability, high impact end of the world event on nobody’s radar.