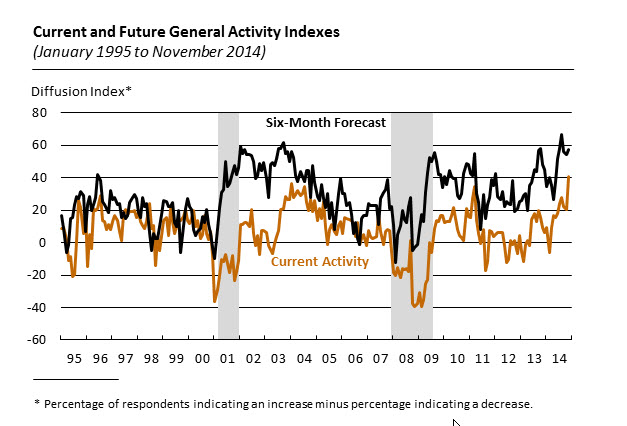

Markit reported its flash PMI for the U.S. service sector this morning, coming in at 56.3 and softer than the expectation of 57.3,

The seasonally adjusted Markit Flash U.S. Services PMI™ Business Activity Index – which is based on approximately 85% of usual monthly replies – registered 56.3 in November, down from 57.1 in the previous month and the lowest reading since April. Moreover, the index has now pointed to softer growth of business activity in each of the past five months, to signal a sustained loss of momentum since the post – crisis peak seen in June…

Commenting on the flash PMI data, Chris Williamson, chief economist at Markit said:

“A fifth-consecutive monthly slowing in growth in the service sector adds to signs that the economic upturn has lost considerable momentum, though it’s important to note that the pace of expansion remains robust by historical standards“

After the manufacturing PMI showed factory output growth slowing in November to the lowest since January, the weaker pace of service sector expansion puts the economy on course to grow at a 2.5% annualised rate at best in the fourth quarter.

With extreme weather hitting parts of the country, growth could slow even further.“However, growth has merely eased from very strong rates earlier in the year. Importantly, even the slower rate of growth signalled by the PMI surveys remains sufficiently strong to generate robust numbers of new jobs. Firms took on staff at

a rate consistent with another increase in payroll numbers of roughly 200,000 in November.“The worry is that any hiring intentions could rapidly deteriorate if firms’ order book inflows fail to pick up again soon.”

{kind=link}