I had an interesting conversation with an economist friend this morning about inflation and excess capacity. He sees no evidence of excess capacity in the U.S. economy, including the service sector, where he cannot find, say, a plumber for hire to do some home improvements.

We then moved on to an esoteric conversation as to why those inflationary pressures are not showing up in the official data. They do seem to be building in the pipeline, however.

We concluded mismeasurement, archaic data collection, the deception of averaging, and mused that in the coming years economic data would be measured in real time by big data and we will not have to wait months for GDP and measurements of inflation. That is looking in the rearview mirror as to how the economy is functioning and trying to work through the noise of lousy data.

Asset Markets

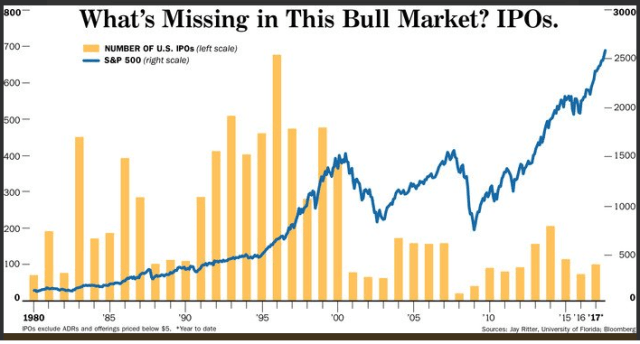

Speaking of lack of capacity, take a look at the lack of new stock supply (IPOs) and removal of old stock supply (buybacks) from the market over the past few years, which have been a big driver of this bull market. At the end of the day, Econ 101 teaches us an increase in demand (yield chasing in the current case) while supply remains constant or declines drive prices higher, no?

We have written about this in past posts, which apply to the housing and risk-free bond markets as well.

Our family just survived the Northern California fires with one of our old houses going up in flames. Five percent of the housing supply in our city, already in bubblicious mode, burned down.

Now a very odd market. Existing housing supply is nonexisistant yet land values in the burned out areas are plummeting.

Upshot

A different type – a supply restricted – bull market in many of the asset classes, which artificially lowers the relative cost of capital in some and makes expanding capacity in other real sectors — investing in automation, for example — cheaper than hiring new workers.

All in all, sounds smells and acts like inflation to us, which can destroy jobs just as deflation destroys jobs. Especially as the asset imbalances lead to the boom/bust cycle, which we have experienced already twice early in this century to the extreme. If it keeps us, we will have to start needing seasonal adjustments on the S&P500!

Arghhhh… Those distortions.

The majority of economists need to widen their vision of how they perceive as inflation. Instead of calling it “financial imbalances,” for example, call it for what it is: asset inflation. In addition, understanding that inflation in one sector can distort and result in adverse disinflationary forces in others, with a relatively artificially cheap cost of capital.

P.S. This has been an extremely difficult year, but I still have much to be thankful for. Great family and beautiful daughters. Priceless!

Happy Thanksgiving, folks.

.

.

Pingback: Heads Up! Friday’s Rare S&P Shooting Star Candlestick | Global Macro Monitor