Summary

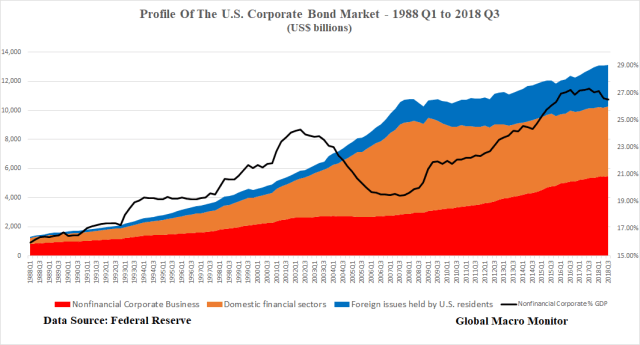

- Nonfinancial corporates have amost doubled their stock of outstanding bonds since the GFC moving from 19.5 percent of GDP in 2007 to 26.5 percent in Q3 2018

- Conversely, the domestic financial sector has been delevering, reducing bond debt by almost 25 percent since 2007, which reduces systemic risk

- Foreigners are by far the largest holders of U.S. corporate bonds and, we suspect, the weakest hands

We spent most of the day crunching numbers on the U.S. corporate bond market as stocks went on another roller coaster ride. Given all the hand-wringing and concern over the buildup of corporate debt since the Great Financial Crisis (GFC), we have a real need to see and understand the data.

The Data

We look at the changes in level, profile, and ownership of the corporate bond market over two different periods with the Fed’s Flow of Funds data. Our point of reference is Q4 2007, which was not only the end of the early century bull run in stocks and beginning of the GFC but also the quarter where nonfinancial corporate debt as a proportion of the corporate bond market was at its lowest (26.6 percent).

Fast forward 43 quarters to Q3 2018, the latest available data, and lag back 43 quarters from Q4 2007 to Q1 1997, and there you have our three points of measurement.

Conclusions/Data Inferences

1997 Q1 to 2007 Q4

- The data illustrate the massive build in leverage in the domestic financial sector from 1997 to 2007, which was the primary cause of the GFC. Domestic financial sector bond debt grew by 378 percent over the period, increasing at a compounded average growth rate of 15.7 percent, to almost 60 percent of the market.

- The stock of nonfinancial corporate bonds grew at a more modest CAGR at 5.5 percent during the same period, right in line with nominal GDP growth.

- Foreign issues in the U.S. experienced significant growth though from a small base.

- Overall corporate bond debt to GDP grew from 41.08 percent of GDP in 1997 to 73.15 percent by Q3 2018.

- Foreign issues should be excluded from the bond debt-to-GDP ratio to gain a better measure of the true debt burden on the U.S. private sector.

2007 Q4 to 2018 Q3

- The U.S. domestic financial sector has been deleveraging since the GFC, reflected in the negative 23.7 percent growth rate in the sector’s bonds outstanding.

- Conversely, nonfinancial corporates have grown their bond debt by over 90 percent to 42 percent of the corporate bond market and 26.50 percent of GDP, up from 19.47 percent in 2007.

- Nonfinancial corporate bonds now make up the most significant percentage of corporate bonds outstanding in the U.S. and, by extension, now the biggest

- The diminishing liquidity, or lack of traditional market makers, magnifies the risk of an outsized dislocation in the sector. Though not on such a massive scale, the buildup in nonfinancial corporate bond debt since 2007 mirrors that of the financial industry from 1997 to 2007.

Who Owns The Corporate Bond Market

- Foreign holders of U.S. corporate bonds make up the largest ownership group subjecting the market to capital flight risk, which, in other countries, is often sparked by domestic political instability. Watch this space.

- Life insurance companies are the most significant domestic holders of corporate bonds, taking down almost 20 percent of outstandings.

- Mutual funds are a close third followed by households, which include hedge funds.

- Other makeup over 20 percent of corporate bondholders but each group is less than 5 percent of the market. They include state and local employee pension funds, banks, state and local governments, broker-dealers, ETFs, closed-end funds, among others.

- The largest hands – foreign holders – are most likely the weakest hands. Another risk not even close to the radar of most traders and investors.

Upshot

You now have the data and charts, folks. Short and sweet, easy to read.

Now you have knowledge and can’t claim you were unaware of the risks if the GE refrigerator falls through the kitchen floor.

Data Source

Help keep the lights on at the Global Macro Monitor. Contribute any amount based on your perception of our value added by clicking the PayPal donate widget at the right side of the screen. You don’t need a PayPal account just a credit card. Thank you!

Pingback: Gundlach’s Coming Corporate Bondageddon | Global Macro Monitor

Pingback: Ownership & Profile Of The U.S. Corporate Bond Market – Q4 2019 | Global Macro Monitor