There was some rare good news out of Ukraine today when a vessel loaded with 26,000 tons of corn left the port of Odesa — the first legal shipment of grain since Russia’s invasion began in late February.

It’s a small step but potentially significant for some of the world’s poorest countries as they wrestle with soaring food prices caused in part by uncertainty over supplies of millions of tons of Ukrainian grain blocked by Russia’s assault. – Bloomberg

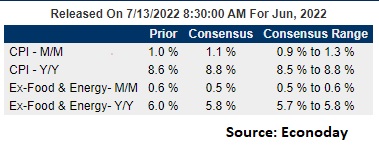

The BLS reports CPI inflation tomorrow with the expectations of the print in the above table.

We are taking the under on the overall consensus expectation of 1.1 percent and the over on the core of 0.5 percent. All based on anecdotal evidence as we see gas and avocado prices plummeting over the past few weeks and rents skyrocketing.

Housing

Nevertheless, the BLS has really painted itself in a corner with how they measure housing inflation.

We have been beating this dead horse for years, and now it has risen from the dead and will bite the BLS and the inflation figures in the arse. For the first time since its inception, the new measure of housing (OER – Owners Equivalent Rent) will be tested in a high inflation environment.

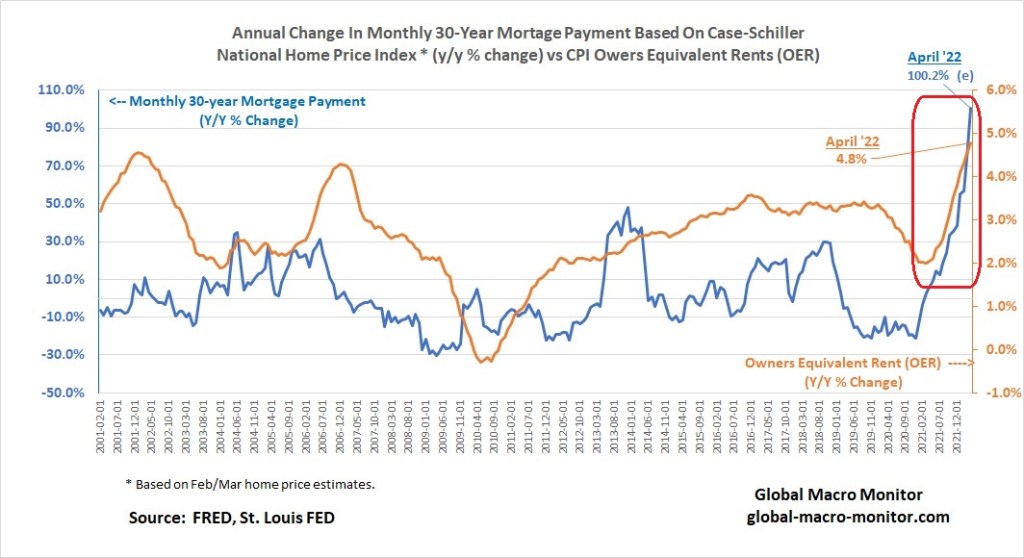

How odd is it that housing prices are softening, but a fixed-rate mortgage is up almost 100 percent in the last twelve months? Moreover, what if homeowners get the Airbnb bug and believe they can rent their homes at the Airbnb rate? That’s trouble with a capital T for the inflation figures, folks, as OER is 25 percent of the CPI basket.

The Los Angeles Times printed a good piece yesterday, which sounded like the Global Macro Monitor.

Money Quotes:

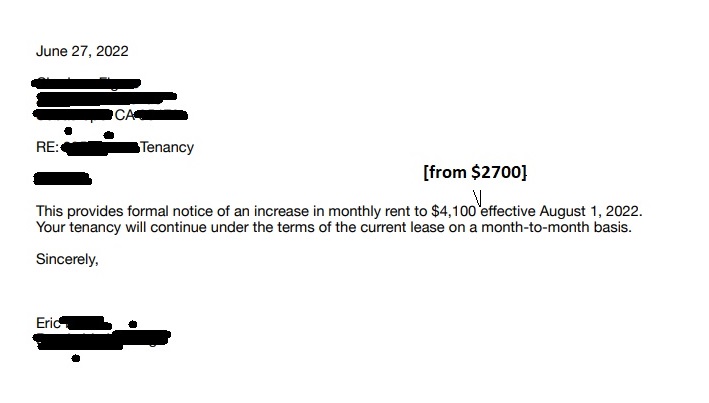

Annual rental costs for new tenants jumped from 4.3% in July 2021 to 11.1% in March 2022. For existing tenants, inflation was lower and grew at a slower pace over that period, climbing from 1.5% to 2.7%. For residents of owner-occupied units, the trend was similar. (BLS is expected to release inflation data for June on Wednesday.)

With the spread between the new-renter and continuing-tenant rates at an all-time high, according to BLS data, that bias is even more pronounced than usual. That gives new ammunition to critics who have argued the data published by the BLS fail to reflect the severity of housing inflation, especially in states such as California, where the cost of housing is higher.

Beyond masking the extent of inflation faced by new tenants, Sohn said, the agency also distorts the market’s reality with the way it calculates the cost of housing ownership. Almost two-thirds of Americans live in homes they own.

Since 1983, BLS has approximated the rental value of owner-occupied homes by measuring the rent paid by tenants in the same vicinity. This is then translated into a rent equivalent.

“To me, the owner-occupied rent is somewhat a wild guess in the official data,” Sohn said. “If I were to rent my own house to myself right now when the price rise is really high, I would be paying much more than what an apartment rent would charge but the BLS wouldn’t reflect that necessarily.

”This data is evidence that rents are going up very fast, faster than they have been, for new tenants after a long period of slower price growth,” said David Wessel, director of the Brookings Institution’s Hutchins Center on Fiscal and Monetary Policy.

Past trends suggest it’s only a matter of time before the higher inflation rate spills over into renewals as well, he said. – LA Times

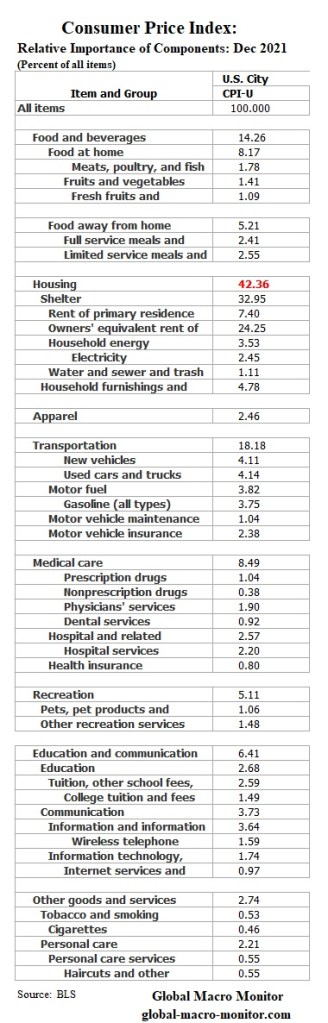

The Heavy Weight Of Housing In The CPI

Housing is 42 percent of the CPI basket and overshadows all else. Nothing comes close in terms of its importance. See our early May post, CPI Inflation’s Big Problem: Housing.

This will be a big headache breaking the feedback loop for the policymakers. We wouldn’t be surprised if they start tinkering with the basket again.

The Fed made their inflationary bed, and now they have to sleep in it. And we all suffer…well most of us.

Watch Jay Pow stumble over this question of why they are buying $40 billion a month in mortgages when there is a dearth of supply in housing.

A well regulated Militia, being necessary to the security of a free State, the right of the people to keep and bear Arms, shall not be infringed. – Second Amendment of the U.S. Constitution

Looks like he will soon be back in action with a vengeance:

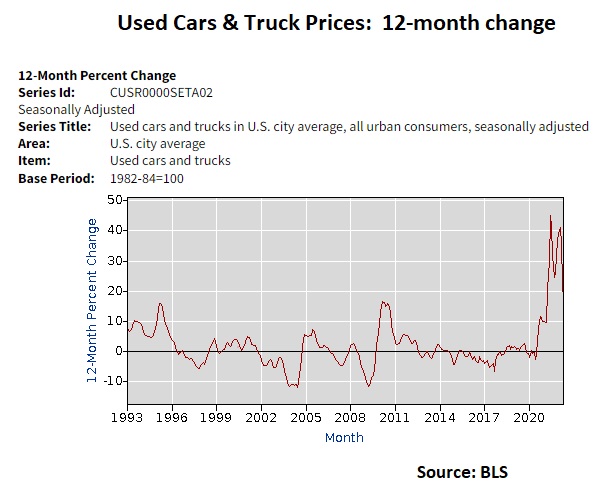

A record share of new car shoppers are being saddled with monthly payments topping $1,000, according to June data from Edmunds. That’s higher than the average cost of rent in 24 US metro areas on the Zumper National Rent Report. Meanwhile, the average monthly car payment reached $712 in May, according to Cox Automotive. That’s higher than rent for one-bedroom apartments in cities like Wichita, Kansas, and Akron, Ohio. – Bloomberg

What could possibly go wrong? FOMO in the used car market….Geez!

It appears the used car bubble is going to burst. Bummer, my daughter just bought a used VW yesterday. No worries, she is not a flipper and got a very good price.

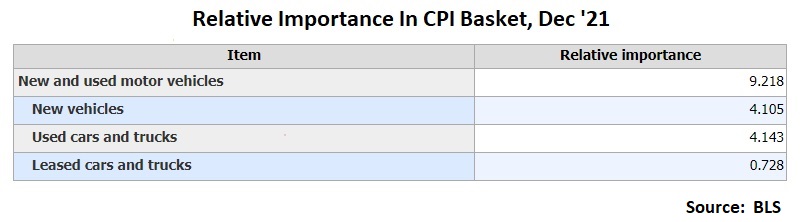

The coming deflation – yes, lower prices and not “disinflation“, which in the words of Wolf Blitzer, is “happening now” – in used car prices will dampen CPI inflation on the margin, even though they are only about 4 percent of the CPI basket.

The butterfly effect is the concept that small causes can have large effects. Initially, it was used with weather prediction but later the term became a metaphor used in and out of science.

In chaos theory, the butterfly effect is the sensitive dependence on initial conditions in which a small change in one state of a deterministic nonlinear system can result in large differences in a later state. The name, coined by Edward Lorenz for the effect which had been known long before, is derived from the metaphorical example of the details of a tornado (exact time of formation, exact path taken) being influenced by minor perturbations such as the flapping of the wings of a distant butterfly several weeks earlier. Lorenz discovered the effect when he observed that runs of his weather model with initial condition data that was rounded in a seemingly inconsequential manner would fail to reproduce the results of runs with the unrounded initial condition data. A very small change in initial conditions had created a significantly different outcome. — Wikipedia

On this day in history, June 28, 1914, the driver for Archduke Franz Ferdinand, nephew of Emperor Franz Josef and heir to the Austro-Hungarian Empire, made a wrong turn onto Franzjosefstrasse in Sarajevo.

Just hours earlier, Franz Ferdinand narrowly escaped assassination as a bomb bounced off his car as he and his wife, Sophie, traveled from the local train station to the city’s civic city. Rather than making the wrong turn onto Franz Josef Street, the car was supposed to travel on the river expressway allowing for a higher speed ensuring the Archduke’s safety.

Yet, somehow, the driver made a fatal mistake and tuned onto Franz Josef Street.

The 19-year-old anarchist and Serbian nationalist, Gavrilo Princip, who was part of a small group who had traveled to Sarajevo to kill the Archduke, and a cohort of the earlier bomb thrower, was on his way home thinking the plot had failed. He stopped for a sandwich on Franz Josef Street.

Seeing the driver of the Archduke’s car trying to back up onto the river expressway, Princi seized the opportunity and fired into the car, shooting Franz Ferdinand and Sophie at point-blank range, killing both.

That small wrong turn, aminor perturbation to the initial conditions, or deviation from the original plan, set off the chain events that led to World War I.

Stumbling Into The Great War Fearing Russian support of Serbia, Franz Josef would not retaliate by invading Serbia unless he was assured he had the backing of Germany. It is uncertain as to whether the Kaiser gave Franz Josef Germany’s unequivocal support. Russia, fearing Germany would intervene, mobilized its troops forcing Germany’s hand.

The great European powers thus stumbled into a war they didn’t want through complicated entanglements and alliances, and miscalculation. Russia backing Serbia; France aligned with Russia, Germany backing the Austro-Hungarian Empire; and Britian, who really didn’t have a dog in the fight except her economic interests, aligned with France and Russia.

Later the U.S. would enter the war due to Germany’s unrestricted submarine warfare threatening American merchant ships and the Kaiser floating the idea of an alliance with Mexico in the famous Zimmerman Telegram, which was intercepted by the British.

Of course, some will argue that Great War in Europe was inevitable

The great Prussian statesman Otto von Bismarck, the man most responsible for the unification of Germany in 1871, was quoted as saying at the end of his life that “One day the great European War will come out of some damned foolish thing in the Balkans.” It went as he predicted. – History.com

Nevertheless, maybe the course of history would have been different if not for that wrong turn on June 28, 1914, which created the humongous butterfly effect, which we still experience the consequences this very day.

The botched Treaty of Versailles sowed the seeds the for World II. The War contributed to the Russian revolution and Cold War. The redrawing of borders in the Middle East after the War created the conditions for the instability and breakdown to tribalism the region experiences today.

A map marked with crude chinagraph-pencil in the second decade of the 20th Century shows the ambition – and folly – of the 100-year old British-French plan that helped create the modern-day Middle East.

Straight lines make uncomplicated borders. Most probably that was the reason why most of the lines that Mark Sykes, representing the British government, and Francois Georges-Picot, from the French government, agreed upon in 1916 were straight ones. — BBC News

If Franz Ferdinand had not been murdered on this day in history, that conflict between the Serbs and the Austro-Hungarian Empire may have been contained to just the Balkans. Maybe.

The butterfly effect. Think how many small events, decisions, mistakes, one small turn, or “minor perturbations” in plans have had enormous consequences in your own personal life.

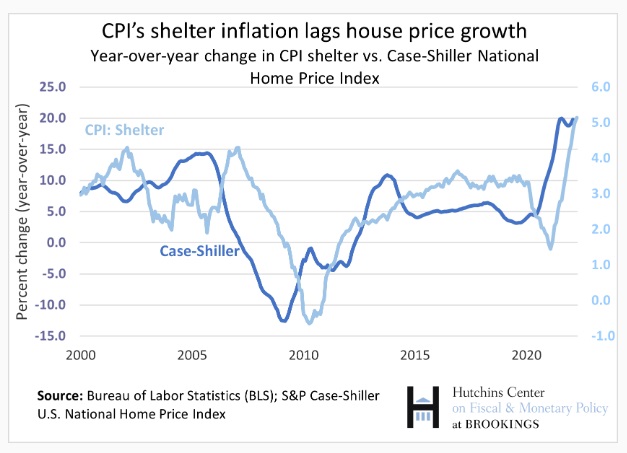

Over time, changes in house prices do predict changes in rents—although the relationship is far from 1 – to-1 and occurs with long lags. Xiaoqing Zhou and Jim Dolmas of the Dallas Fed find house price growth’s correlation with OER inflation peaks at about 0.75 after 16 months; the correlation with rent inflation peaks at after 18 months. – Brookings

The Fed is under a lot of heat for letting inflation get out of control, which is now generating super hawkishness even among the most gentle of monetary doves. The scorching is illustrated in the above NY Times headline.

We are reposting our piece from last April 2021, Just In Case, You Think The Fed Has A Clue, in which we questioned the Fed’s economic sanity to keep buying mortgages while the housing market was in a massive bubble.

Bond yields are now spiking, and the stock market suffers because of the monetary authorities’ ineptitude as the economy contemplates a bond and stock market without central banks. The major buyers of Treasury securities since the beginning of the century have now morphed into net sellers in aggregate.

Nevertheless, making monetary policy is difficult, especially in the last few years, so we grant policymakers considerable grace.

Valuations and multiples have to come down as interest rates rise.

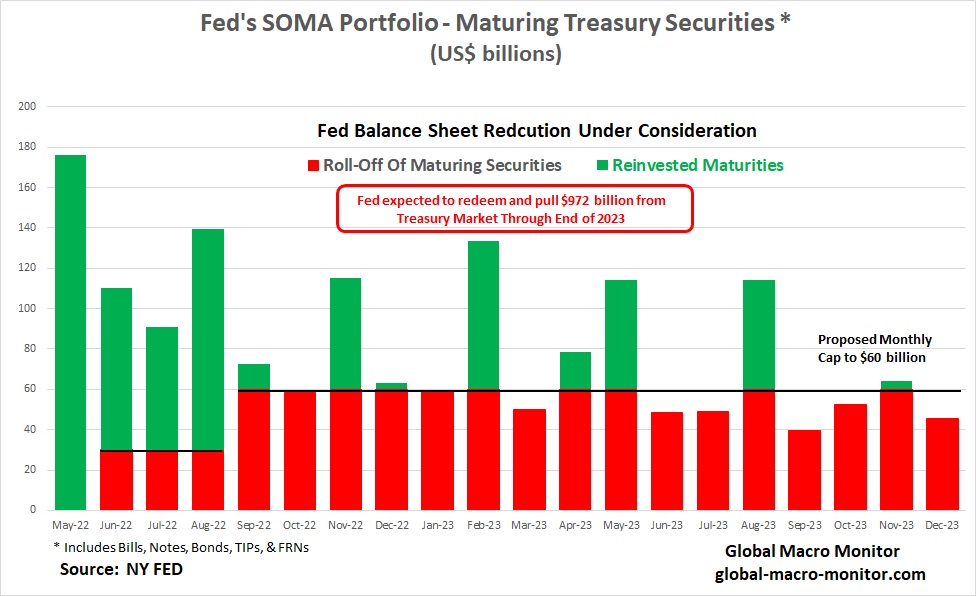

Given the FOMC’s latest statement on balance sheet reduction, we estimate the Fed will be extracting almost $1.5 trillion from the economy throughout 2023, approximately $972 billion from the Treasury market, and a maximum of just over $500 billion in mortgages.

Inflation As The End Game

However, we doubt the Fed and the American body politic have that high of a pain threshold for the subsequent economic and financial pain such a monetary tightening will bring. We, therefore, expect inflation will be the end game but only after, at the very least, a few deflation scares. When the going gets tough, the Fed will default to the mantra of most central banks and monetary authorities throughout history,

Print [debase], baby, print [debase]!

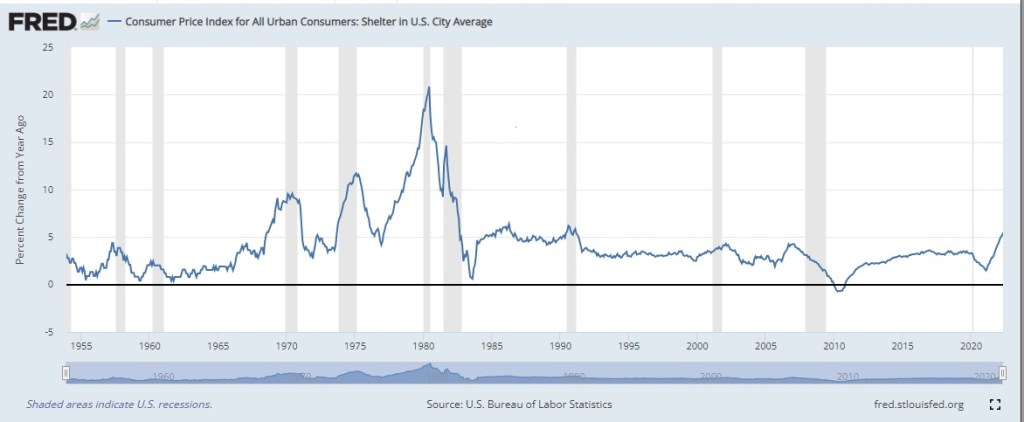

Housing Is Now The Problem, And Its Measurement Is Fatally Flawed

We estimate the Fed bought over $525 billion in mortgages between March 2021 and March 2022. During this period, the housing market was in Fuego with FOMO panic buying, driving up the National Price Index by 18 percent during the same period.

Moreover, the 30-year fixed-rate mortgage rate was up 150 bps, or 47.3 percent, driving up the cost of the monthly mortgage payment on the average house price in the United States by almost 75 percent. Let’s repeat that, folks, our best approximation of the cost of a monthly 30-year fixed-rate mortgage payment is up 75-100 percent in the past year.

The official measure for owners’ residential home inflation in the CPI basket is up a relatively measly 4.5 percent year-on-year as measured by Owners Equivalent Rent (OER), 24 percent of the CPI basket. What a complete joke.

Watch this space in tomorrow’s CPI release. [OER came in today up 4.8 percent y/y, which kept the overall number hotter than expected.]

The spike in mortgage payments has priced out most first-time buyers, forcing them into the rental market (7.4 percent of the CPI), raising rents by over 4 percent in the past year.

Different Housing Market Than The GFC

Of course, the housing market is in a much different condition than it was at the onslaught of the Great Financial Crisis (GFC), as all cash payments — an acute reflection of too much “money” in the system — have replaced the funky, highly levered subprime mortgages.

The result should be the reverse of the GFC, where housing prices collapsed almost overnight. This time, we expect a slow and chronic leak in housing prices with fewer forced bankruptcies, and less sensitivity to mortgage rates as they continue to climb until the Fed gets rolling in draining the excess money from the economy.

OER Starting To Track Real Housing Costs

Let us beat this dead horse one more time.

The above chart also illustrates that OER is starting to track the monthly mortgage payment for the first time, which is not a positive for the Fed or inflation.

The reason for this apparent disconnect is that most homeowners and renters did not move in 2021. They thus did not have to pay the spot price for shelter as it rose rapidly. Instead, many had to pay the rate that they signed for earlier in the year or the rate they signed for years earlier that had been modified slightly by their landlord or bank. These prices should tend to converge to the market price, but the lag time may be significant and the convergence incomplete. – VOX.eu

If homeowners have changed their perfunctory answer to the BLS survey question used to calculate 24 percent of the CPI

“If someone were to rent your home today, how much do you think it would rent for monthly, unfurnished and without utilities?” – BLS

to one where homeowners perceive themselves as real renters that track real mortgage costs, or if they get the Airbnb bug, the measured inflation rate for shelter will continue to rise. This may or may not be happening but keep it on the radar.

We feel for first-time homebuyers caught up in the FOMO bubble of the past year. We concede they may have some inside knowledge of a potential spooky inflation to come, but stretching to buy a starter home on a limited budget when interest rates are at artificial and historic lows, and prices at record highs can, and most likely, will be a toxic cocktail. Of course, we are not talking about the properties or “LifeStyles Of The Rich And Famous.”

Can’t wait to hear the Chairman justify zero rate policy and deficit monetization with inflation roaring at > 5 percent. It would be entertaining if it weren’t so damaging.

Watch Jay Pow stumble over this question of why they are buying $40 billion a month in mortgages when there is a dearth of supply in housing.

Here’s a pretty good theoretical model (follow the entire thread) estimating that U.S. inflation may reach double digits by Q1 2022. One of the premises is that monetary authorities have no way out of this rabbit hole and are constrained by the risk of severely disrupting financial markets in an asset dependent economy.

Recall our view that deflation/inflation is a corner solution and Wall Street’s “Goldilocks” scenario is still just a marketing gimmick. Deflation as markets try to move back to mean valuations – a lot lower – or inflation, and lots of it.

1/n How much excesss liquidity has US monetary easing created? And how much inflation will it create?

Anyone with a better model, lay it on the table. Stop with the “fake news” or “don’t worry” nonsense. CPI prints > 4 percent in May and you heard it here first.

GMM’s HealthWars

CK and I are battling some serious health issues. Mine, an acute skirmish, which I am now recovering.

CK’s, a three-front protracted war. Her courage to get up and fight everyday has been such an inspiration during my little battle. She also saved my life by forcing me to “ignore my primary doctor’s diagnosis of “all is well” and aggressively pursue my symptoms.” If not for that, the Grim Reaper would have liquidated my position and GMM would be no more. Thanks, CK.