Summary

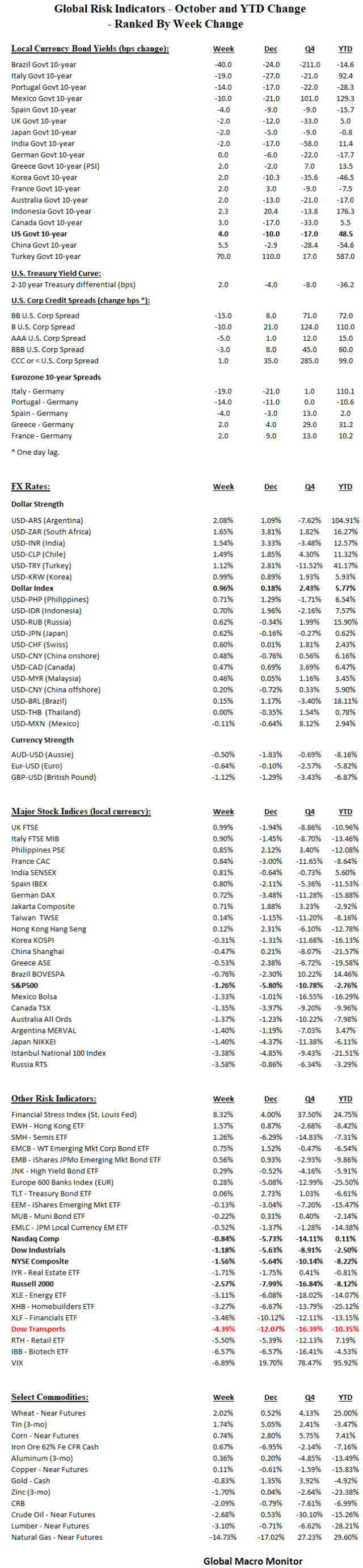

- Bond yields relatively stable in spite of weak and volatile equities

- Bookend EM 10-year yields – Brazil in 40 bps, Turkey out 70 bps

- U.S. credit stabilized last week

- Dixie traded to new 52-week high but couldn’t close above the November 12th closing high

- Cable getting schmoked on the BREXIT clown show. Starting to look interesting as we think the end game is “Exit the BREXIT” with a second referendum. Timing is tricky

- Euro sovereign spreads tighter

- The Russell continues to lead U.S. stock indices lower

- Transports hit again, now down over 12 percent in first two weeks of December trading. Watch this schpace.

- Nattie lives up to its name, “the widow maker” with yuuge vol. The grains are starting to look interesting. Trying to break out of trading range.

Commentary – The next week will close the books on a volatile and ugly 2018 for almost every asset class. Mr. Market is hoping Chairman Powell will pull a rabbit out of his hat at the FOMC this week. How is that it was the “greatest economy in the world” and no worries over the flat yield curve at the beginning of September to “the economy is sliding into recession” and beware the inversion of the yield curve?

Let us tell you why. At the end of September, the 10-year note yield broke out to new highs as the U.S. government borrowing requirement is hoovering up all the world’s dollar liquidity. The U.S. stock market cracked, and given the new economy, asset markets are now a huge driver of growth, very unhealthy in the long-term, especially with such a wide wealth disparity. The Fed is now effectively charged with keeping assets afloat and moving higher to keep the economy, at least, treading water. As wealth becomes more concentrated, the marginal effect of higher asset prices diminishes, resulting in a need for even higher asset prices.

We are not sure Chairman Powell will recognize this, or recognizes it all, for that matter. Monetary policy can’t change it, it’s too late. Only structural changes can fix the asset price driven economy

Dollar Liquidity

The markets are also now in a zero-sum game competing for dollar liquidity. The U.S. government borrowing requirements have never been higher, “the biggest dollar amount of securities for sale as a percentage of GDP since World War II“, and are on auto-pilot unless the Fed quits shrinking its balance sheet. Therefore the natural impulse is for interest rates to rise in the U.S. unless haven flows off-set the huge increase in the new supply of U.S. govies hitting the market.

Haven flows are generated by selling in other markets. That is exactly what has happened over the past six weeks. Don’t get lost in the noise, folks.

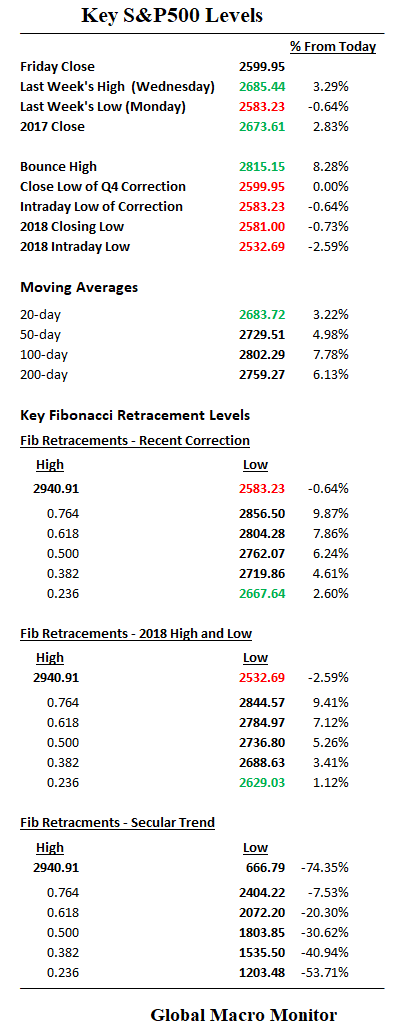

S&P

The 2018 closing low at 2581 beckons. We think a test of the year’s low at 2532.69 is a done deal. It’s a mug’s game but we believe going into to the new week they keep selling ’em and then a rally into the Fed meeting. The Fed is painted in a corner. If it recognizes weakness, the market sells. If they acknowledge the continued relatively strong data, such as retail sales and labor tightness, the market sells. In other words, pack it up and enjoy your holidays.

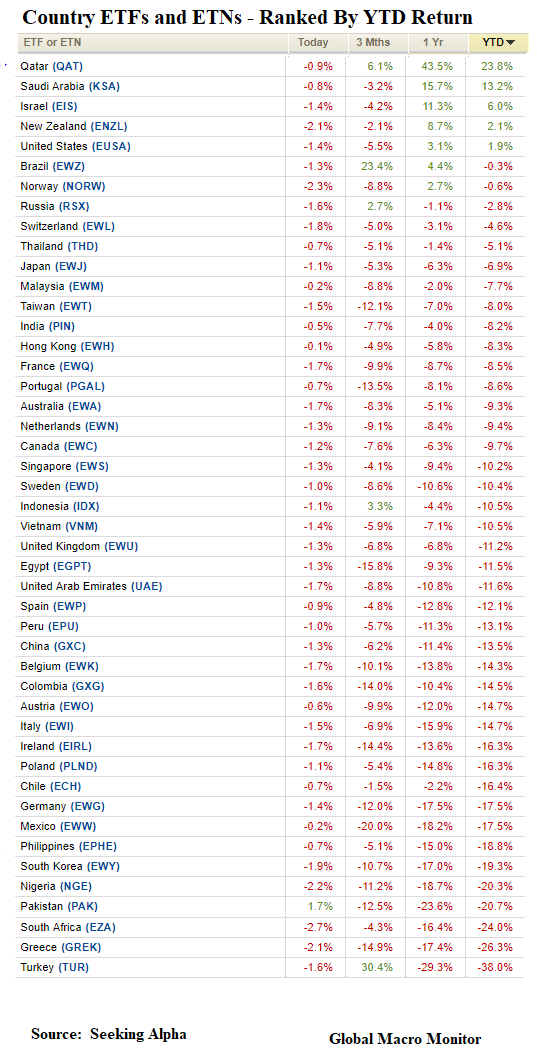

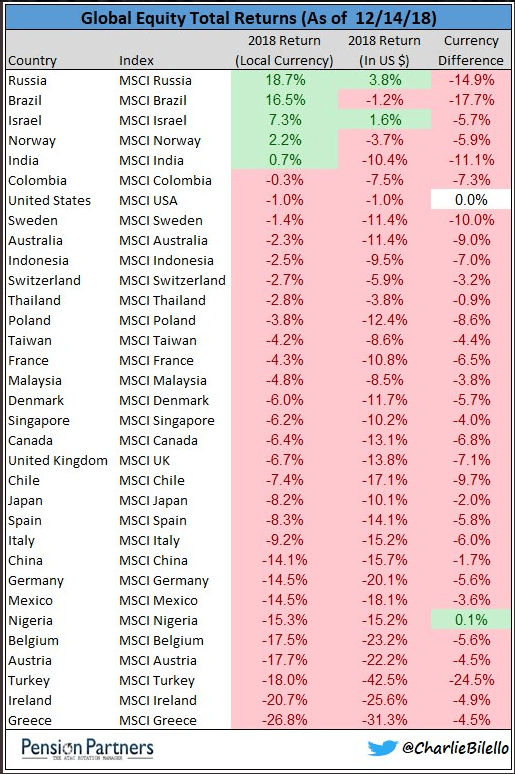

Global Equity Returns

Germany’s Perverted Yield Curve

Jeff Bezos’ Company Christmas Party