Summary

- Ugly Thanksgiving week for equities. S&P led all major indices lower

- Philippines stocks were the only major index in the green as stocks broke out of a range on positive sentiment due to lower oil prices and expected inflation

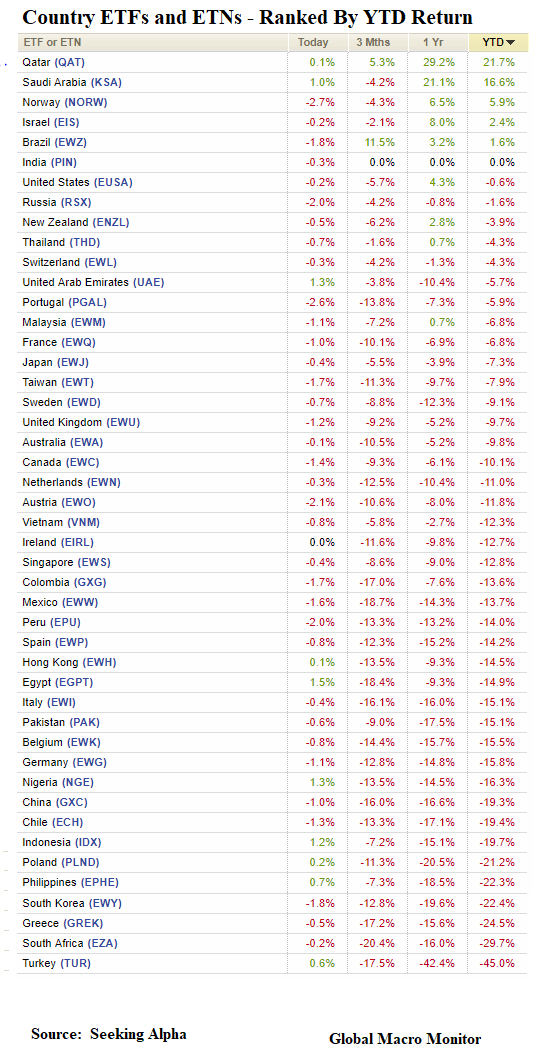

- Only Brazil, Argentina, and India stock are green YTD, and only in local currency terms. Negative, some extremely, when currency weakness is factored

- Table 2 illustrates 2018 has been a horrendous year for world stocks in dollar terms

- The U.S. 10-year yield was only able to eke out 2 bps on the big sell-off in stocks

- Credit spreads continue to blow out and November is the first month of credit weakness confirming stock weakness

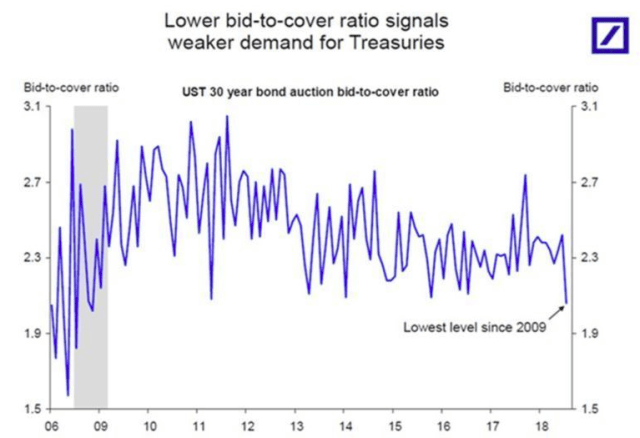

- Chart 2 confirms our prediction the demand for Treasury bonds is fading while supply is increasing. Could be a big problem. Watch this space

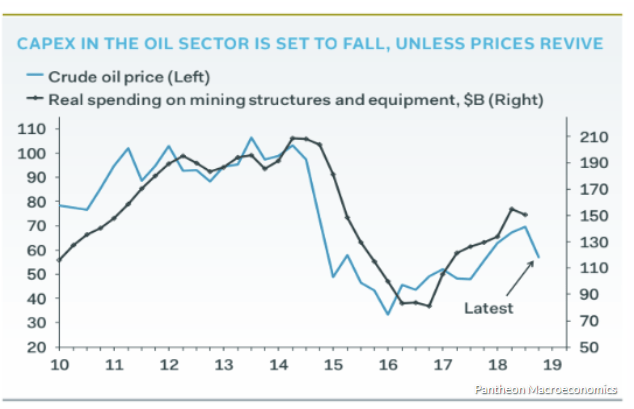

- Crude oil, down over 10 percent on the week, is way oversold but looks like a $40 handle is a done deal next week. Oil is a trending machine. Stay with trend and wait for the turn before even thinking about it

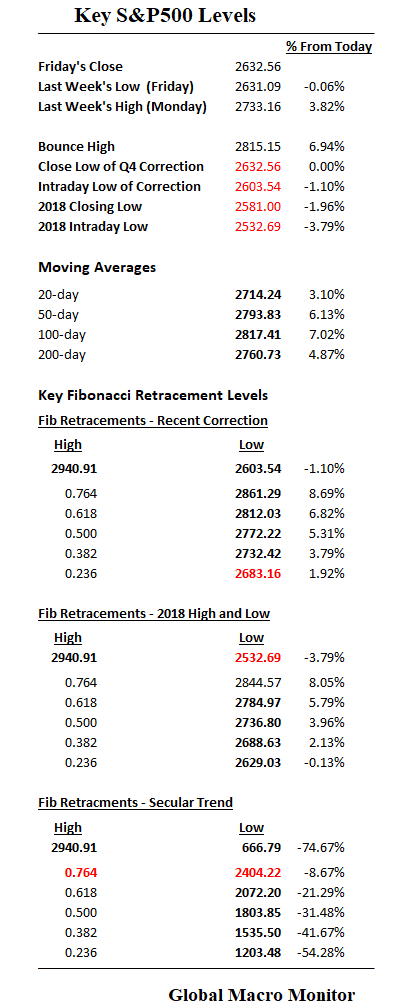

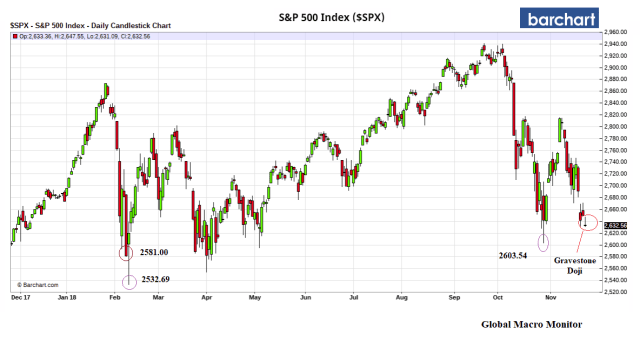

Commentary: Watching for some stability to return to stocks. The S&P Q4 correction intraday low needs to hold at 2602.54, which we have little confidence it will. Watch for a close below 2581.00, the 2018 closing low. That will increase the probability the 2018 intraday low of 2532.69 to around 90 percent. If that fails, stocks are in deep trouble.

Credit spreads also need to stabilize. Too many BBB bonds out there and feels like the floor is ready to give way.

Treasury yields are not behaving as they should — moving lower with stocks — as the technical position is out of kilter. New big issuance with declining demand from past buyers is not being absorbed by haven flows. We believe the Treasury market is crowding out all other assets and major factor of weakness in risk assets.

Note the divergence in Chart 6 of yields and oil prices. Many expect that to close, which it may a smidgeon, but not as the bond bulls expect. We are in a different world: a different fiscal regime and different buyers.

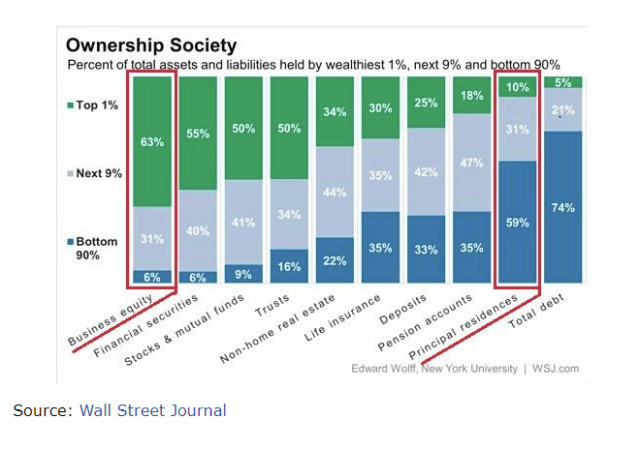

Chart 3 is a big flashing orange light that political instability is coming.

We expect at least an effort to bounce risk assets but it should be a feeble one and chance to sell. BEARISH.

Table 1

Chart 1

Chart 2

Chart 3

Chart 4

Chart 5

Chart 6

Chart 7

Table 2

Table 3