We began the week with our Watch This Space post:

Because the eurozone is where the big bond bubble lives.

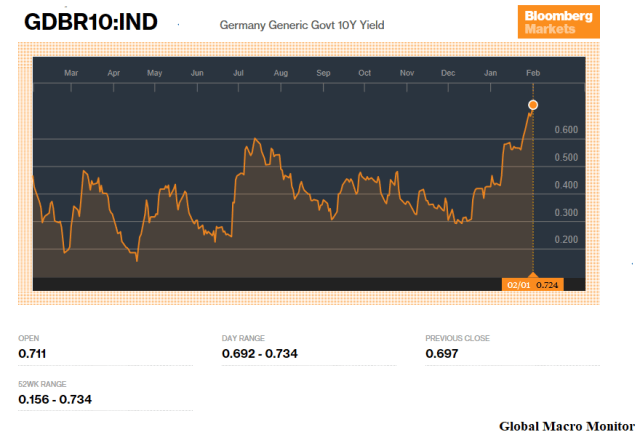

Though the euro periphery is now in Convergence 2.0 mode on hopes of eMac’s vision of a more integrated ‘zone, the German 10-year is at a critical level, and yields only 63 basis points in an economy that is probably growing close to 5 percent on a nominal annual basis. It reflects a stunningly loose monetary policy and a central bank way behind the curve.

The repressed yield is technical as the German government’s new bond issuance is virtually nil as it runs a budget surplus and the dearth of bunds is exasperated by the ECB’s quantitative easing. We have referenced this as a major factor of the “steel bubble” in asset prices, the bursting of which is very stubborn.

A spike in bund yields could put further pressure on U.S. bond yields and may be the trigger for the long-awaited and ever fleeting equity market correction. Maybe.

Stay tuned.

Full stop.

Bund yields have broke higher this week, up 10 basis points.

Greenspan Speaks

Former Fed Chairman, Alan Greenspan, weighed in yesterday talking bubbles.

Let me put it to you this way. I think there are two bubbles. We have a stock market bubble, and we have a bond market bubble. I think at the end of the day the bond market bubble will be the critical issue……we are working our way to a major increase in long-term interest rates. – Alan Greenspan

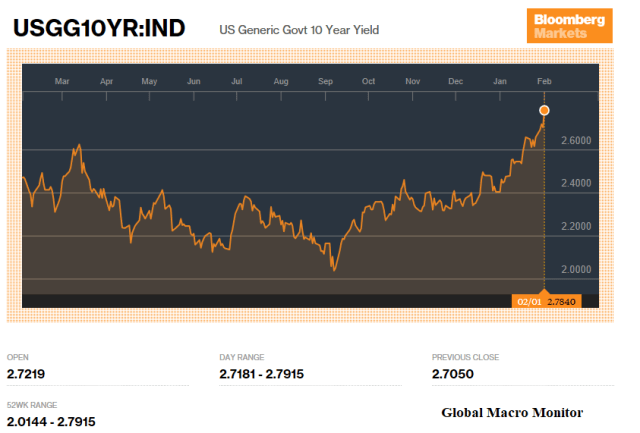

Global Bond Yields Spiking In New Year

Bond markets of the advanced economies are having a rough start to the year as the global economy gathers steam and inflation expectations pick up.

More importantly, the markets are beginning to discount the supply distorting effects of quantitative easing coming to an end.

The U.S. budget deficit is set to accelerate, which will increase supply, coupled with the confluence of potential negative demand factors: 1) the Fed bid is gone and are now running off their Treasury book; 2) Bund yields are finally moving higher, reducing potential portfolio substitution; and 3) the direction of the dollar is dubious, which may spook off foreign buyers. In addition, a new and untested Federal Reserve Chairman.

Moves Off Low Base

The table illustrates the carnage in 10-year local currency sovereign bonds.

The absolute basis point moves mask the pain as the increase in yields started from such a low base. Focus on the relative moves in percentage terms.

The German bund yield has moved up almost 70 percent since the beginning of the year, and the Japanese JGB yield has more than doubled.

The U.S. 10-year is up nearly 40 bps, though smaller in percentage terms, but still substantial relative to the annual moves over the past three calendar years: 2015 – +9.9 bps; 2016 – +17.5 bps; and 2017 – -3.9 bps.

No sugar coating, folks. It’s been fast and furious.

.

We believe the bond market reaction to tomorrow’s employment numbers will be a huge tell. Bonds seem to be oversold and the fast money may be a bit offside going into the number (see the Quandl CFTC chart below). If a repricing is taking place and a bubble is indeed bursting, however, no need to be a hero by stepping in to catch a falling knife.

The New Narrative

We now hear that bond yields are just in the process of moving back to normal in an global economy that has healed thyself. Don’t worry.

We are always worried! Will markets be internally consistent here and also normalize asset values with the interest rate move, which are currently at rare historic extremes?

Probably not overnight, we suspect.

The rise in rates have landed a body blow to equity markets over the past few days, however, just like a Joe Frazier left hook. Stumbling, temporary down, but no knockout punch.

Warning Signal

Rising interest rates coupled with a falling currency, the ugly cocktail currently be mixed in the U.S., is never a good signal and always a red flag, in our book. Ask any veteran of emerging markets.

Moreover, ignore the large increase in public (and private) debt in many of the advanced economies over the past ten years at your peril. Rising interest rates will feedback into budget deficits, which will feedback into bond markets. Not exactly the loops we prefer.

.