Global Stock Indices

Good week for stocks.

Major U.S. major indices closed at record highs. Brazilian stocks at new highs as traders remain confident President Temer will implement market reforms even though he faces a second round of corruption charges, of racketeering and obstruction of justice, which were brought against him on Thursday. Risk doesn’t seem to matter anymore.

Emerging markets all the rage this year.

The NIKKEI up on big yen sell-off and North Korean missile fatigue.

Greece continues to sell off as reports the IMF could conduct a Greek bank asset quality review as part of its third bailout review. Last month, Reuters reported that bad loans accounted for 50 percent of bank loan portfolios last year.

Global 10-year Bond Yields

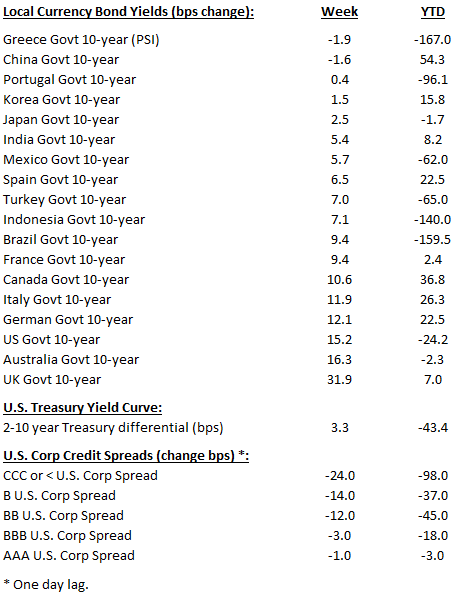

Interest rates up big in the Europe and U.S. last week.

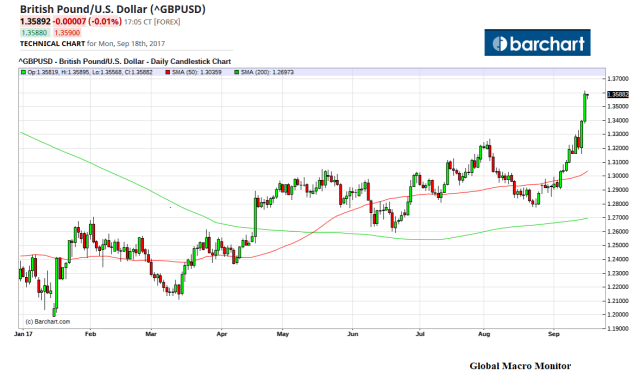

The U.K. especially hit hard as the view, expressed by a majority of the nine-member monetary policy committee (MPC) at Thursday’s meeting, that “rates could rise in the “coming months“ to buffer inflation risks. U.K. inflation is expected to soon hit 3 percent, mainly the result of the crash of the sterling after the Brexit vote.

Inflation? When was the last time inflation was on the radar in any of the G5 countries?

Even the U.S. printed a hot CPI number on Thursday at 0.4 percent (versus 0.3 expected) increasing 1.9 percent y/y. The core rate came in at 0.2 percent ending a five-month streak of weaker-than-expected data, mainy due to an increase in shelter. Odds of a December Fed rate hike jumped markedly.

Federal funds futures implied traders saw about a 52 percent chance the U.S. central bank would raise the target range on key short-term borrowing costs by a quarter point to 1.00-1.25 percent in December, up from 42 percent prior to the latest reading on the consumer price index, according to CME Group’s FedWatch program. – Reuters, September 14

The head for spread continues as high-yield came in double digits, with the dash for trash outpeforming, probably due to the robust and more sustainable stronger global economic outlook and, of course, spread panic.

Bahrain priced its $3bn, three-tranche bond issue at 5.25 per cent for 7.5-year money, with a 12-year maturity at 6.75 per cent and a 30-year tranche at 7.5 per cent. Investor demand was strong with deal 5x oversubscribed.

Bahrain is rated BB- by S&P and BB+ by Fitch, both with a negative outlook.

Portugal regained their investment-grade sovereign credit rating, with S&P raising its rating on the country by a notch from BB+/B to BBB-/A-3 on Friday.

The stable outlook balances our expectation of solid economic growth and further budgetary consolidation, as well as receding external financing risks over the next two years, against the risks of a weakening external growth environment and vulnerabilities emanating from high, albeit falling, private-and public-sector debt. – S&P via FT, September 15

China plans to bring a dollar-denominated bond for the first time in a decade, The final terms are not yet set, but Beijing is expected to raise up to $2bn, most likely in 10-year notes.

The Russian central bank cut rates 50 bps to 8.5 percent.

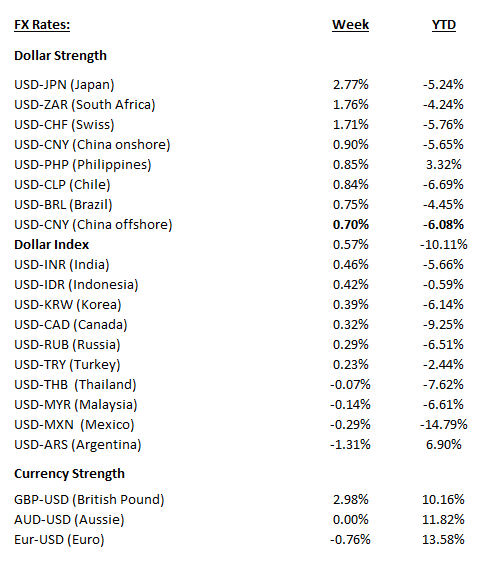

Global Currencies

The story of the week was the the British pound for all the reasons mentioned in the bond market review above. The yen also had a tough week as traders seem to be questioning its haven status as missiles from North Korea fly over the island nation.

The dollar index continues to hover around 92 as the euro/dollar is having trouble breaking through the 1.20 level. Watch 91 on the index now.

Why is the euro rallying? Because it can.

Bonds are slow to adjust to the much improved economic and inflationary conditions in Europe due to repression caused by the ECB’s asset purchases (QE). The pressure has to be released elsewhere, and the currency market has little or no government intervention and trades relatively free. It may also be causing the euro to overshoot.

The short-term fate of the dollar is dependent on the Fed’s FOMC statement and press conference this coming week.

Will they announce the of start quantitative tightening (QT)?

Given the significant loosening of financial market conditions since the beginning of the monetary tightening cycle, we think so.

It is going to get interesting from here, folks.

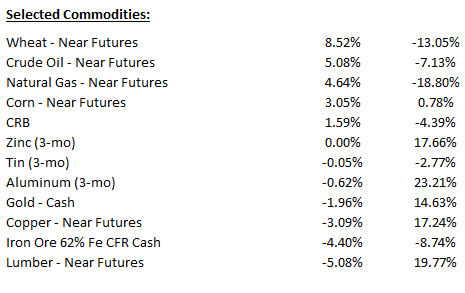

Select Commodities

Hedge funds, running net short, were covering their wheat futures at the end of the week as worries over the Australian crop due to colder than normal conditions made traders nervous.

Crude up nice on the week. It appears the market is balancing quicker than expected. Global demand is starting to accerelate with the global economic recovery.

Risks to the price are a ramp in U.S. production and backsliding by OPEC due to the higher prices. Upside price risk, include Venezuela production is declining and there is pressure on Libyan, Nigerian, and Mexican production. Also note the widening spread in Brent and WTI spread (see our Global Risk Monitor – other risk indicators),

Finally, we continue to see a wide spread between WTI and Brent. That spread has been above 10 percent for five consecutive daily trading sessions.

The last time this happened, it came at the end of a significant trend in which the spread expanded to a double-digit percentage difference, with early September 2015 comprising the end of the cycle. Two periods of major pricing advances occurred during that trend. – OilPrice.com, September 15

Iron ore seems to have put in a short-term top on the weaker China data that came out late in the week.

Lumber futures came under pressure on Friday mostly due to the roll in the daily nearest contract and there is now speculation the U.S. government may have to back away from tarrifs imposed on Canada due to an unexpected increase in lumber demand to rebuild Houston and Florida after the dual hurricanes. Lumber prices are already up 20 percent this year.

… Paul LePage, the Republican governor of Maine, asked the U.S. to at least suspend the tariffs until the hurricane rebuilding has been completed.

LePage said “corporate greed from a coalition of big lumber companies” already sent softwood market prices soaring.

“Making a profit is the goal of any company — and it should be,” LePage wrote in an op-ed in The Maine Wire.

“But it is unconscionable that this coalition is in a position that could lead to price-gouging Americans in distress.”

The National Association of Home Builders in the United States made a similar plea to the White House earlier this month. – The Canadian Press, September 16

Other Risk Indicators

Semis continue to rock partly due the bitcoin story.

European banks up on higher interest rates across Europe.

The Russell is making a nice bounce and now back above 1,400, a key level, which reflects postive growth expectations.

Bonds and VIX down big.

What Is On Our Radar

The FOMC will be big this week.

We do expect them to announce the start of the quanitiative tightening (QT). Financial market conditions continue to loosen. The window is open.

We are expecting a speed wobble but no big market disruption. Yet. The level of reserves are so high in the financial system a few $10 billion here and there will not do much. A 10 percent reduction will start to bite.

Flows matter? Not yet.

QE3 stopped long ago and the markets keep on rocking. It appears credit based money is partially picking up the slack of the the termination of central bank base money as QE ended in the United States.

With the markets in full blown “beast mode” they will probably focus on a possible lowering of the dots and use it as an excuse to move higher, setting up a bigger October correction, in our view.

European Bond Market

We are watching the European bond market very closely because that is where the big bond bubble is. Growth and inflation are accelerating in Europe, and interest rates are waaaay out of line.

A temper tantrum in the European bond market, causing a spike in market interest rates spilling into the U.S. is the trigger most probable on our event risk checklist that will cause the short sharp sell-off in risk markets in October that we are expecting. We will have a post later in the week with more in depth analysis.

The U.K. may be the canary in the coal mine – a spike in 10-year rates of 32 bps, or over 30 percent, this week. Inflationary fears causing interest rates to spike is possibly the worst case economic scenario for the risk markets.

Nevertheless, risk loves the global growth Goldilocks scenario, for now, and still cannot stand 0-2 percent interest rates. All in the context of extreme valuations.

We expected a blow off buying spree in September setting up for the October correction.

It now feels like we are in that giddy/blow off stage. All lathered up and only a little more to go.

Wouldn’t chase here, unless your a very short-term flipper, and would be reducing risk going into October. No shorting until the break and then be quick on the draw to cover as everyone aglo in the virtual world will be looking to buy the big dipper.

Then it will be time to reassess the probability the raging bull market continues (doubt it) based on the inflation outlook, future ECB and Fed policy, and, probably most important, the action in bonds markets.

No Big Bear Yet

It is currently hard for us to imagine a 2000 or 2007-08 scenario with the synchonized global growth story until interest rates move several hundered basis points higher in Europe and 100-200 bps higher in the U.S. x/ some Black Swan event. Higher interest rates will bring the extreme valuations to the market forefront.

In general, never short risk markets, unless for a short-term event driven trade as you know John Bull can stand many things but he cannout stand negatitve, zero, and two percent interest rates. Yield and return chasers will run you over.

A seven to plus ten percent correction and a decent blow out in credit spreads precipitated by a European bond market temper tantrum given current valuations? In a heartbeat.

Mr. October on deck.

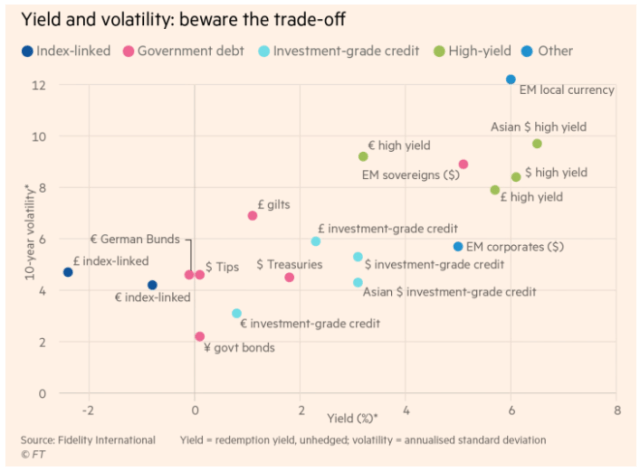

Key Charts

.

.