My father-in-law died of rectal melanoma, a disease so rare his doctors didn’t even know it existed. He was diagnosed with having a rectal fissure. He lived with some discomfort until I called him one night. Slurring his words, he said he felt “really shitty.”

My immediate response was he was having a stroke and called 9-11. Sad story short, the melanoma, a relatively benign cancer if caught early but spreads through the body like wildfire if not treated, had moved into every vital organ in his body. Terminal.

This sad story of my father-in-law reminds me of what we believe is the misdiagnosis of today’s asset markets. Like rectal melanoma, today’s market backdrop is so extremely rare and unprecedented that nobody knows how the future will play out. Creating the condition markets hate most – uncertainty.

Rare Conditions

Let us review for a moment the rare factors and conditions, which are determining the backdrop of current asset price dynamics,

- The Federal Reserve is taking unprecedented action reversing the massive expansion of its balance sheet. Thus far, we calculate its holdings of Treasury and Mortgage-Backed securities have been reduced by around $350 billion since October 2017. That equates to about 16 percent of the Q3 2017 U.S. monetary base.

- The supply of negative yielding debt reached a peak of $12 trillion in mid-2016 (24.2 percent of Advanced Economies (AE) GDP and after falling to around $5.5 trillion has climbed back to $7.76 trillion (15.1 percent of AE GDP) last week on the Q4 flight-to-quality trade.

- The United States implemented a pro-cyclical fiscal policy at the beginning of 2018, which is very rare and maybe unprecedented.

- The United States government borrowing requirement is north of $1 trillion per annum as far as the eye can see with no plan for long-term fiscal sustainability. In other words, the global capital market is being hit by a huge supply of Treasury securities. Unprecedented during an economic expansion, and appears can only be funded without a spike in interest rates with haven flows. That is selling in other markets.

- At the end of Q3, U.S. stock market capitalization to GDP was at a high only seen in 1929 and 2000.

- If the S&P500 closes the year at the current level, it will be only the 5th quarter that S&P500 fell more than 10 percent with the economy growing at 3 percent in the past forty years.

- Portugal’s 10-year yield is trading 120 bps lower than the U.S., which we doubt reflects interest rate parity. Italy’s yield, after trading years below the U.S., in now only 10 bps wider.

- Global politics, including President Trump’s mounting political and legal issues

- The collapsing post-War order

Traditional Metrics

Considering all the above, the market still focuses and is obsessed with traditional tools and metrics.

We posit that the Fed’s move off ZIRP to a 2-2.25 percent Fed Funds rate target, with core inflation running at 2.0-2.5 percent should not wreck a viable economy. We believe the move to normalize short-term interest rates are not what is disrupting the market’s unstable equilibrium, which, by the way, has been relatively stable over the past seven years. Think Minsky.

Crowding Out

It is the combination of the large borrowing requirement by the U.S. government due to its larger deficits and the roll-off of Treasury maturities in the Fed’s quantitative easing portfolio, which monetary policymakers maintain is on autopilot.

Though quantitative tightening calls for a maximum of $30 billion per month in the Treasury portfolio and $20 billion in the MBS portfolio to be redeemed, the realized amount depends on the maturity structure of the securities in the SOMA portfolio in any given month.

Rather than showing up in the banking system, the tightening of liquidity is showing up in the bond markets. The $247 billion the Fed has rolled up has to be refinanced by new buyers or the Treasury is forced to run down its checking account balance at the Fed.

Upshot

The U.S. government’s financing requirement, which includes the Fed’s roll-off of Treasuries, is a better diagnosis, of what ails Mr. Market, in our opinion. The Treasury is crowding out other asset markets and now competing more voraciously for global capital. Without quantitative easing or leverage, it is a zero-sum game.

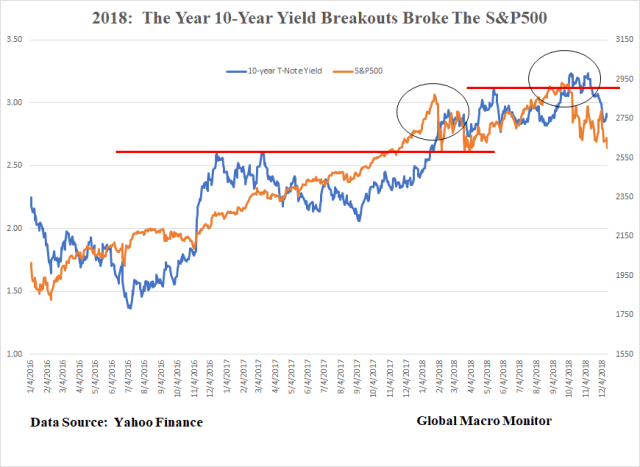

Note in the above chart, January’s stock market correction began just a few days after the 10-year yield broke out. The Q4 correction began on the same day.

Why are yields rising? Several reasons (see here), including the large increase in supply, though the Treasury appears to engineering a flatter curve by front-loading the bulk of the supply in 2 and 3-year notes.

It appears the note and bond yield cannot remain at current levels or go lower without haven flow buying, which by definition, means selling in other risk markets. The market may be signaling long-term rates should be much higher but the economy cannot sustain those levels. Too many distortions and noise to say with any level of certainty, however.

Politically Neutral Fed Funds Rate

As Mr. Market and Mr. President pound Mr. Powell, he may or may not recognize this.

If he caves to the pressure and doesn’t raise the interest rate on Wednesday, the risk markets will experience the year-end rally that it pressuring the Fed to ignite. Temporarily.

On the other hand (we are economists, after all), if the Fed addresses the stress quantitative tightening and the fiscal imbalances are putting on the markets, the rally should be more powerful and long-lasting.

What Should The Fed Do?

Glad you asked.

In our opinion, rather than fret over what is the politically neutral Fed funds rate they should ignore the market noise and presidential tweets, and do what they believe is line with their trajectory for inflation and the economy. That could be in line with what Mr. Market and Mr. President want, or it could not.

Otherwise, Mr. Powell’s Fed, who still has a chance to break from the ghost of the market ownage of Christmas past, will be reacting to stock market volatility until kingdom come. Good luck with that one.

The signals from a distorted yield curve and the message of the current correction may just be noise. After all, the economy grew almost 7 percent in the same quarter of the 1987 stock market crash, with the S&P finishing down over 23 percent in the last three months.

Could it be that risk is not correctly priced and Mr. Market is making the adjustment? At least, put it on the table for consideration and then begin to think about structural reform to fix what ails the market.

Here’s to hoping the economy has not morphed into the asset-driven monstrous vermin we fear it may have, tossed to and fro by the next 10 percent move in the S&P500. I guess will find out if the Fed believes that on Wednesday.

The question to ask then: does a recession cause a market sell-off or does a market sell-off cause a recession?

As always, we reserve the right to be wrong.