Summary

- Global equities finished the first half relatively weak. The S&P500 moved back and tested the bottom of the old trading range of 2700-2742. We seriously doubt this range holds and expect lower prices unless POTUS gets religion on free trade. Doubt it

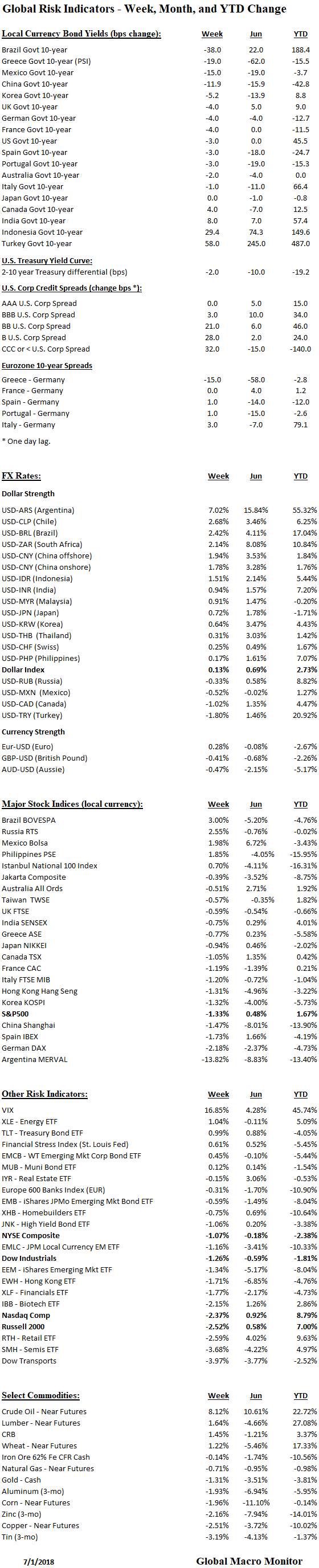

- Big barbell week in 10-year sovereign yields with Brazil down 38 bps and Turkey out 58 bps

- U.S. credit corporate spreads significantly wider on the week. Watch this space

- EM FX generally weaker, with Argentine peso down another 7 percent. Turkey and Mexico a bit stronger

- The U.S transports were hammered, down almost 4 percent on the week

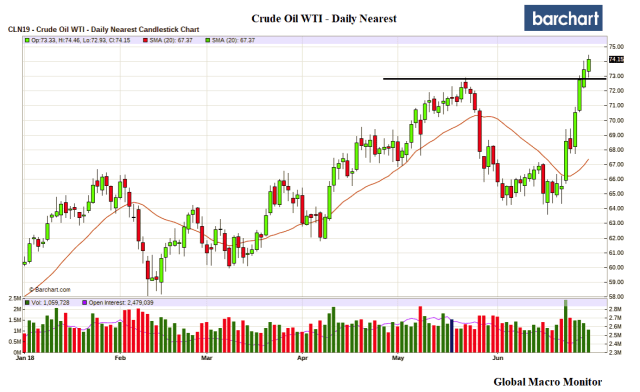

- Crude up 8 percent and climbing to $80. Trump claims he has a deal with the Saudi king to increase production. If true, which we doubt, bid adieu to OPEC. Trading down a little less than 1 percent at 20:30 eastern

- Surprising the hard roll in copper since June 7th

Commentary: Big events this week, though we expect quiet trading with the July 4th holiday and tomorrow’s World Cup match between Brazil and Mexico.

Our focus: 1) let’s see how crude responds to the Trump tweet; 2) how EM reacts to the election of the lefty president, AMLO in Mexico; 3) U.S. tariffs and retaliatory tariffs take effect on July 6th, and 4) most important, the Fed steps up it Quantitative Tightening cap to $40 billion per month,

We estimate the Fed will reduce its SOMA Treasury portfolio by $24 billion and the MBS book by $11.2 billion in July. It is more challenging to estimate MBS redemptions due to the uncertainty of prepayments. We also expect the SOMA portfolio will have only $6.3 billion available to rollover into Treasury auctions in July, which are increasing in size by 13 percent per month on average y/y in 2018. Thus Fed participation in July’s Treasury auctions will be reduced to 2 percent of total new issuance, compared to 7 percent in June and 15.6 percent in May. On the margin, and all other things being equal (they never are), this should put upward pressure on interest rates, especially if traders realize and internalize the data.

Since QT began in October 2017, we estimate the Fed has reduced its holding of T-notes and bonds by $98.3 billion and the MBS book by $46.9 billion, for a total of $141 billion. The balance sheet reduction is not insignificant and equivalent to around 3.7 percent of the U.S. adjusted monetary base. We maintain this is what really matters and should be the focus of investors and not the obsession over interest rates.