Summary

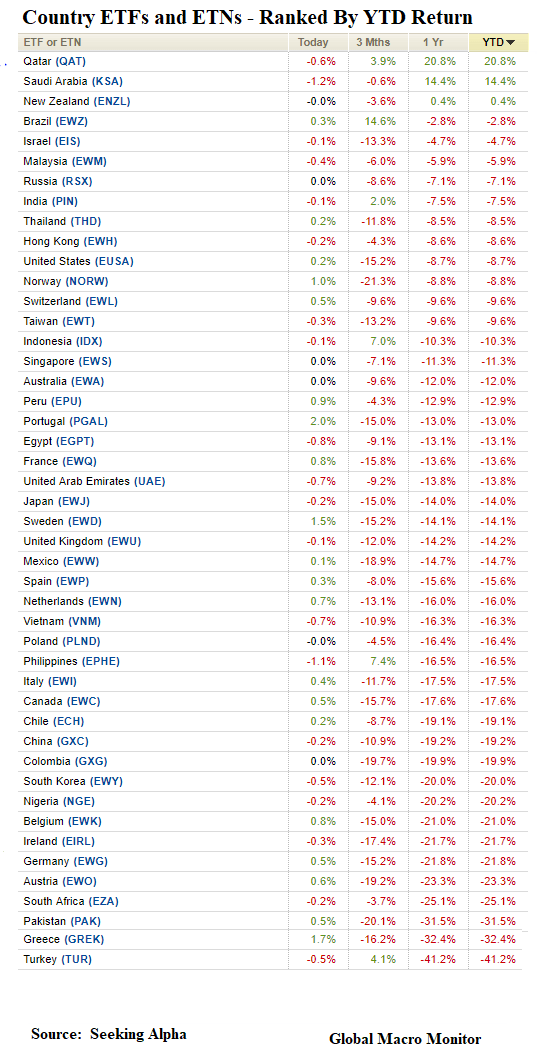

- Fugly year for the financial markets. Unless you’re a trader, 2018 couldn’t end fast enough. The country ETF table illustrates the pain for dollar-denominated returns as only Qatar and Saudi delivered positive returns > 0.5 percent

- China and Brazil led local currency bond markets with Mexico, Indonesia, and Turkey 10-year yield blowing out 100 plus bps. The U.S. 10-year yield climbed 27 bps even as the major stock indices were down almost 10 percent. Extremely rare

- The U.S. yield curve pancaked with the 10 minus 2s down 33 bps. We suspect much was technical. More later

- U.S. credit began to blow out in Q4 and not much of recovery in the last week with stock bounce. Be wary of stocks until credit begins to recover

- Bad year for EM FX with Argentina, Turkey, and Russia taking major hits. Some EM currencies did begin to stabilize and recover the losses in Q4, however. We blame the huge increases in the U.S. public sector borrowing requirement, which will continue to suck up global liquidity

- The dollar index was up over 4 percent on the year hitting a high of 97.71 in mid-December. Markets are betting on a lower dollar. Not so sure. We will watch and wait and don’t believe the U.S. is heading into a recession in 2019

- Watch 104.55 on Dollar/yen and 114.55 to the upside

- We like cable and expect the pound to rally to over 1.40 on the back of a second BREXIT referendum, which should be announced sometime soon and will almost surely result in a remainers victory. If we’re wrong 124.33 is your stop.

- Ugly year for all stock markets in dollar returns

- Brazil stocks are our top pick as the New Year begins with the Bolsonaro government taking power. Political risk is elevated but not yet

- China stocks may see a bounce on the hype of a trade deal in January. Worth a trade

- Can European banks get any worse? Deutsche Bank continues to circle the drain and will probably be rescued by mid-year. The question is will the German government and EU wipe out current shareholders with a bail-in? Probably, and the market senses it, making the bailout self-fulfilling

- The grains stood out as the only decent performer in our coverage of the commodity complex. Crude will hold the key in 2019 but we don’t expect a major recovery and could see a $30 handle by end of Q1

- The CRB down over 12 percent on the year due to crude’s weighting. Don’t you wish landlords moved your rent based on commodity prices? The decline in crude oil is a change in relative prices and results in economic stimulus as consumers real income has increased

Commentary: What’s up in 2019? More volatility. We expect a huge Rumble In The Jungle, especially after the attempted January rally fails. Stay tuned for the trades we think will work.

Note how wrong the market was on expectations on a Fed hike and a pause.

Pingback: Dollar On The Launchpad | Global Macro Monitor