-

In economics, things take longer to happen than you think they will, and then they happen faster than you thought they could.

-

Join 1,204 other subscribers

Contribute To GMM

Categories

- 3D Printing

- Agriculture

- AI

- Algos

- Apple

- Automation

- Banking

- BFTP

- Bitcoin

- Black Swan Watch

- Bonds

- Brazil

- Brexit

- BRICs

- Budget Deficit

- Capital Flows

- Cartoon of the Day

- Cashless Society

- Chart of the Day

- Charts

- China

- Clean Tech

- Climate Change

- Coach C

- Commodities

- Coronavirus

- COVID

- Credit

- Crude Oil

- Currency

- Cyprus

- Daily Risk Monitor

- Day In History

- Debt

- Demographics

- Disinflaton

- Dollar

- Earnings

- ECB

- Economics

- Economist

- Egypt

- Electric Vehicles

- Emerging Markets

- Employment

- Energy

- Environment

- Equities

- Equity

- Euro

- Eurozone Sovereign Spreads

- Exchange Rates

- Fed

- Finance and the Good Society

- FinTech

- Fiscal Cliff Monitor

- Fiscal Policy

- Food Prices

- France

- Futurist

- Game Theory

- General Interest

- Geopolitical

- Geopolitics

- German Bund

- Germany

- Global Macro Watch

- Global Reset

- Global Risk Monitor

- Global Stock Performance

- Global Trend Indicators

- Gold

- Greece

- Healthcare

- Heat Map

- Hedge Funds

- Housing

- Human Interest

- Immigration

- Impeachment

- India

- Inequality

- Inflation/Deflation

- Infographics

- Innovation

- Institutional Investors

- Interest Rate Monitor

- Interest Rates

- Interviews

- Italian Yields

- Italy

- Japan

- Jobs

- Lectures

- Macro Notes from Conference Calls

- Manufacturing

- Masters

- Mexico

- Monetary Policy

- Movies

- Muni Bonds

- Muni Market

- Natural Gas

- News

- Nonlinear Thinking

- North Korea

- Overbought Markets

- Picture of the Day

- PIIGS

- PMIs

- Policy

- Politics

- Population

- Populism

- Poverty

- President Trump

- Qunat Strategies

- Quote of the Day

- Quotes

- Rare Earth Elements

- Readership

- Reads

- Real Estate

- Relative Strength Index

- Robert Shiller

- RSIs

- S&P500

- Sector ETF Peformance

- Semiconductor prices

- Semiconductors

- Social Media

- Socialism

- Song for the Week

- Sovereign Debt

- Sovereign Risk

- Spain

- Sports

- State and Local Government

- Tail Risk

- Technical Analysis

- Technology

- The Big Reset

- The Weekend Read

- This Day In Financial History

- Trade War

- Trades

- Tweet of the Day

- Ugly Chart Contest

- Uncategorized

- US Releases

- Video

- Volatility

- Wages

- Week Ahead

- Week in Review

- Weekend Reads

- Weekly Eurozone Watch

- Whales

-

Recent Posts

Meta

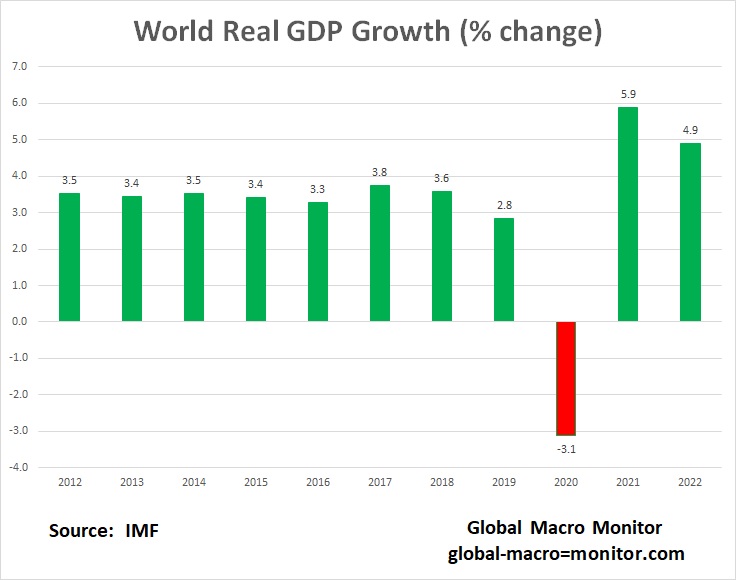

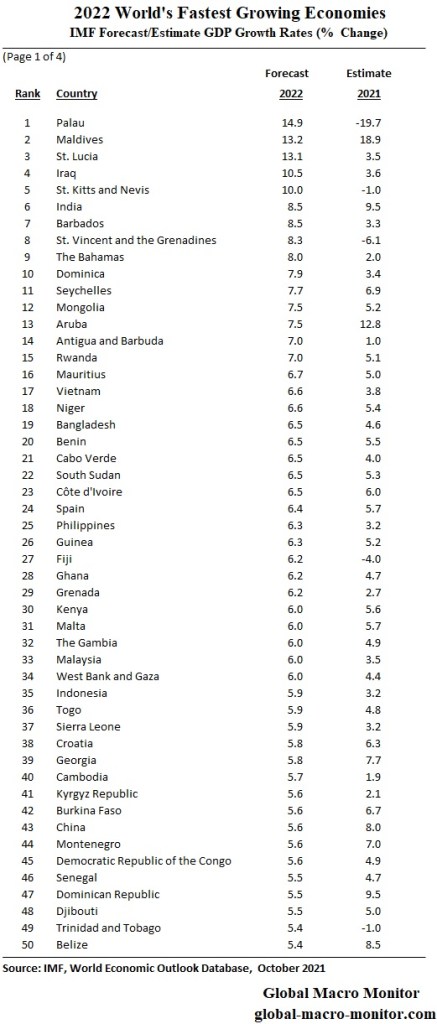

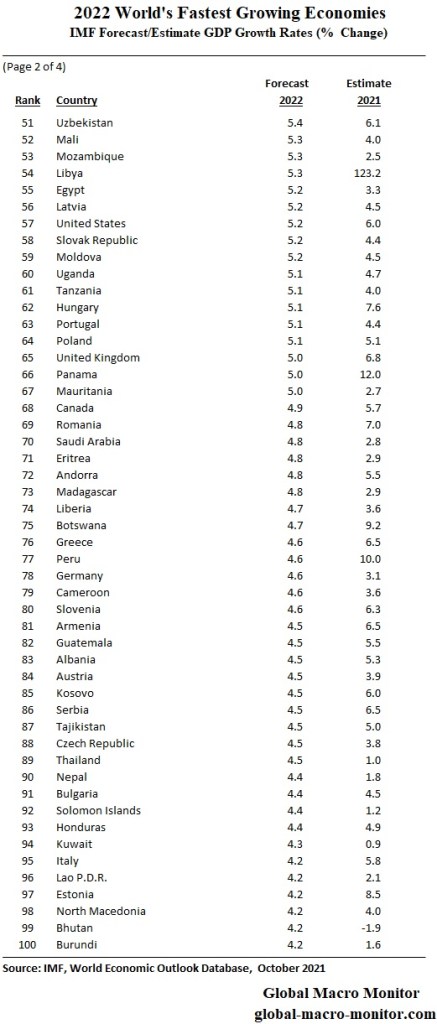

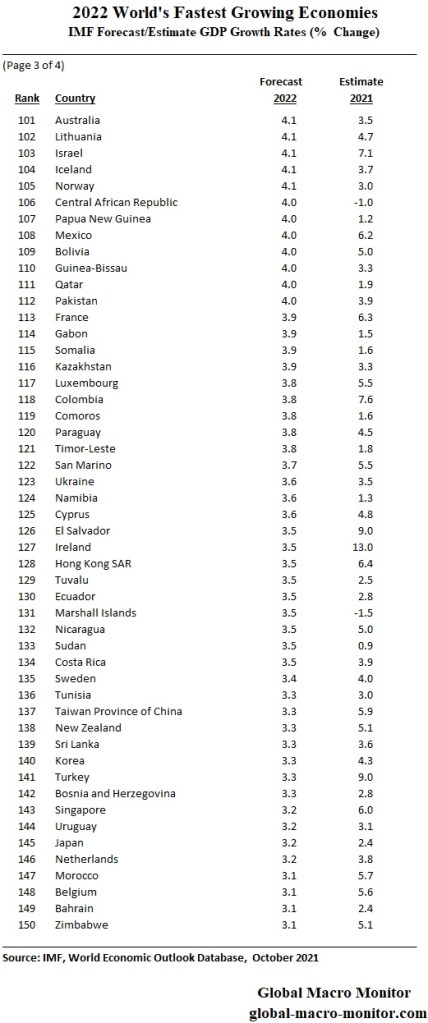

World’s Fastest Growing Economies In 2022

We have updated our tables of the IMF’s forecast and estimates of GDP growth rates for the G20 and the rest of the world for 2022 and 2021. The post has always been a favorite for our readers. The 2022 forecast ranks the world’s fastest to slowest growing economies in the ginormous table below.

The data are from the October 2021 IMF’s World Economic Outlook so are a bit stale and do not reflect the new COVID variants but are close enough for government work and snapshot of the coming year.

We have also added a chart of world GDP growth to illustrate how disruptive the COVID shock was. Some advanced economies are now overheating from too much stimulus, including the U.S., and will need to adjust fiscal and/or monetary policy. It’s is very difficult to forecast during the pandemic.

Posted in Uncategorized

Leave a comment

The COVID-19 League Of Nations

Great chart from the Economist on how nations are faring during the pandemic using a multiple of indicators. Those damn Nordic socialist countries are kicking our arse!

The pandemic has created winners and losers—and the dispersion between them is likely to persist in 2022.

In order to assess these differences, The Economist has gathered data on five economic and financial indicators—GDP, household incomes, stockmarket performance, capital spending and government indebtedness—for 23 rich countries. We have ranked each economy according to how well they have performed on each indicator, creating an overall league table (the chart shows the ranking and four of our five indicators). Some countries remain in the economic pits, while others are faring better than they were before the pandemic on almost every measure. Denmark, Norway and Sweden are all near the top, and the American economy has also performed reasonably well. Many big European countries, however, including Britain, Germany and Italy, have fared worse. Spain has done worst of all. – Economist

Posted in Uncategorized

3 Comments

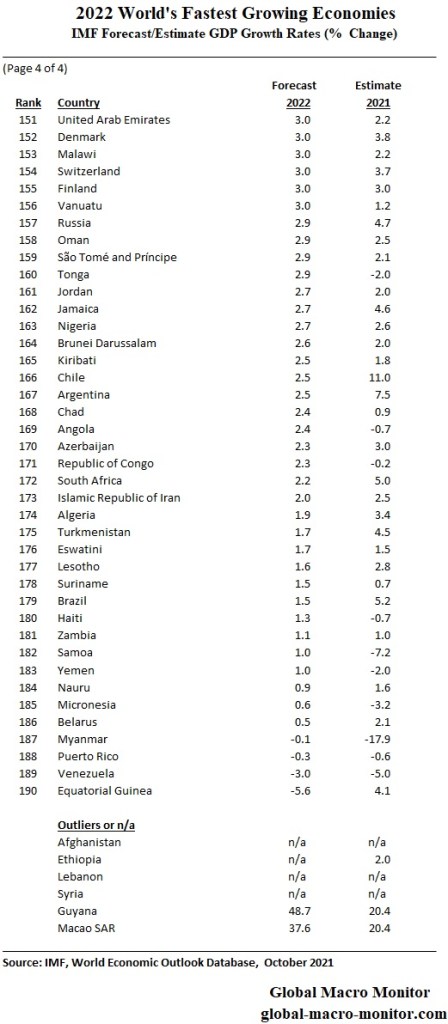

Not Quite In Full Flight

According to Exante Data , creator of the following chart, U.S passengers now screened by the TSA is back to 83 percent of the 2019 levels. Getting there but not home yet.

I dropped my daughter and her significant other at SFO on Christmas Day to fly to London. At the same time, a good friend, known as Harry The K. on this site, flew back from Heathrow and is sick with THE symptoms but is yet to be tested. Godspeed, HTK.

Let’s take every precaution, throw off the fear and get back to normal. Don’t live like what King Solomon described as those who were afraid to get out of bed because “there are lions roaming the public square.”

May science and the miracle of modern medicine coupled with our unselfish and empathetic behavior kick COVID’s ass in 2022. Let’s do this, folks!

Posted in Uncategorized

Leave a comment

Envy Always Leads To Misery

Hope everyone is enjoying the Holidays.

This is a great video worth a few minutes of your time, especially the FOMO crowd.

Look for big changes coming to GMM in the next year.

Happy New Year! A healthy and prosperous one.

Posted in Uncategorized

2 Comments

“Consumers Spending At The Fastest Pace We’ve Ever Seen”

NEW YORK (AP) — The head of the nation’s second-largest bank said consumers are spending “at a faster rate” than he’s ever seen but he remains concerned about how inflation and supply-chain issues will influence the economy going into the winter. – Brian Moynihan, CEO, Bank of America

The above statement by Brian Moynhan jibes with our view and posts over the course of 2021.

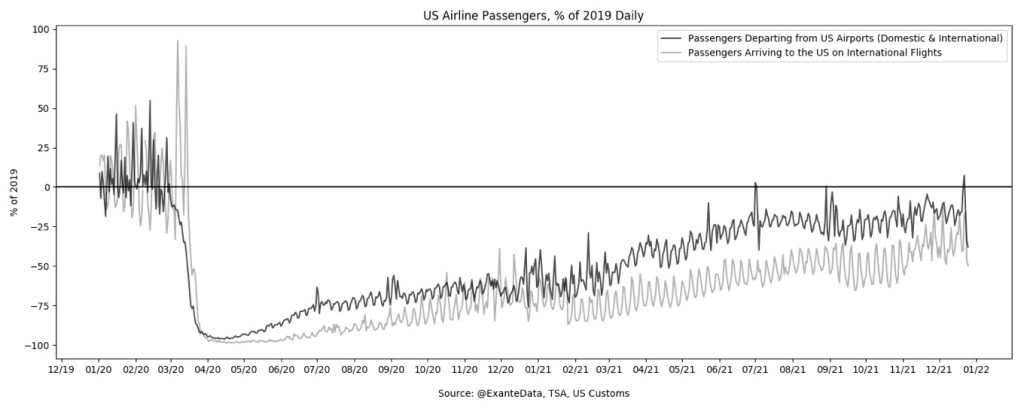

In our last post, a bit too wonky, we tried to convey how out of whack the bond market is with the economy. We have redone the chart to rid it of the COVID outliers and it more clearly illustrates the historic difference beween nomimal GDP growth, which should come in aournd 15 percent in Q4, and the 10-year note yield. The differential this quarter will come in only second to Q2 1978.

The data clearly illustrate the odd and unprecedented times in which we live. The stock market is going up, however, so “all is calm, all is bright.” Am I right?

Moreover, we have a sense the market is coming around to what we have been saying over the past few months: the economy is overheating and the Fed has some very heavy lifting to do.

We are reposting our chart on retail sales, which shows how far out of line current spending is with its pre-COVID trend.

We also maintain the primary factor causing inflation and the supply chain debacle is excess demand, the result of too much stimulus not just from the Fed but all the major central banks and governments.

The Fed may have to surprise on the hawkish side tomorrow but we’re doubtful as they don’t have the stomach for the pain it will cause in the stock market.

As Greenspan was in the 2004-07 tightening cycle, we suspect this Powell tightening will be way too slow and not bold enough.

Our bet is if the S&P craters, Powell will cave. Hence inflation will be a more permanent feature or the U.S. economy going forward.

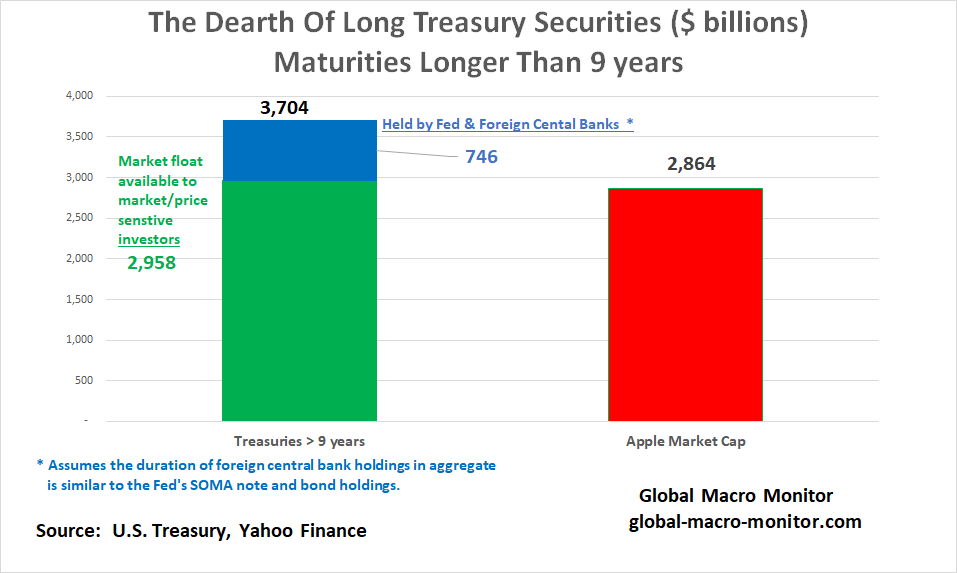

The dearth of longer maturity Treasury coupon securities has significantly distorted the yield curve.

Reverse Operation Twist

The Fed should also consider a reverse Operation Twist, where they sell or announce they are going to swap their long-term Treasury notes for shorter maturities. This would steepen the yield curve and slow down demand in the bublicious housing market and, more important stifle the market yapping that the world is coming to end because the yield curve is flattening or inverting.

Lack of price discovery in the bond market is going to become a very real problem for monetary policymakers throughout the world.

Go to 20 seconds in to hear Moynihan’s comment on the consumer.

Posted in Uncategorized

Leave a comment